An accounting policy is a documented set of rules governing accounting at an individual enterprise. The provisions of the order on accounting policies are based on generally accepted accounting principles. These recommendations are binding.

History of occurrence

For the first time, the Russian accountant came across the concept of “accounting policy” in the early 90s of the last century. The characteristics of the document were recorded in the Regulation “On the Accounting and Financial Reporting of the Russian Federation”. But widespread use in practice did not begin immediately. Today, no organization is complete without the creation and observance of individual accounting rules.

Accounting Policy Framework

Any set of rules cannot be created unreasonably. When developing and approving a document, the chief accountant and company management should pay attention to the following criteria, on which the essence of accounting policy directly depends:

- Status, form of ownership, type and type of activity of the company.

- Current and long-term development plan.

- Features of financial activities depending on industry.

- Professional qualifications of employees.

- The economic situation in the company.

The accounting policy of the organization is formed on the basis of generally accepted rules of accounting. accounting based on the specific situation of the enterprise.

What issues should be covered by accounting policies?

The approved document governing the accounting at the enterprise must not only comply with established state standards, but also comply with all aspects of the accounting process. There are three types of characteristics of accounting: methodological, organizational and technical.

An understanding of the methodology includes a description of the techniques used in the accounting process, which are legally presented to the enterprise of choice. For example, each legal entity has the right to independently determine the method of calculating depreciation. There are a lot of such issues on which the accounting of one organization may differ significantly from another. In addition to depreciation, they include:

- methods for classifying the property received as OS or IBE;

- financing of OS repair work;

- methods for assessing IBE and other valuable property;

- accounting for output, procurement and acquisition of values;

- recognition of sales revenue;

- creation of property accounting groups, reserves, special purpose funds.

The order on accounting policies contains a detailed description of teaching techniques. accounting for a particular company. The task of the accountant is to comply with the requirements stated by the management.

Technical and organizational aspect of accounting policies

Technical aspects reflect the use of the provided methods in practice, that is, they regulate the use of certain accounts, forms of documents and other things. These include:

- approved chart of accounts;

- forms of accounting registers;

- data processing techniques;

- drawing up reports;

- control of the internal production sphere;

- order and terms of inventory.

The organizational aspect of the accounting policy of accounting is in the form of a description of the importance of accounting in the enterprise, its relationship with other departments of the financial system.

Normative base

The following documents are used as documents on which accounting of any enterprise is based:

- Regulation “On Accounting and Financial Reporting in the Russian Federation”.

- Instructions on the application of the Model Chart of Accounts of the Russian Federation.

- Regulation of the Ministry of Finance of the Russian Federation “On the accounting policy of the enterprise”

- Regulation “On costs and their composition”.

- Decision on accelerated depreciation and revaluation of OPF.

- Cost recommendations for a particular industry.

The procedure for compiling documents on accounting policies

Approved by the founders, the sample accounting policy of the enterprise should be documented in the form of an order, order, regulation, job description. A major role in the preparation of accounting policies is played by constituent documents, which lay the foundation for accounting according to the type of business entity.

The accounting policy for the year is approved, during which changes can be made only in cases critical for the enterprise: liquidation, transformation or reorganization. The reason may also be changes in requirements for accounting and financial accounting at the state level.

Newly established enterprises must approve accounting policies within 90 days. The countdown starts from the moment you acquire legal rights or register with government agencies.

Change in accounting policy content

If the need for changes is not due to serious reasons such as reorganization or liquidation, the company has the right to edit the document for the new reporting year. Changes come into force on January 1 of the year following the date of publication of the document. It should be remembered that the preparation of a new accounting policy should be reflected in the annual financial statements in the form of an explanatory note.

Any change must be justified, because the order on accounting policies directly affects the economic activity of the enterprise. It is especially necessary to carefully check the need for methodological changes that can directly affect the financial result.

Accounting policies reflected in the financial statement

A sample accounting policy of an enterprise must be published. Employees should be familiar with the requirements that directly affect the performance of their duties. The need to mention accounting policies arises in the preparation of financial statements. But it is not necessary to disclose the content of the entire document: it is enough to reflect the main points.

There are two methods according to which the company reflects accounting policies in the annual report: an indication of deviations from the rules or a description of each item. The first option involves the most complete characterization of established accounting methods. At the same time, they describe all the methods established by the state or adopted independently.

If the company carries out financial activities strictly within the framework accepted by the state, the accounting policy is characterized only in cases where deviations from the general rules are observed. In other circumstances, it is sufficient to indicate that the company fully complies with the recommendations of the state on bookkeeping.

Reflection of tax accounting

Tax accounting at the enterprise should be carried out in strict accordance with the articles of the Tax Code of the Russian Federation. In the section of the accounting policy reflecting the procedure for tax accounting, items should be included that describe:

- the procedure for reflecting tax accounting data;

- establishment of responsible persons for maintaining and organizing tax accounting;

- terms and composition of documents provided to the responsible person;

- types of accounting tax registers.

A tax accounting policy should be created based on the tax base of the enterprise, a list of obligatory payments to the state budget, and workflow rules.

Regardless of the direction of the enterprise, the accounting policy should reflect the requirements of the Tax Code. The expenses and income of the enterprise, the procedure for their formation, determination of taxable shares is the basis of tax accounting, which cannot be canceled or completely changed.

Changes in tax accounting policies for 2016

In 2015, the Tax Code of the Russian Federation underwent changes that come into force from the beginning of 2016.Some of the amendments will affect the operations of enterprises. When compiling the accounting policy for 2016, it is necessary to take into account the following requirements of the Tax Code:

- property on which depreciation is charged are considered material values worth more than 100 thousand rubles;

- for enterprises that pay income tax on the amount of 10-15 million rubles, the limit on the amount of income from sales for the quarter increases;

- The simplified tax system was canceled for organizations whose revenues exceed 79 million 740 thousand rubles.

Accounting policies: articles and their characteristics

The document establishing the procedure for the implementation of accounting consists of 5 sections:

- general information regarding the organizational part of accounting;

- methods of accounting for fixed assets and intangible assets;

- accounting of inventories;

- reserve creation procedure;

- accounting for other income and expenses.

General information may be filled in in any form, but it must necessarily contain information about the company, responsible persons, application of a standard or working chart of accounts, and organization of accounting.

Reflection of accounting methods for fixed assets and intangible assets

OS accounting procedure and intangible assets regulates the accounting policies of the enterprise. An example of filling this section is given below:

OS accounting

- Accrual depreciation method - linear / cumulative / decreasing balance / production.

- The minimum value of property attributable to fixed assets is 100 thousand rubles.

- Control over assets with a value less than the minimum - on off-balance sheet account 013.1 / registers of analytical accounting.

- Annual revaluation of fixed assets - made / not made.

- Analytical accounting document - inventory card / inventory book.

- Retain inventory cards for n years.

Intangible Assets

- Accrual of depreciation - by the linear / production method - of the reduced balance.

- Reflecting the presence of intangible assets on the balance sheet - reflect / not reflect.

- The useful life and depreciation method for the current year are changed / not changed.

Characteristics of accounting policies of inventories and reserves

Accounting procedure inventory reflects the accounting policies of the enterprise. A sample (Russia) of compiling the characteristics of accounting for MPZ will be considered as an example:

The accounting policy of enterprises governs the accounting of inventories according to the following rules:

1. Assess:

- materials - at the actual / accounting price;

- finished products - according to the actual / normative using sc. 40 / normative without the use of sc. 40 price;

- goods - at the purchase / sale value.

2. Transport and procurement costs for the sale of goods should be included in the cost / sale items.

3. Write off MPZ from the warehouse at the average cost / cost units / method FIFO / method LIFO.

4. To carry out the formation of value at full / reduced cost.

In the section for creating reserves, the amounts of future expenses are indicated by cost items, as well as the need for creating reserves for doubtful obligations and for reducing the cost of fixed assets and intangible assets is indicated.

An example of the contents of the accounting policies of the enterprise for accounting

Consider one of the possible options for processing documentation related to the description of methods boo. accounting.

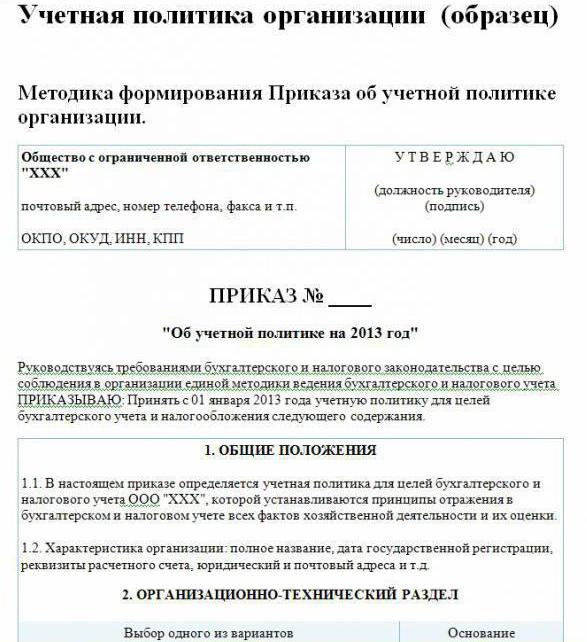

Accounting policy of the enterprise (sample):

Visit LLP

st. Builders, 48

phone 8 (3812) 234949

fax 8 (3812) 234853

Order No. 23

“On accounting policies for 2016”

According to the legislation of the Russian Federation, in order to comply with a unified system of accounting and tax accounting

I ORDER:

Approve from 01.01.2016 the accounting policies of the company for accounting goals given content:

Organizational and technical aspects

1.1. Accounting is an accountant.

1.2. The level of centralization of accounting is centralized.

1.3. The organizational structure of accounting is linear.

1.4. Forms of primary documents developed by the enterprise independently and presented in the annexes to the order.

1.5. Persons entitled to leave a signature in the primary documentation are listed in the appendix to the order.

1.6.The accounting form is automated.

1.7. The company uses the Standard Chart of Accounts of the Russian Federation.

1.8. The procedure for conducting an inventory, the composition of the commission is approved in the annex to the order.

Methodological aspects

2.1. Depreciation of fixed assets and intangible assets is calculated on a straight-line basis.

2.2. Set the minimum cost of the OS in the amount of 100 thousand rubles.

2.3. As part of the MPZ, assets with a value of not more than 82 thousand rubles are subject to accounting.

2.4. Amounts of depreciation deductions of intangible assets shall be reflected on account 05.

2.5. Do not reevaluate the OS.

2.6. Take material values into account without using accounts 15, 16.

2.7. MPZ should be put into production at an average cost.

2.8. Transportation and procurement costs should be included in the actual cost.

2.9. To evaluate the purchased goods at actual cost.

210. The accounting of output shall be made using account 40.

2.11. Reserves for future expenses are not created.

Methods not specified in this document should be applied in accordance with the Regulation of the Ministry of Finance of the Russian Federation “On Accounting and Financial Reporting”.

Director Savochkin P. B. signature

In the given example of accounting policy, only the main points of the methodology for organizing accounting are indicated. accounting. For the most part, the company is based on generally accepted rules.