A statement of changes in equity is a mandatory financial reporting document that reflects the movement of equity capital, as well as containing information on the amount of retained earnings (loss) and the share of the company. Small business owners with the right not to conduct an audit and non-profit entities may not draw up this report and exclude it from the financial statements.

Composition and structure of the report

The document is divided into 3 parts, each of which has a tabular form. Despite the fact that there are established forms for the preparation of samples reporting, enterprise can independently edit the document to obtain the desired view. Nevertheless, it should consistently indicate information on the sections:

- I - "The movement of capital."

- II - “Adjustments due to changes in accounting policies and bug fixes.”

- III - “Net Assets”.

The content of the statement of changes in equity fully reflects events occurring with the company's own sources. The first section is devoted to the capital structure and operations conducted with it. The second consists of at least three, and if it is necessary to reflect changes in other capital items, then more parts. The third section contains information on the values at the end and beginning of the period of net assets. The report on changes in capital (form 3) should be compiled on the basis of data for 3 years: the reporting and two years preceding it.

Report Content Requirements

The report on changes in capital (form 3) must be drawn up in accordance with the requirements of the RF Ministry of Finance. The contents indicate:

- values of net profit and loss;

- each item of profit / loss, income / expense in monetary terms and their amount;

- the effect of the accumulation of changes in accounting policies and the adjustment of errors considered in accordance with IFRS;

- operations related to capital;

- changes in additional and reserve capital, as well as the state and value of the shares of the enterprise.

The data should be presented in the report itself or in the appendix to it. Subject to the accounting and financial accounting rules, it is not difficult to fill out form 3 “Report on changes in capital”, a sample form of which can be found in the recommendations of the RF Ministry of Finance for the preparation of mandatory financial statements.

Description of the first part of the report

Section I of the third form contains information on all changes in the elements of the company's equity for the period under review. It includes: authorized, additional, reserve capital, as well as data on retained earnings (loss uncovered), repurchased shares from owners of the enterprise.

In each of the parts indicate the relevant indicators, which can be compared with the data of past years. If the company has not changed accounting policy then the values will coincide with those recorded in the reports for the past 2 years. In case of changes, it is necessary to carry out data adjustments and indicate the reasons for the discrepancy in the explanatory note to the report.

Share capital: rules for filling in the columns

The authorized capital of the enterprise is created during the formation of a legal entity through contributions from the founders. During the financial activities of the company, the volume of assets may change, which should be documented.

The statement of changes in capital begins with the first part of the “Authorized Capital” of Section I. The data necessary to fill in is on account 80, which is opened for accounting of funds in the authorized capital. In the column indicate:

- the balance of the initial capital as of 31.12. reporting year and two previous years;

- Amounts by which capital was reduced or increased in one year.

Credit turnover on account 80 indicate in the corresponding line of the report - capital increase. If there are debit turns in the account of the authorized capital, fill in the column explaining the reasons for its decrease. An increase or decrease in the number of shares and their face value and also reorganization of the enterprise.

Own and repurchased shares

The data for this article of the report are in the balance sheet (section III). The numerical value of shares owned and repurchased from shareholders is included in and deducted from equity. Because of this, it is recommended to indicate the amount in parentheses in forms 1 and 3.

Shares repurchased for further resale in value terms are reflected in the account. 81. The amount is the actual cost of the acquisition. When shares are withdrawn from circulation, the amount of the authorized capital is reduced by the amount of their value. The difference between the selling price and the face value is attributed to other income / expenses of the enterprise.

Reflection of additional and reserve capital in the report

Cash in additional paid-in capital is accounted for score 83. The main feature of filling in the column “Additional capital” is the reflection of indicators that affect its overall value. Moreover, the reporting period is taken from the reporting period from 31.12 of the previous year to 1.01 of the reporting year. This procedure is established due to the rules of revaluation of fixed assets: data received on 1.01 of the new year must be indicated on 31.12. of the previous year. For example, when revalued on 01/01/16. For the report, the date 31.12.15 will be indicated.

The indicator is determined by the data on the turnover of the loan when interacting with accounts:

- accounting for cash and settlements in the formation of a positive exchange rate difference;

- accounting for financial results (account 91) in the formation of negative exchange rate differences;

- 75 on the amount of contributions of the founders in the property of the enterprise.

Accounting reserves are on the account. 82. The document indicates data on the amount of deductions in the reporting and two previous periods. Reserve capital is formed from retained earnings in order to pay off expenses in cases where it is impossible to pay them out of net income.

Retained earnings and uncovered loss

To reflect data on the amount of retained earnings (loss) use the period that affects the total value. As for the indicator of additional capital, the considered period is the period from December 31 of the year preceding the reporting year to 1.01. reporting year.

The indicators forming profit (loss) include:

- cash assets of net profit (loss);

- OS revaluation process;

- expenses and incomes affecting the change in the amount of capital;

- amount of dividends;

- process of reorganization of a legal entity.

Characterization of the values of some lines of the report

Revenues and expenses that are directly related to the increase (decrease) in capital do not include in the financial result of the company. In the case of income, their value is attributed to line 3213 (3313), and in the case of expenses, to line 3223 (3323) of the statement of changes in equity.

The values of the lines of capital reduction are indicated in parentheses, since the values change capital downward. Line 3227 (3327) contains information on the amount of profit that was distributed between the founders.

After the data of the first section has been successfully entered into the document, it is necessary to calculate the sum of all values. It should be borne in mind that the value in parentheses must be subtracted from the result. The total values should coincide with the data indicated in the balance sheet (section III).

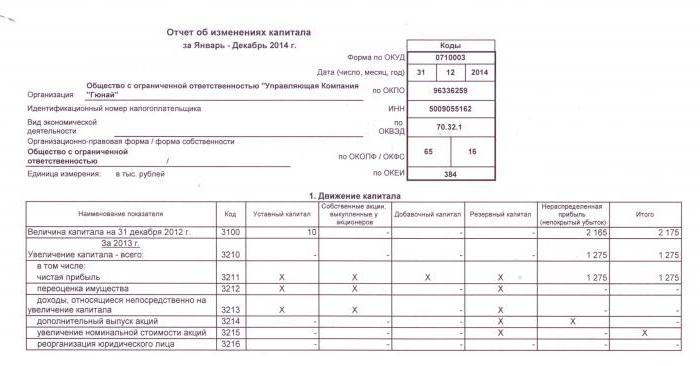

Filling in Section I of the statement of changes in equity

Each of the filled-in articles of the section has its own code. Consider the example of filling out the first section without specifying the amounts, considering the reporting year 2015. First, the data is grouped into subsections:

- code 3100 "Amount of capital as of 12/31/13";

- code 3200 "Size of capital as of December 31, 2014";

- code 3300 "The amount of capital as of 12/31/15."

Each of them (except 3100) contains the following information:

1. Code 3210, 3310 "Increase in the amount of capital, total", including:

- 3211, 3311 "Net profit";

- 3212, 3312 "Revaluation of fixed assets and intangible assets";

- 3213, 3313 "Incomes that directly relate to the increase in capital";

- 3214, 3314 “Additional issue of shares”;

- 3215, 3315 “Increase in the par value of shares”;

- 3216, 3316 "Reorganization of the jur. faces. "

2. Code 3220, 3320 "Decrease in the amount of capital", including:

- 3221, 3321 “Loss”;

- 3222, 3322 "Revaluation of fixed assets and intangible assets";

- 3223, 3323 “Expenses directly related to the decrease in capital”;

- 3224, 3324 “Decrease in the par value of shares”;

- 3225, 3325 “Decrease in the number of shares”;

- 3226, 3326 “Reorganization of the jur. faces ”;

- 3227, 3327 "Dividends".

3. Code 3230, 3330 "Additional paid-in capital".

4. Code 3240, 3340 "Reserve capital".

The table shows information without a column about the name of the article: only the code is used. When reporting, you must fill in all 8 columns.

| Code | Authorized capital | Own shares repurchased from owners | Extra capital | Reserve capital | Retained earnings (loss) | Total |

| 3100 | () | |||||

| 3200 | () | |||||

| 3210 | ||||||

| 3211 | - | - | - | - | About (Ct.) 84 count 99 | |

| 3212 | - | - | Ck (Ct) 83 | - | ||

| 3213 | - | - | About (Ct.) 83 | - | ||

| 3214 | About (Ct.) 80 count 75 | About (Ct.) 81 in correspondence with sc. 75, 91 | About (Ct.) 83 in correspondence with sc. 19, 75 | - | - | |

| 3215 | About (Ct.) 80 count 75 | About (Ct.) 83 in correspondence with sc. 19, 75 | - | - | ||

| 3216 | ||||||

| 3220 | () | () | () | () | () | |

| 3221 | - | - | - | - | About (Dt) 84 count 99. The value in "()" | () |

| 3222 | - | - | () | - | () | () |

| 3223 | - | - | () | - | () | () |

| 3224 | About (Dt) 80 count 75. The value in "()" | About (Dt) 83 count 75, the value is in "()". Or About (Ct.) 83 in correspondence with sc. 80 | - | () | ||

| 3225 | About (Dt) 80 count 81, the value in "()" | The total turnover on the account. 81 (if the amount of About (Dt) ›the amount of About (Kt), then the value in" () ") | - | () | ||

| 3226 | () | |||||

| 3227 | - | - | - | - | About (Dt) 84 count 75, 70, value in "()" | () |

| 3230 | - | - | About (Dt) 83 in correspondence with sc. 84 | About (Ct.) 82 count 83 | About (Ct.) 84 count 83 | - |

| 3240 | - | - | - | - |

In parentheses are the values that are subtracted during the calculation, and a dash means an empty column. The table shows an example of filling out without specifying the amounts of data in the first section of the statement of changes in equity.

The lines of subgroup 3300 are filled in the same way as 3200. After filling in each column, the final value is displayed, which is indicated in the lines of subgroups 3210 and 3220, and then in the general characteristic of capital for the year (line 3100, 3200). In order to determine the value of the column "Total", you need to add all the data of each column in a row.

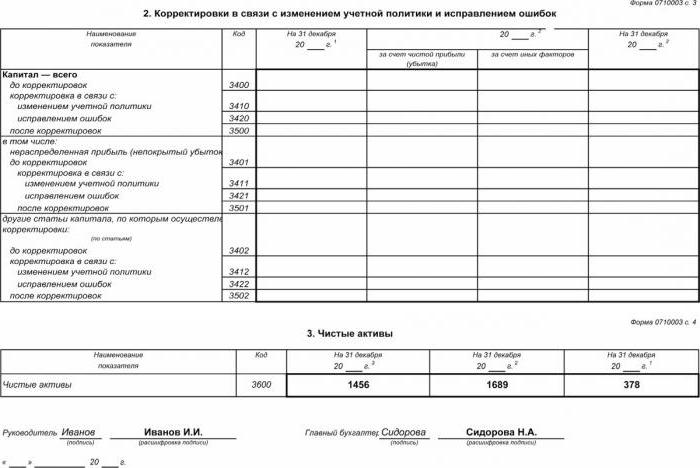

Section II - Correction and Correction of Errors

As in the first section, the data indicate the reporting period and the two years preceding it. The compilation of a statement of changes in equity using this document is mandatory only in cases where during the reporting period changes were made to the accounting policies of an enterprise or serious errors of previous years were corrected.

The report is compiled in the form of a table indicating the names of indicators, their codes and values for the 3 periods under consideration. The document is compiled using the algorithm:

- Indicate the amount of capital before adjustment in line 3400.

- In line 3410 reflect the adjustment values due to changes in the accounting policies of the enterprise.

- On line 3420, reflect the adjustment value due to bug fixes.

- In the necessary line of 3401-3502 indicate in detail the reason for the adjustment of the capital item.

The second and third points of the algorithm are carried out depending on the necessary actions: the adjustment is made due to the correction of errors or changes in the accounting policies of the organization.

Statement of Changes in Equity: Section III

The form of the third part of the report contains information on the net assets of enterprises for the 3 periods under review. Net assets are the sum of the value of non-current and current assets that are secured by equity. The value of the net assets of AO and LLC is calculated according to the order of the RF Ministry of Finance.

Accounting is the main data source for calculating net assets. The values for the calculations are taken from the balance sheet (form 1). The net asset formula is: Ch.a. = A - About - Z, where:

- A - assets that are taken into account (current and non-current assets, section I-II of the balance sheet);

- About - the amount of obligations accepted for calculation (excluding deferred income free of charge or in the form of state assistance);

- З - debt of shareholders on the amount of contribution to the authorized capital.

AO or LLC is extremely important to monitor the indicator of net assets: it will always be equal to or more than the authorized capital.If the condition is not met, it is necessary to take measures to comply with it: reduce the amount of own funds contributed by the founders.

Generating a statement of changes in equity in 2016

For 2016, no adjustments were made to the preparation of the financial statements. Form No. 3 still consists of four parts: the title and three sections.

The title should contain basic information about the company:

- name;

- OKPO, TIN;

- legal type of organization, OKOPF code;

- OKVED;

- reporting year and date of filling out documents;

- form of ownership and OKFS code;

- Indication of the rounding code for amounts up to thousands of rubles (384) or millions (385).

Most of the title page is drawn up like other reporting forms.

Data must be indicated sequentially for each year (from the third to the reporting year), negative values should be enclosed in parentheses. Fill in blank fields with a dash. The last date for the submission of the annual report for 2015 is the date 03/31/16.

Financial analysis of the statement of changes in equity

A qualitative analysis of the annual reporting, in particular form 3, allows you to evaluate the development of the enterprise in dynamics and to develop further goals of financial activity. The results of the systematization of data may indicate the near future of the organization: bankruptcy or an increase in profit. Considering the indicators of the report on changes in capital, the specialist is able to highlight the strengths and weaknesses, thereby providing management with the opportunity to regulate their own business policies on favorable terms.

The nature of the analysis of reporting depends on the purpose, which can simply be monitoring data or determining liquidity, creditworthiness, solvency and other indicators of the effectiveness of an enterprise. For calculations using the appropriate coefficients.

The main indicators of the company’s capital flow are the coefficient of income and disposal of funds, which are determined by the formulas: KP = П ÷ Сc.g., Kat = V ÷ Cng. The coefficient of income is calculated as the ratio of the amount of capital received to the balance at the end of the year, and the coefficient of disposal - as the amount of disposed of funds to the balance at the beginning of the year. If the income ratio exceeds the value of the disposal coefficient, then the equity of the enterprise is enriched. The rule also applies in the opposite direction.

The statement of changes in equity is included in statutory financial statements, which consists of four forms. Entries are made only on the basis of accounting data. Most of the information is transferred from the balance sheet. After calculating the total amounts of form 3, it is necessary to check their coincidence with the data of form 1.