At the end of 2013, the Federal Tax Service of the Russian Federation, in agreement with the Ministry of Finance, issued a letter proposing the introduction of the UCD - a universal transfer document. As the tax service explained, it could be used already from the beginning of 2013. A universal transfer document was introduced instead waybill and invoices. In Federal Law No. 402, organizations and entrepreneurs are given the right to independently develop the primary securities that are necessary during work and the use of which will be most convenient. Let us further consider what constitutes a universal transfer document. A paper sample will also be presented in the article.

General information

The FTS proposed in its letter to combine the invoice and the accounting document. This innovation applies to all business entities, including those working on a simplified taxation system. Thus, enterprises can not only receive UPD from contractors. The company has the right to write out the universal transfer document themselves. In this case, the main requirement is compliance with all the required details listed in paragraph 2, Article 9 of the Federal Law No. 402.

Functions

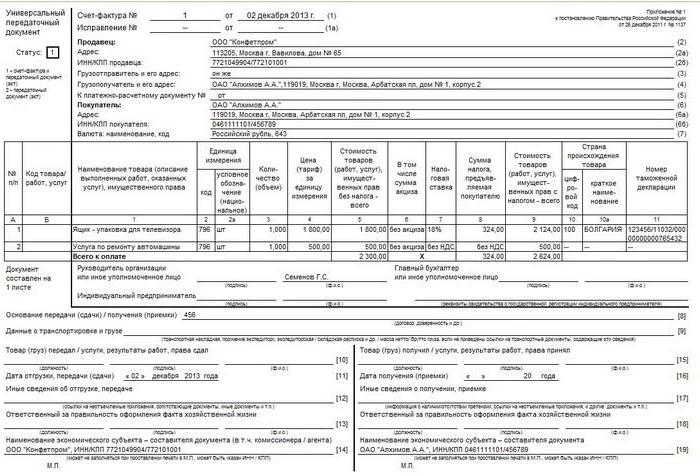

The universal transfer document form is based on an invoice. At the same time, it is completely transferred to the new paper and is separated by a bold line. After that, information on the date of shipment and reception of products, responsible persons is indicated. These are the details that are usually present in such papers as OS-1, TORG-12, M-15 and so on. The use of a universal transfer document can be carried out in two ways. This is due to the fact that it contains the data of the invoice and primary accounting paper.

So, a universal transfer document can be used to confirm only the transfer of ownership or additionally for calculating VAT. Depending on this, certain codes will be indicated. In the special column in the upper left part the status of the universal transfer document is indicated. This can be code 2 or code 1. In the latter case, the paper acts as an invoice and act, in the second - only as a transfer document. When specifying code 1, a separate invoice is allowed. The owner of the property independently decides what function the universal transfer document will perform.

When can I apply paper to an enterprise on the USN?

Entrepreneurs and companies using the simplified special regime are not VAT payers. This is established by Art. 346.11 of the Tax Code in clause 2 and clause 3. In this regard, it is impractical to write out an operational tax statement for services, goods, and work during normal business operations. This is due to the fact that in their activities, "simplists", as a rule, use an act or an invoice - one paper confirming the fact of transfer of ownership and implementation. The form of such documents is not so voluminous and is more familiar in work. If desired, of course, you can use the innovation.

If the company decides to use a universal transfer document, the form should contain code 2. In some cases, entrepreneurs and companies meet valuable customers and charge VAT on sales. In this case, the counterparties receive products with input tax. In such a situation, it is more advisable to use a universal transfer document. When can I use paper for others? It can be used by intermediaries in the simplified tax system, who sell products / work with VAT on their behalf.This is because such agents are required to issue invoices and invoices to customers. In such cases, the code 1 is placed in the upper left corner.

Universal Transmission Document: Completion

Thus, a new paper can combine the functions of an invoice and an act of shipment. But for this to be implemented in practice, it is necessary to correctly fill out the document. In the invoices there are their details, and in the acts - their. And this information is different from each other. Consider the situation. A universal transfer document performs 2 functions simultaneously and has, accordingly, code 1.

In this case, information should be present in lines 1-7, columns 1-11. In paragraph 5 of Art. 169 of the Tax Code, as well as in Government Decision No. 1137, rules are established in accordance with which information is entered into the universal transfer document. Signatures of the chief accountant and manager or persons authorized by them must be mandatory. Otherwise, the paper will not be valid. If the document contains code 2, then it should indicate all indicators that are mandatory for any "primary". These details are listed in Art. 9, paragraph 2 of the Federal Law No. 402.

Important point

When entering data into a universal transfer document with code 2, you can enter information into lines other than mandatory. The presence of information in them will not be considered a mistake. On the contrary, in this way, the contents of the business transaction will be more fully revealed. However, experts recommend special attention in such cases to columns 7 and 8. They indicate the tax rate on VAT and the amount of deduction. If information is present in these lines, then the company on the simplified tax system can be counted as the payer of the specified tax. But according to the law, the subject does not have such an obligation. To avoid confusion, leave these lines blank. The exception is the cases mentioned above when the company fulfills the request of the counterparty or is an intermediary.

Mandatory details

To make it clear what and where to enter, it is advisable to present this information in a table.

| Props | Counts |

| Name | The name of the UPD is indicated in the upper left corner. It is specified by code 1 or 2. The column "status" is informative. When entering data only in this line without specifying other information in the remaining lines, the paper does not become an invoice or primary. |

| Date of preparation | Box 1 |

| Name of the business entity issuing the universal transfer document | Page 14 and 19 or "M.P." (print location). |

| Contents of operation | Columns 2b, 2a, 2, 6b, 6a, 6. These lines indicate information about the parties to the transaction.

Box 1 and column B (at the discretion) reflect the subject of the contract. Page 8 - the grounds for the emergence of legal relations. Columns 9, 17 and 12. They indicate additional information reflecting the circumstances and conditions of the operation. Page 11 and 16. They may contain clarifying information about the dates of fulfillment of the conditions. |

| Cash and (or) natural dimension | Page 2-6, 9. If the transaction is made with an advance payment, then the information is entered on page 5. |

| The names of the employees who performed the operation or are responsible for it. | Page 10 and 15 or 13 and 18. |

| Signatures of the above persons, their F. I. O or other details by which they are identified. | Page 13 and 18. In the absence of signatures in them, columns 10 and 15. If there is no signature in page 10, then "the Head of the enterprise or another authorized person". |

Possible difficulties

In the form of the document under consideration, in addition to details that are familiar to the employee, there are also those that may cause a number of questions. The tax service in Appendix 3 to his letter explains what information should be in unfamiliar lines. In addition, the Federal Tax Service clarifies what you need to pay attention to when filling out already known columns.For example, questions may arise when filling out lines 3 "Consignor and his address" and 4 "Consignee and his address". In addition to the name and location of these entities, it is allowed to supplement the information with information about the TIN and KPP.

Product / Work Code

It is put down in column B. This requisite is not considered mandatory. In this case, the main thing is that the subject of the operation be understood on line 1. If the entrepreneur decides to fill out this line, then when selling goods, you can enter the article of products. If we are talking about work, then the OKVED code is indicated. If information about the service, then the view on OKUN fits in. These data can subsequently help in calculating incomes if the company combines several special modes or uses reduced rates for insurance contributions.

Line 10

This column shall indicate the name of the position of the person who is responsible for the delivery of work or shipment of goods. It must also bear his signature and F. I. O. When issuing paper with code 1 without fail, it is certified by the head, accountant or their authorized representatives. If one of them gives the work or goods, then in page 10 it is enough to enter only the position and F. I. O. It is not necessary to re-sign.

Date of delivery / shipment

It is indicated on line 11. In accordance with the general rule, the date of delivery / shipment coincides with the date on which the shipping document was issued. In the prescribed manner, the “primary” is compiled on the day the transaction is completed. But there are cases when a document is executed on one date, and the shipment itself, for one reason or another, occurred on another. In these situations, of course, the numbers will be different. The universal document provides column 11, which indicates the real date of the operation. Even if the numbers match, it is recommended that you complete page 11. This will prevent inconsistent paper changes.

Other data on transfer / shipment

This information is indicated on line 12. Here you can provide links to information related to the transfer / shipment. For example, this can be data on certificates, passports, the number and types of any other documents that act as an integral appendix to the FRS. If the work is transferred, then a report with a detailed description may be provided separately. Often, tax officials require detailed information in such cases.

Responsible for clearance

Line 13 should indicate the position of the person who is responsible for the correct documentation of the transaction by the enterprise. His surname and initials are also placed here. Without fail, he must sign if his signature is not higher in the line of the person responsible for the shipment or certification of the invoice.

Name of compiler

It is indicated in column 14. Here the name of the person who wrote the document is entered. This may be an organization that maintains accounting with the seller in accordance with the contract. Line 14 is allowed not to be filled, provided that in the field "M. P." there is a stamp indicating the name of the compiler.

Likely difficulties with the buyer

Some columns of a universal document may raise questions from the counterparty. So, in line 15, he must indicate the name of the position of the person who received the goods or accepted work / services, his name, initials. His autograph is also put here. Line 16 shall bear the actual date of acceptance / receipt. This attribute is not considered mandatory. Nevertheless, the Federal Tax Service always recommends specifying it. The date that fits in column 16, should not be earlier than the date of the compilation of the UPD (in page 1) and the number in page 11. On line 17 "Other data on acceptance / receipt", you can indicate that the buyer has no complaints. If they arose, then you should provide a link to the document by which they were issued. Column 18 contains information about the person responsible for the correct execution of the transaction / transaction.The name of his position is indicated, a signature is put. However, the latter may not be necessary if the same person appears on line 15 as being responsible for acceptance. Column 19 should contain information about the purchasing enterprise composing the document. As with the seller, this may be an accounting organization. This line is not filled if there is a seal in the "M. P." field, if the necessary information is visible on the print.

Accounting reflection

As mentioned above, several different dates may be present in a universal document. In this situation, the most important thing is not to confuse anything. Consider the situation. For example, the seller company makes UPD. In accordance with it, accounting profit will be reflected in accounting. In general, this must be done on the date of shipment. It is indicated on line 11. If this column is not filled out, then income is recognized on line 1 - at the date of preparation of the document.

Nuance

If the universal document has the status 1, then it is necessary to determine the date on which the invoice will be considered issued. If you write out this paper in the usual mode at the request of the counterparty, then the VAT return is filed based on the results of the quarter when it is presented. If the company acts as an intermediary, then on the date of invoice submission, the accounting statement must be registered in the appropriate accounting journal. The number on which the paper is presented will be considered the day of shipment (column 11). If it is not indicated, then you should be guided by line 1. The exception is when the results of work are accepted and transmitted on different days. In these situations, the date indicated on page 16 will be relevant. Consider the situation on the part of the buyer. In accordance with the received document, the company reflects expenses in accounting. This is done on the acquisition date, which is indicated on page 16. The same day will be considered the date of receipt of the invoice. This rule is valid if the document has the status 1 and it contains all the details required for such cases. When reflecting expenses in tax accounting under the simplified tax system, it is important not only the fact of making a purchase, but also the payment for it. Other costs may also apply. For example, to reflect the expense for the main asset, it must be put into operation.

Conclusion

It must be said that the UPD is not a binding document. A letter from the Federal Tax Service is advisory in nature. The company itself chooses which documents it is more convenient for it to draw up - the usual ones or use the new form. In this case, it is advisable to look at the situation. When entering information into the DLC, a number of features should be taken into account. In particular, when filling out, it is necessary to comply with the requirements of Art. 9, Clause 1 of Federal Law 402 and Art. 169 Tax Code. It should be remembered that the details of the invoice and the "primary" are not identical. For example, the first one, when sold, indicates the country of origin of the product (domestic goods are an exception). However, for the primary documentation, such a requirement has not been established. Along with this, some details may not be available on the invoice, and for the "primary" will be required. Particular attention should be paid to dates. There are several of them in the document and they do not always coincide. All these nuances must be taken into account during registration.