According to the provisions of the law, netting between organizations is a method of terminating obligations related to the supply of goods, production of works, and the provision of services. It is allowed subject to a number of conditions. Let us further consider in detail how netting between organizations is carried out.

General information

Offsetting is often considered as one of the ways of making settlements between entities. This is due to the fact that it is reflected in accounting similarly to financial transactions. Meanwhile, it should be said that offsetting between organizations has a number of features. This is a rather complicated and complex operation. In its implementation, not only financial and accounting services should take part, but also supply and household, legal and other departments of enterprises. Close cooperation and interaction of these units will ensure the legally correct execution of the operation.

Specificity

According to Art. 410 GK, full or partial termination of obligations the term of which has not yet arrived, is not indicated or is determined by the time of the demand, it is allowed by offset. For this, a statement from one of the participants in the relationship is sufficient. The same business entities, as a rule, act as parties to two or more obligations, in accordance with which homogeneous counterclaims arise.

The considered method is used mainly in the presence of various agreements concluded by these persons. However, in practice, netting between organizations is also possible when enterprises act as participants in a single obligation. For example, in case of improper fulfillment of the terms of the contract by the commission agent, the principal may submit a claim to it. He has the right to demand the payment of a fine and indemnification. These requirements may be presented for offsetting counterclaims related to the payment of commission fees.

Key features

The requirements to be set off have a counter character. Each business entity has a certain obligation. Accordingly, the request of the other party appeals to him. Along with this, he is also a creditor, since the second participant has obligations to him. So, being a debtor, he has the right to make demands. The repayment method under consideration is used in homogeneous liabilities. This means that the requirements should concern one subject. As a rule, they are money.

Features of occurrence

According to the provisions of the current legislation, if the obligation allows you to determine, or provides for the day of performance or the time period during which it must be repaid, then the conditions of the contract are implemented on the specified date or within the prescribed period. An enterprise that is in debt to another business entity may present the latter with a uniform claim. But this is allowed only after the time specified for its repayment, not earlier.

Repayment specificity

Offsetting between organizations with equivalence of obligations is carried out in full. In practice, this situation is far from always the case. If the requirements are not equal to each other, then the larger of them is partially repaid in an amount equivalent to the value of the smaller one. It follows that a larger obligation will remain in the remainder.At the same time, smaller requirements will cease in full. Consider an example. The company has an obligation to another company in the amount of 400 p., And the second to the first - in the amount of 250 p. In the event of netting, the last claim will cease completely. And the obligation of the first company will remain in the amount of 150 p. Legislation allows for offsetting between three organizations. In addition, each obligation must have the above characteristics.

Exceptions

They are defined in Art. 411 GK. The norm indicates circumstances in the presence of which debt adjustment by the considered method is not allowed. In particular, this applies to obligations:

- for compensation for harm caused to health or life;

- on the payment of alimony;

- about lifelong maintenance;

- to which the statute of limitations applies and it has expired.

This list is considered open. The contract or legislative provisions may provide for other cases in which it is impossible to conclude an agreement on offsetting mutual claims.

General rules for the operation

As mentioned above, the presence of mutual debt acts as the basis for using the considered method of calculation between entities. The difficulty in carrying out the operation, as a rule, is due to the fact that the company in most cases has obligations to several contractors. Therefore, in identifying mutual debt often errors occur. To prevent them, you should:

- Keep specific and clear analytical records.

- Identify the amount of mutual obligation with each counterparty individually.

Registration

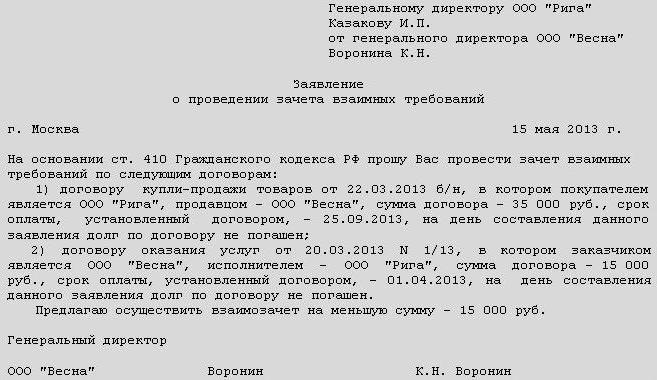

According to the provisions of the law, a statement from one of the participants in the relationship is enough to carry out the operation. At the same time, it should be documented. For this, a bilateral or trilateral act may be drawn up. The law also allows for the issuance of a protocol for the repayment of obligations. Also, the parties to the relationship can enter into an agreement on offsetting mutual claims.

Any of these documents will act as a legal basis for reflecting transactions in the accounting of enterprises. In addition, if they exist, there will be no disputes with the tax service. It should also be said that an offsetting agreement or other document fixing the transaction is necessary for the legal department of the company. The legislation does not allow its implementation without the consent of the counterparty. Otherwise, the second party to the relationship has the right to sue and collect the debt.

Common pattern

For clarity, we can consider the following example of netting. A contract was signed between the purchasing company (A) and the supplier company (B). In accordance with it, the first company accepted obligations to pay for products delivered by the second participant in the relationship. In accounting, the receivables of the supplier and the accounts payable of the buyer were reflected. These companies also signed a contract. Under its terms, the above firm B committed to pay enterprise A the work it did. Accordingly, the receivables of company A and the accounts payable of B. were reflected in accounting. These companies have counter obligations. Guided by the norms of the Civil Code, they signed an agreement on netting. According to the document:

- Company A repays liabilities to firm B. At the same time, it closes the receivables of the latter.

- Company B repays liabilities to firm A. Accordingly, it also closes the receivables of the latter.

This scheme is considered the most common in practice.

Act of offset between organizations: sample

This document is one of the ways to complete the operation. Certain requirements are imposed on him. In accordance with Art.9 (p. 1) of the Law on Accounting, all facts of economic life must be accompanied by supporting documents. They act as primary accounting papers. The act of netting between organizations also belongs to this category. The sample document contains the required details. They are:

- Name.

- Date of issue.

- Name of the company on behalf of which the document is compiled.

- The essence of the operation.

- Measuring units in money / kind.

- Names of positions of persons responsible for the operation and correct execution.

- Signatures of authorized employees.

Additionally

In accordance with clause 3.12 of the GOST, the registration number on the document consists of a serial number, which can be supplemented at the discretion of the catering or trade enterprise with the case index, according to the nomenclature, information about the executors, the correspondent, etc. When offsetting is made Act of reconciliation. It is executed by all participants in the operation. The registration number of this document includes the document numbers from each side. They are put across the oblique line in the order indicated by the participants. An integral element of the required details is the signature. It includes the name of the post, the autograph itself and its transcript. The act of netting must contain information about all its parties. Accordingly, the document must contain the signatures of these participants. A similar rule applies to the preparation of an agreement or protocol on netting between enterprises. After signing the documents, information about the operation performed should be reflected in accounting.