Mortgage for most Russians seems to be the only solution to the housing problem. But the unstable economic situation, overwhelming interest rates on mortgages, job cuts do not contribute to the development of a mortgage program that provides young families with conditions for expanding the family, or demographic growth with an improvement in the quality of life of those who need housing conditions. By the way, in 2017 the birth rate fell by 11% compared to 2016. And, according to demographers and sociologists, the decline in the birth rate due to housing problems will be from year to year, threatening a demographic catastrophe, until 2034.

The state is taking measures to facilitate credit housing programs by making housing more affordable, but it is up to the banks to make decisions on the conditions for issuing mortgage loans and lowering the mortgage rate.

Mortgage Development Conditions

The mortgage market in Russia has existed for only 20 years. But due to the characteristic opacity of banking policy, not everyone who wants to purchase housing through a mortgage can do this - there is never confidence in the possibility of paying the next installment, in the stability of the interest rate, there is no guarantee of the reliability of the bank itself.

Since 2010, the legislation began to appear decrees regulating the activities of banks in relation to mortgage lending. Thanks to these regulatory legal conditions, banks cannot:

- Unilaterally change the interest rate on the loan or the term of the loan, unless this is indicated in the contract as a “punishment” for long delays of the borrower.

- Include hidden fees in the contract for consideration and writing of the contract, not provided insurance payments.

- Enter important information in small print in the contract.

- Hide the full cost of the loan.

When concluding a loan in banking institutions, there was a restriction on the amount of the penalty for late repayment of the next payment, which should not exceed the key rate of the Central Bank at the date of signing the loan agreement, that is, it should be unchanged throughout the contract. The Central Bank's key rate is the interest rate at which banks take short-term (1 week) loans. The key rate since July 2017 is 9.25% per annum.

Options for lowering mortgage rates

Mortgage loan payments can be reduced by using several options that you need to carefully study before contacting the bank.

- Mortgage refinancing is a refinancing of a current mortgage loan in a new bank. At the same time, payments may decrease due to the extension of the payment term.

- Restructuring consists in re-issuing the current mortgage loan in the same bank, but with new conditions, in order to ease the mortgage burden of the borrower. In this case, an additional agreement is concluded to the current agreement with fixed agreements on the conditions for further payments on the mortgage or a new loan agreement.

- Social state support is a reduction in mortgage rates to 6% by repaying part of the mortgage payments and down payment from the state subsidy under the Family Mortgage program.

- Appeal to the judiciary is advisable if the bank violates the terms of the mortgage agreement, including unilateral changes in the interest established for the loan for the loan, which do not comply with the orders of the Central Bank of the Russian Federation. In this case, the borrower submits an application to recalculate the total cost and payments on the mortgage, as well as changes in the terms of the mortgage agreement on a mandatory basis by the bank.

To renew the contract in order to lower the mortgage rate, it is best to contact the bank where the salary payments or other payments, deposits, deposits, other accounts with funds on them are made. In such a bank, it is easier to conclude a mortgage agreement on favorable terms, with a reduced mortgage interest rate.

State subsidy "Family mortgage"

At the beginning of 2018, a law on mortgage lending was adopted - a program of preferential subsidies that allows families with children to purchase the necessary high-quality housing on preferential terms. This program stimulates the mortgage market and promotes housing construction. The mortgage rate reduction program in 2018 is valid until 2022, and it is planned to help 500 thousand families in this way in Russia.

The meaning of the program is to provide state support to families whose 2nd, 3rd child is born in the indicated period - this is an opportunity to take a mortgage at 6% per annum. The rest of the mortgage interest to the bank is compensated by the state. An important point is the choice of housing and its cost. According to the program, mortgages are subsidized only in new buildings with a cost not exceeding eight million rubles - for residents of Moscow and St. Petersburg (including the regions of these cities) - and three million rubles - for all other regions. Secondary housing is not subsidized. With a loan that was taken on housing before the start of the program, there is also the possibility of lowering the interest rate on the mortgage, according to the terms of the program.

To obtain a favorable mortgage interest under the state subsidy program, you must contact the banking institutions that participate in the program, the most recognized of which are Sberbank, VTB, AHML.

Mortgage Refinancing

In cases where loan payments become overwhelming due to intractable circumstances arising - salary reduction, temporary incapacity for work, dismissal, it is possible to re-pay the remaining loan amount to another bank, i.e. refinance the existing debt. Such a loan is targeted and should be aimed solely at repaying an existing loan. Mortgage refinancing is offered by many banks in the Russian market, but for the possibility of re-lending, it is necessary to comply with the conditions of banks.

Refinancing is available under the following conditions:

- The age of the borrower is from 21 to 65 years.

- The borrower has no delays in the current loan agreement or similar delays did not exceed 10 days.

- Payments on the current loan were made for at least 6-10 months.

- Until the end of the current contract for more than 6 months.

- The borrower is a citizen of Russia with a permanent place of registration.

- The borrower is employed and legally paid, with at least 1 year experience.

- Monthly loan payments should not exceed 60% of the salary.

- Positive credit history.

Documents for refinancing

For refinancing, it is necessary to submit to the selected bank a document from the creditor bank, the loan in which it is planned to refinance, on the consent to refinancing, as well as the details of this bank, the amount that must be transferred for repayment and information about the borrower's delinquencies. This document is valid for only 3 days, so it must be submitted after choosing a new bank.

The refinancing procedure with the aim of lowering the mortgage interest rate is the transfer of funds from the new bank account to the account at the bank where the loan is closed, and re-registration of the collateral property to the bank where monthly payments under the new agreement will be made.

Such a service is beneficial if the loan was originally taken in foreign currency or at a floating interest rate, which is extremely inconvenient in an unstable economic environment. The costs of completing the refinancing procedure, including a real estate appraiser, certification of documents by a notary, the provision of new certificates, will significantly increase the amount of payments on refinancing. But at the same time, monthly payments on a new loan can be significantly reduced, especially if refinancing combines all credit payments made in the first bank. There can be up to 5 types of such payments.

Debt restructuring

Restructuring of the mortgage allows you to review the individual terms of the contract and adjust it more profitably for the borrower in order to avoid fines, penalties and delays. The revision of the current loan agreement includes questions about lowering the interest rate on the mortgage, deferring payments up to 12 months, the so-called credit holidays, changing the currency of the current loan, increasing the term of the loan agreement, paying only the loan body for a certain period, changing the monthly payments.

To provide such a review, the borrower must write a petition asking for a reduction in interest rates on the current mortgage, as well as convince the bank of the reasons forcing the borrower to ask for loyalty. These reasons include:

- lower wages;

- dismissal;

- birth of children;

- temporary disability.

Restructuring in the end is always more costly, since prolonging the payment term increases the overall overpayment of interest.

Mortgage rate reduction in Sberbank

In the most democratic bank in our country, Sberbank, a program for reducing credit interest payments “Refinancing” is provided. The rate for the program is 13.9% per annum.

The procedure allows you to save significant amounts on long time frames for paying mortgages. Sberbank may change the terms of the mortgage agreement under the terms of the restructuring. To do this, you must submit an application to lower the mortgage rate at Sberbank. At the same time, the maturity can be either prolonged or shortened if the interest rate in the bank is reduced.

How to apply

There are two reliable ways to apply for a lower interest rate on a mortgage. The most standard is to contact the bank office in person, and the most convenient is to fill out an application through the “personal account” function on the website, for example, Sberbank. When filling out an application, it is important to check your credit history, because delays and debts can impede a positive response from the bank.

To fill out an application, you need to find a function in your account to send a message where you can send an application to lower the interest rate on a mortgage. So write the subject of the letter - refinancing a mortgage rate. The letter must be accompanied by a pre-filled application form from the computer desktop with an electronic signature, if any. If there is no electronic signature, then, having filled out and printed the application form for lowering the mortgage rate, sign it, scan and save it. Then send through your account.

You can personally apply for a lower interest rate on a mortgage at Sberbank by asking the manager for an application form. If you have a ready-made form, it will be surely issued, and if there are no forms, then the application can be submitted in any form.

How to fill out an application

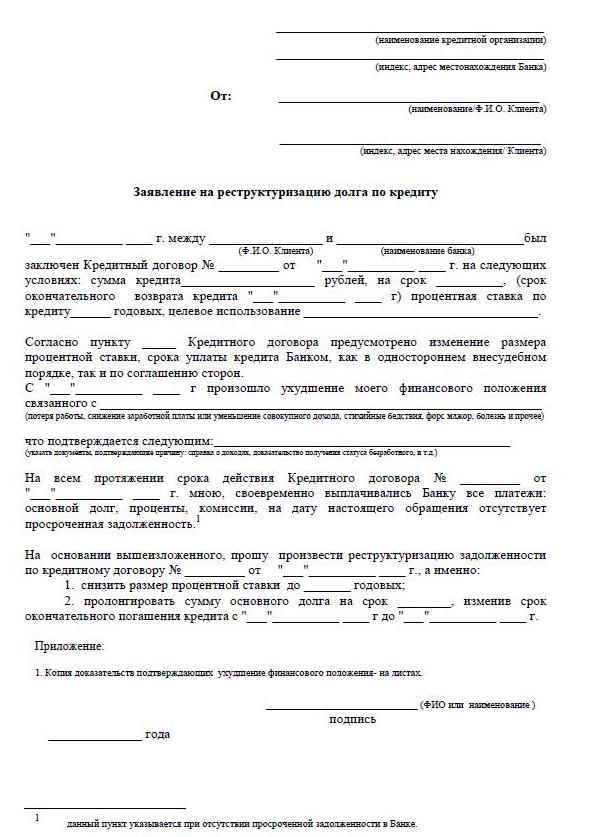

A sample application for lowering the mortgage rate is provided by the employee of the bank, in which it is planned to apply for this issue.

- The application heading indicates where the document is submitted, its full name, passport data: series, number, by whom it was issued and when, the registration address is in the same place.

- Directly under the word "statement" it is indicated that the applicant is a borrower according to the contract - the number and date of signing the contract. Further along the text of the application: “I ask you to lower the interest rate on the mortgage agreement (agreement number, date of signing) for a reason (reason is indicated).”

- It is important to indicate in the application how the bank can give an answer - to notify the decision: in person, by regular mail or e-mail. Indicate address, phone, email. At the end of the application, the date must be fully indicated. and signature.

- For the reliability of your data on the current loan, it is advisable to enclose a copy of the mortgage agreement, an extract on the balance of the debt, a statement of income, an extract from the USRN.

- Consideration of an application to lower the mortgage rate of Sberbank takes 1-1.5 months.

Conditions for amending the contract

In banking organizations, there is a mandatory informing of borrowing customers in case of changes in the interest rate on mortgage lending, in order to provide more affordable conditions for borrowers. Information is made via SMS to mobile phone numbers or in the form of notifications by e-mail or address mail. With a general reduction in the interest rate, by order of the bank management, information is sent out in bulk. But there are cases of loyalty to an individual borrower who carefully pays monthly installments over a long period of time - they individually consider the issue of lowering the interest rate.

When the borrower learns on his own about the possibility of reducing the mortgage rate associated with a change in the program of the lender, the initiative comes from the client-borrower. In this situation, the borrower independently makes a statement to the management regarding a possible reduction in the interest rate on the existing mortgage, receives a decision, then an appropriate additional agreement to the existing agreement with a changed interest rate or an agreement with new conditions is prepared.

The borrower performs an independent analysis of the situation in the mortgage market in his region. And, if there is a decrease in the interest rate on the mortgage, it submits applications to the selected banks for refinancing.