Property - this is the main means, property of the enterprise. Under current law, such an asset is a tax base. Read more about how property tax is accrued, the postings that are used in this operation, read on.

Base

The tax base for organizations is property, which is listed as “Fixed Asset”. For this purpose, accounts 01 and 03 are used in the balance sheet. The tax amount is calculated at the residual value of the object. It is defined as the difference between the accounts “01 (03)” and “02 (10)” Depreciation. The algorithm for calculating and posting property tax is different for different groups of objects. Therefore, consider OS should be in different subaccounts.

Asset groups

There are 4 groups of property:

- property recorded at residual value;

- assets taxed at cadastral value;

- movable property registered until 01.01.13;

- movable property registered after 01/01/13;

The taxation in the BU is not regulated by acts. The process depends on the accounting policies of the company, documented.

Accrual Property Tax Transfer: Postings

The amount of tax can be attributed to any expense account: fixed assets, general business expenses, expenses on sale, etc. How often is accrued organization property tax? The posting for this operation includes account 91-2. It is much easier to check the correctness of the calculations and identify an error when debiting amounts to this account. Consider the main accounting entries:

- accrual of property tax - DT91-2 KT68;

- transfer of withheld amount to the budget - DT68 KT51.

Write-off is carried out quarterly and per year. If an error is detected, the tax amount is adjusted using the income tax account. If the collection amount is overstated, then the amount of expenses is reduced: DT68 KT91. If the fee is reduced, then, together with the additional charge of tax (ДТ99 КТ68), penalty calculation.

Motor vehicles

Until 2013, movable property was taxed according to general rules. After amendments to the law, all movable objects that were registered until 2013 were excluded from taxation. If the object was registered shortly before this date, then, subject to the use of the correct entries, the accountant can postpone the date of registration of the object and reduce the base legally.

First you need to split the vehicle accounting into two subaccounts depending on the date of purchase. It is reflected in the object cards and most often coincides with the day specified in the acceptance certificate. If the object needs installation, then the date of its registration is postponed for the period necessary for the installation. The transactions for calculating property tax do not change at the same time, but the sequence of acceptance of the object for accounting in the accounting office looks different:

- DT08 KT07 - the object was transferred for installation.

- DT01KT08 - the object is registered as an OS.

So that in the future there are no questions from the inspection bodies, it is necessary to supplement these postings with an order on the transfer of property to installation.

Legislative regulation

The regulatory documents spelled out the procedure for calculating and declaring the amount of tax. Accounting rules are determined by each organization individually and are fixed in orders on tax policy. Amounts of tax paid are expensed. Property tax postings depend on the organization.

Expenditure

The amount of the fee should be included in the cost of manufactured products.The organization selects a specific item of expenses on its own. It could be:

- 44 - implementation costs;

- 91-2 - other expenses;

- 20 (23,) - the main (auxiliary) production;

- 25 (26) - overhead (general) expenses.

The use of real estate in the production process serves as the basis for the selection of second-class accounts for cost accounting. Trade organizations use account 44, service providers - 91-2. The last option is simple. Using this account allows you to easily make adjustments in the future.

Fines

For incorrect reflection of the amount of accrued tax, the organization may be fined. The Federal Tax Service checks the correctness of maintaining the control unit and the control unit. Incorrect or untimely postings on the tax on property are grounds for calculating a fine. In the first case, an administrative penalty of 10 thousand rubles is envisaged, for a repeated offense - 30 thousand rubles. If, as a result of an error, the tax calculation base was reduced, then the amount of the fine increases to 40 thousand rubles. Similar amounts shall be presented if the order of reference is violated.

BASIC

When calculating the tax, the amount indicated in the declaration is included in the general expenses. If an entity applies the accrual method, then expenses are recognized on the last day of the quarter (year). If the cash method is used, then expenses are taken into account after tax.

Example

The company works at OSNO. Income tax calculated on an accrual basis. At the end of the year, the tax base amounted to 190 thousand rubles. The rate is 2.2%. Tax amount: 190 * 0.022 = 4.18 thousand rubles.

For the year, the company transferred tax advances to the budget in the amount of:

- for the I quarter. - 1010 rubles .;

- for the second quarter - 810 rubles .;

- for the III quarter. - 870 rub.

For 4 square meters. it is necessary to list: 4180 - 1010 - 810 - 870 = 1490 rubles.

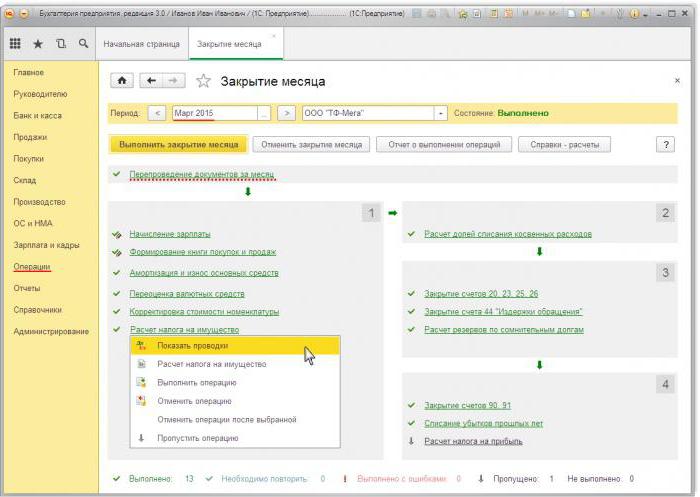

Consider the transactions for the calculation of property tax in 1s 8.2:

- ДТ91-2 КТ68 - 1490 - the tax for 2014 was calculated (12/31/15).

- DT68 KT51 - 1490 - the tax for 2014 was paid (03/26/16).

The amount of the fee is included in other expenses. This condition is provided for by Art. 264 of the Tax Code of the Russian Federation. If the company reimburses the tax to its counterparty, then write it off as expenses, there is no reason. But if reimbursement is stipulated by the terms of the contract, then these expenses can be attributed to non-operating expenses (Article 265 of the Tax Code of the Russian Federation). True, in this case, they will have to defend their rights in court. Conflict situations can be avoided by laying the amount of compensation in a separate payment, for example, the provision of services.

STS

Organizations located on the “simplified system” do not pay tax. An exception are enterprises that have property on the balance sheet for which the base is calculated at the cadastral value. Payment is made on a common basis.

If the company uses the scheme "STS income", then the property tax will not reduce the base. If the scheme "STS income - expenses" is used, then the amount of tax is included in expenses during the period when the funds were transferred to the budget.

UTII

Enterprises located at UTII do not pay property tax. An exception are organizations that have property on the balance sheet for which the base is calculated at the cadastral value. Payment is made on a common basis. The amount of tax base for calculating UTII does not reduce.

Property tax postings in 1s 8.3

To calculate the tax amount in 1C, you need to fill out an OS card. To do this, you first need to capitalize the object with the document “Goods Receipt” with the operation type “Equipment”. The document should indicate the number of objects and the initial amount. As a result of the document, the following transactions are formed: DT08 KT01 and DT19 KT60. Next, you need to create and post a document “Acceptance of the OS for accounting”. This document completes the process of forming the initial cost and puts it into operation. Formed book value can be viewed in the report “SAL in the account” 08.

The tax return is located in the Regulated Reporting Section.To automatically generate data, you need to select a specific report form and click the "Fill" button. The program displays the average cost for the year, and then carries out the accrual. The final amount is reflected in Section 1. If the calculation is made at the cadastral value, the final result is reflected in Section 3.