Based on the data of the primary documentation, overalls are monitored at enterprises with harmful and dangerous working conditions. It is often necessary to purchase an IBE. Therefore, accountants must know how to keep records of workwear. Let us consider in more detail how to draw up documents and conduct operations in 1C.

Providing PPE

Ensuring the preservation of the lives of workers is one of the principles of the declaration of the International Labor Organization and the Universal Declaration of Human Rights. In the Labor Code of the Russian Federation, the obligation of employers to provide normal working conditions for employees is put forward in the first place. According to Art. 210 of the Labor Code of the Russian Federation, one of the main directions of state policy in this area is the provision of protective equipment to employees.

PPE are items used to prevent exposure to harmful production factors. They apply if the safety of work cannot be ensured only by equipment and labor organization.

PPE are divided into:

- insulating suits, spacesuits;

- respiratory protection products such as gas masks and respirators, air masks and masks;

- special clothes: vests, coats, wraps, etc .;

- means for protecting the lower extremities (boots, shoe covers, etc.), upper limbs (gloves, mittens), heads (helmets, hats, berets), faces (shields), eyes (safety glasses), hearing organs (special helmets , headphones);

- means for protection against falling from height;

- dermatological agents.

Safety measures at the enterprise and Art. 221 of the Labor Code of the Russian Federation provide for the procedure for providing employed persons with protective equipment. The employer is obliged to provide the necessary IBE to persons working in hazardous industries and in contaminated premises. It also has the obligation to preserve, wash, dry, disinfect, decontaminate and repair the work clothing. According to Art. 215 of the Labor Code of the Russian Federation, SIZ - even of foreign manufacture - must comply with the requirements of the protection of the Russian Federation and have a quality certificate. Otherwise, they can not be used.

The list and number of required IBEs is presented in the Model Industry Standards. The requirements listed there do not depend on the industry, workshop or site of work. However, according to Art. 221, the employer has the right to limit the standards for the free issuance of PPE by coordinating the matter with the trade union organization and based on its economic situation. This provision applies if the PPE under consideration differs in quality from standard ones and better protects in conditions of harmful production, high temperature conditions and pollution.

In some cases, the employer may, after agreement with the state labor protection inspector and the trade union body, replace one type of PPE, provided for by the Standard Rules, with another that better protects against hazardous production factors. For example, a cotton jumpsuit can be replaced with a suit or dressing gown of the same fabric, or vice versa. A cloth, canvas tarpaulin suit can be replaced with a cotton one with fire-retardant or water-repellent impregnation, leather shoes can be changed to rubber, half boots made of artificial leather - to tarpaulin. The rubberized apron is changed to a product made of polymeric materials, mittens - to gloves. In the same way, you can replace the material and use gloves made of polymer materials instead of rubber products to protect your hands.

PPE such as a safety belt, dielectric gloves, galoshes, rug, glasses, shields, gas mask, respirator, helmet, mosquito net, shoulders, helmet, elbow pads, caps, antiphones, helmets, light filters and other items not specified in the Model Norms may be issued to employees after preliminary certification of jobs. The nature of the work performed is investigated, and the period of use is determined - until complete wear or as spare.

The personal protective equipment issued to employees must correspond to them in terms of height, gender, size, and the conditions of the work performed. Duty protective equipment provided for by the Standard Norms should be provided to employees exclusively for the duration of the work for which they were originally intended. Such IBEs can be assigned to individual jobs. For example, sheepskin coats can be used at outdoor posts, dielectric gloves - when working on electrical installations, etc. Such PPE will be transferred between shifts, and the masters are responsible for their use.

Warm overalls and shoes (warming suits, jackets, trousers, sheepskin coats, boots, earflaps, mittens, etc.) should be issued with the onset of cold weather, and in the warm season should be surrendered for storage until the next season. The time to use such clothing is set by the employer, together with the union and the body dealing with climate conditions.

Individuals who combine professions or constantly perform several types of work, including as part of brigades, in addition to the main ones, should be given PPE depending on the type of activity.

BOO

Accounting for workwear in the balance sheet is carried out at the actual cost of its purchase or manufacture. If the enterprise uses the IBE of its own production, then the costs of their manufacture are grouped first on the accounts of production costs. Upon issue, the cost is calculated, which includes all costs. Ready-made workwear is sent to the warehouse by the “Act of Completed Works”. In the control unit, the posting DT23 KT10 is formed for the amount of manufacturing costs. Analytical accounting should be kept as detailed as possible, indicating the quantity, name, date of receipt and return, financially responsible persons.

In BU, the cost of the IBE is debited one-time or linearly. The first method can be applied if the service life of the item does not exceed 12 months, and the second for longer-term IBEs. More details on the decommissioning of workwear will be discussed later.

Options

Overalls are usually considered as part of inventories. But if its value exceeds 40 thousand rubles, and the period of use exceeds 12 months, then it comes into the OS. The selected option must be written in the order on the accounting policies of the organization.

The purchase of workwear

If the purchased goods are accounted for as part of the OS, then they should be received on account 10. It is indicated on the “Materials” tab in 1C program. It is also necessary to allocate a separate sub-account “Overalls in stock”. The receipt of goods in the program is carried out on the basis of a receipt order. You can use a unified form or develop your own form and indicate in it all the necessary details.

Example

The conditional LLC, engaged in the transportation of goods, in February 2016 acquired 10 vests for driver’s cars at a cost of 159.3 rubles. per pc The total purchase price amounted to 1,593 rubles. According to the Model Standards, the period of use of vests is one year. In this case, overalls in accounting will be accounted for as part of the IBE.

LLC (name)

PKO dated 02.28.16 No. 15

| Material value | unit of measurement | Qty | Price without VAT, rub. | Amount without VAT, rub. | VAT | ||

| Name | Item Number | Rate | Amount, rub. | ||||

| Vest | 3202 | PC. | 10 | 135,00 | 1350,00 | 18 % | 243,00 |

Postings in accounting:

- DT10 sub-account “Overalls” KT60 - 1 350 rubles. - the cost of workwear (excluding VAT).

- DT19 KT60 - 243 rubles. - input VAT.

- DT68 “VAT calculation” KT19 - 243 rubles.- accepted for deduction of VAT.

- DT60 KT51 - 1,593 rubles. - funds are listed to the supplier.

Accounting for the issuance of workwear

Distribution of purchased goods should be based on the primary document. Its form must comply with the requirements of tax and accounting. If a decision is made to use a unified form, then to account for issuance, you can apply a bill of lading (No. M-11), or a bill of lading for goods (No. M-15), or a limit-fence card (No. M-8). And you can draw up your document based on any of the above.

The head of the unit distributes the purchased goods, and the accountant must draw up a statement of the issuance of workwear. It is best to generate this document once a month or year for all employees. You can use such a sample.

LLC (name)

Statement of issue of overalls for 2015

| No. p / p | Full name | Overalls | Units meas. | Quantity, pcs. | Amount without VAT, thousand rubles | date of issue | Life time | return date | |

| Name | Nomencl. | ||||||||

| 1 | Ivanov | Suit | 1840 | PC. | 1 | 1 | 01.09.15 | 1 year | |

| 2 | Petrov | Jacket | 1837 | PC. | 1 | 2,5 | 01.09.15 | 1 year | |

You can insert any lines into your own form. For example, record the return of workwear before the employee is fired. This statement will be considered a register.

The fact of the issuance of workwear should be displayed on account 10. The posting will show the movement of workwear from the sub-account “In stock” to the sub-account “In operation”. Write-off of work clothes is carried out at the same time or evenly upon the fact of their issuance to employees. The cost is included in the production costs of the enterprise.

Example

We supplement the conditions of the previous example. Safety measures at the enterprise provide for the use of vests by transport service employees. The storekeeper of the conditional LLC issued these IBEs on March 17. The movement of overalls between units is made out by the requirement-invoice. The issuance of vests to drivers is recorded in the statement. According to these primary documents, the accountant makes entries in the balance sheet:

DT10 sub-account “Overalls in operation” KT10 sub-account “Overalls in stock”

- 1,080 rubles — moving the IBE to the unit.

Documents from accountable persons in accounting were at the end of the month. Accounting policies it is stipulated that IBEs with a term of use of up to 12 months are written off at a time. In the BU, the following entries are made:

DT20 KT10 - 1080 rubles. - write-off of work clothes at the expense of the enterprise.

DT012 "Overalls in operation" - 1080 rubles. - issuance of IBE to employees.

Return IBE to the warehouse

Most often, workwear is the property of the company. The employee receives it for temporary use, and in case of dismissal or a change of position returns it to the warehouse. This operation must be reflected in accounting.

There is no need to create a separate document. The developed workwear accounting card may contain lines in which the fact of the return of the IBE will be reflected. How to reflect the operation in accounting? If overalls are expensed in full, additional postings are not necessary. If part of the cost is listed on account 10, then you need to make an additional entry, transfer the IBE from the sub-account “Overalls in operation” to the sub-account “Overalls in stock”. The rest of the cost is not written off, since only IBEs that are in operation can be attributed to expenses.

Accounting for workwear in NU is not reflected. IBEs are written off as expenses when calculating NPP at a time. This occurs at the time of transfer of work clothing to the employee. Worn out MBPs are subject to write-off. But this operation is formalized in a separate act.

IBE write-off limits

The Russian Ministry of Labor has developed workwear standards, but only for certain industries, for example, for enterprises in the electrical industry. Other organizations may use the Model Standards for the Distribution of Clothing.

In addition, enterprises can take into account all the costs of acquiring and maintaining the IBE, including in excess of established norms. This does not contradict the Tax Code of the Russian Federation or the Labor Code of the Russian Federation.But first you need to approve the developed calculation rules by an internal order of the head.

But it is impossible to write off low-value and wearing objects according to norms lower than legislative ones. This is contrary to Art. 221 of the Labor Code of the Russian Federation. If the rules provide for three pairs of gloves per year for one employee, then you cannot give him two pairs. For such violations, a fine is provided. Additional costs of the enterprise can be 30-50 thousand rubles, and the head - 1-5 thousand rubles. In the case of a gross violation of standards, the labor inspectorate may stop the activity of the enterprise for 90 days.

The nuances of taxation

Accounting for workwear is carried out without VAT. These IBEs are issued for a time, and not transferred to the ownership of employees. That is, there is no transfer of ownership. The tax authorities will not argue with this. The situation is different if the employee paid money for workwear. For example, upon dismissal, he paid to the cashier its residual value. In such a situation, one must either accrue VAT or refer to FAS Decision No. 2901/2008. The employee paid compensation to the company, but did not buy workwear. It is not necessary to charge insurance premiums on the value of the IBE, provided that it has been transferred to employees for use and not for ownership.

Accounting for overalls, which is subject to decommissioning, in NU is carried out differently than in accounting. IBEs with a cost of less than 10 thousand rubles, which can be used up to 12 months, are included in material costs. The costs of their acquisition are indirect and are written off in full at the time of issue. Overalls, the cost of which exceeds 10 thousand rubles, and the service life is more than one year, is included in the depreciable property and repaid in a linear manner.

Accounting for workwear in 1C

The acquisition of IBE is carried out by the document “Goods Receipt” with the type of operation “Purchase”. To add a nomenclature item to a document, you need to enter a new element in the “Nomenclature” in the “Overalls” or “Special equipment” group, indicate the quantity and account of “10”.

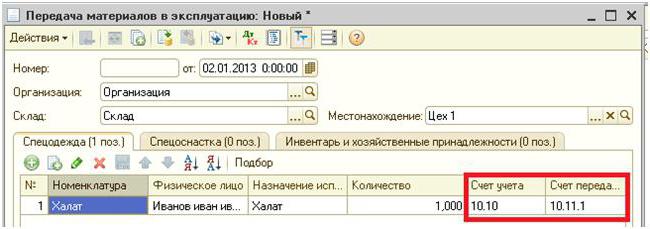

The next stage is the transfer of the IBE into operation for production. This operation is carried out in the program by the document “Material Transfer”. It indicates the individual to whom the BCH is provided. To drive a special gear transmission, you need to select the bookmark of the same name in the same document.

In contrast to the example considered before, the equipment is not transferred to an individual, but to a specific workshop. It is driven into the “Location” field. The same document indicates the method of writing off the value of the IBE: at a time at the time of transfer or in equal installments. For these purposes, the requisite "Intended use" is provided. Basically, decommissioning of IBE is carried out at the time of their transfer to operation. All costs are borne by the production costs of the current period. The requisite “Quantity according to the standard” is filled in, so that at the time of transfer of the IBE by another document, the number of workwear will be substituted automatically.

The repayment order of the IBE depends on the period of operation. If it exceeds one year, then in BU and NU the cost of workwear is charged to material costs. Only in the first case the linear method will be selected.

The special feature of special equipment is that it cannot be attributed to the OS if the cost of the latter is less than 40 thousand rubles. It is written off either in proportion to the volume of work performed, or linearly. In the first case, you need to monthly create a document “Development of IBE and materials” and register the quantity of manufactured products in it.

The debit of the posting to which the IBE will be debited is substituted with the data indicated in the requisite “Reflection of expenses”: account 20 or 25, unit, cost item and item group. The amount on the off-balance accounts 10.11 and 10.10 falls after holding documents.

Write-off of the cost of workwear

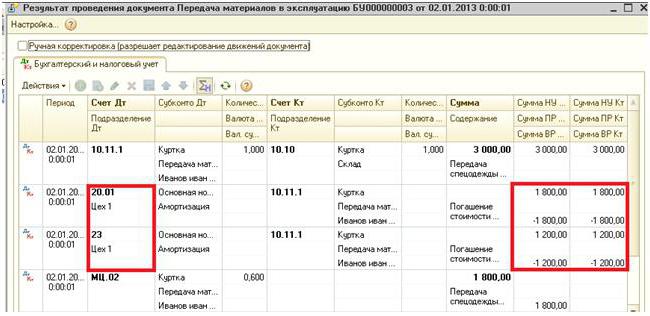

If during the transfer of the IBE it is necessary to remove them from the balance sheet, then when creating the document for the movement of materials, the corresponding transactions should be indicated. If the cost is alienated throughout the entire period of use of workwear, then the transactions are indicated at the end of the reporting period at the end of the month. For these purposes, a separate register “Repayment of the cost of workwear” is provided. He forms the record DT score 20.01 CT score 10.11.

Decommissioning of special equipment is carried out by the document “Write-off of materials”. It is introduced on the basis of the “Transfer of Materials” or separately. In the first case, all fields are substituted from the base document, in the second - they need to be driven in separately or filled in with the "Selection" button. Additionally, in the “Location” field, the workshop from which the special equipment is being displayed is indicated.

The tab “Write-off of expenses” is filled in if the cost of the IBE is not fully paid off. By default, costs will be credited to the debit of the account specified in the main part of the document. You can select the second type of write-off and drive a separate account.