Taxes are the most important tool of the country's economic system. They constitute the largest share of the state budget. Therefore, they are given special attention in form of control and regular legislative changes. The Tax Code of the Russian Federation defines various types of taxes, both for the population and for organizations. For the latter, VAT is of particular importance in the process of purchases and sales. Therefore, any existing or just beginning entrepreneur needs to know what VAT is, the features of its calculation and the procedure for payment.

The concept of VAT

The basic law governing the process of charging and paying fees is the Tax Code of the Russian Federation. It is he who defines the concept, essence and features of the calculation of all taxes in the country, including VAT.

Value added tax is a fee levied on organizations as a percentage of the amount of the increase in value. This increase in value is generated through the difference between revenue and material costs that come from third parties.

The legislation establishes certain types of activities or varieties of products and services for which VAT is partially or completely not subject to calculation. There are also sum limitations on the tax base established by the Tax Code of the Russian Federation and allowing to relieve the company of taxpayer duties.

In addition to determining what VAT is and the restrictions on its payment, the Tax Code of the Russian Federation assigns the fee to a specific tax group. For example, to a species such as indirect taxes. The reason for this is the inclusion of its amount in the price of products sold as a percentage. As a result, when paying VAT, the names of the actual and legal payers differ.

VAT functions

In a market economy and a rational tax system, all types of taxes have four significant functions:

- Fiscal.

- Economic.

- Stimulating.

- Distribution.

For VAT, the fiscal function is manifested in the maximum amount of budget revenues from its calculation due to the stable tax base and acceptable calculation conditions. Of the budget formed from taxes, the majority is accumulated from VAT. The tax also affects the regulation of economic processes. Its rates are involved in pricing and inflation.

Thanks to the establishment of benefits for certain types of activities or specific products, the state is able to stimulate the development of the social sphere, as well as the export of various goods.

Accordingly, the distributional nature of VAT lies in its participation in the redistribution of state GDP. The total amount of tax deductions collected in the budget from successful types of activities is distributed and allocated to support unprofitable sectors of the economy that are significant for society.

VAT payers

The Tax Code of the Russian Federation establishes an extensive circle of persons obliged to pay VAT. The tax is subject to levy on legal entities:

- Enterprises - regardless of the form of activity performing taxable operations: state, municipal institutions, business partnerships and others.

- Persons recognized as taxpayers due to the movement of products through the customs of the Russian Federation. These are organizations with foreign investment or completely foreign enterprises.

Since 2001, individual entrepreneurs engaged in taxable transactions have been equated with enterprises in the obligation to pay VAT with tax legislation.

All persons from the list are registered as VAT taxpayers if they work according to the general taxation system. It happens that with other accounting systems you have to pay value added tax.

Object of taxation

The following categories and transactions are considered to be an object of taxation when calculating VAT:

- Turnovers received from the sale of product activities, as well as sales at no cost.

- Transfer of goods within a Russian organization between its divisions for their own needs, the costs of which were not taken into account in the calculation taxable income.

- The results of construction operations for their own needs.

- Export of goods through the customs border of the Russian Federation.

The calculation of value added tax involves accounting for the following types of sales that are subject to VAT:

- Sale of goods from the organization to another company or individual, even in the absence of shipment and transportation.

- Transfer of products manufactured to order.

- Sale of commission or auction products.

- Exchange of products or materials.

- Gratuitous transfer of products or with partial payment.

- Transfer or sale of property rights.

- Sale of collateral.

The tax base

The VAT return provides for the calculation of the tax calculation of the tax base. Namely, an indicator of the value of transactions subject to VAT. The determination of the tax base for calculating the charge under consideration has a number of features, and primarily depends on the type of operation.

The tax base formed on the basis of the definition of what VAT is, and has a sequence of the following conditions:

- The tax base is equal to the proceeds from the sale of products or property rights, which is determined by the sum of all income related to settlements on these operations. It can be displayed in any equivalent, including in securities.

- A tax base equal to revenue in foreign currencies converted to Russian rubles at the current rate.

- The base under consideration, upon receipt of an advance payment included in it earlier, represents the value of goods calculated on the basis of prices.

- The tax base of the commission or commission agreement is equal to the amount of the fee. There is still a condition.

- The tax base for the sale of a full enterprise is equal to the value of each asset.

Tax rates

In order to calculate the amount payable, the tax base of VAT must first be correctly determined. The tax rate does not depend on the base and is fixed in the Tax Code of the Russian Federation. More precisely, the legislation currently sets the levied rates: 0%, 10% and 18%.

Types of products, the proceeds of which are taxed at a rate of 0%, are fixed in article 164 of the Tax Code of the Russian Federation and have a fairly extensive list of transfers. Basically, these are special varieties of goods, highly specialized works and services.

At a rate of 10%, VAT is charged on the sale of the following product groups:

- Food products.

- Children's goods.

- Periodicals.

- Literature of educational and scientific importance.

- Medical items.

The main sales operations, with the exception of goods taxed at 0% and 10% rates, are subject to tax accounting for multiplication by 18%.

Tax benefits

When calculating the tax base, the legislation defines benefits, in particular activities and products that are not subject to VAT. The collection rate does not apply in the following cases.

- Many types of medical services, including paid ones.

- Educational and cultural services.

- The implementation of residential buildings.

- Disabled goods.

- Property repurchased for privatization.

- Funeral services.

- Insurance operations.

- Transactions with which state duty is paid.

- Photocopy and photocopy.

- Sales of handicrafts.

- Research work at the expense of budgetary funds.

- Repair of household appliances during the warranty period.

Features of the calculation

The calculation of the amount of VAT to be paid has a fairly simple algorithm of actions. The tax base is initially determined. Subsequently, it is multiplied by the set rate. It should be remembered that the timing of VAT payment and the calculation period vary. The amount of tax to be paid to the general budget is calculated based on the results of each month or quarter.

After determining the amount of tax payable, it is necessary to reduce it by the result of tax deductions, if any. What it is? Tax deductions are the amounts of VAT presented to the payer for operations that are involved in calculating the fee. The VAT tax return provides an indication of these deductions and the amount of the difference between the VAT exhibited and the VAT presented.

Payment Procedure

Payment of calculated VAT amounts is based on accounting and tax calculations. It is determined by the results of each reporting period. Terms of payment of VAT established by tax legislation, are defined as no later than the 25th day of the month following the end of the reporting period.

VAT reporting

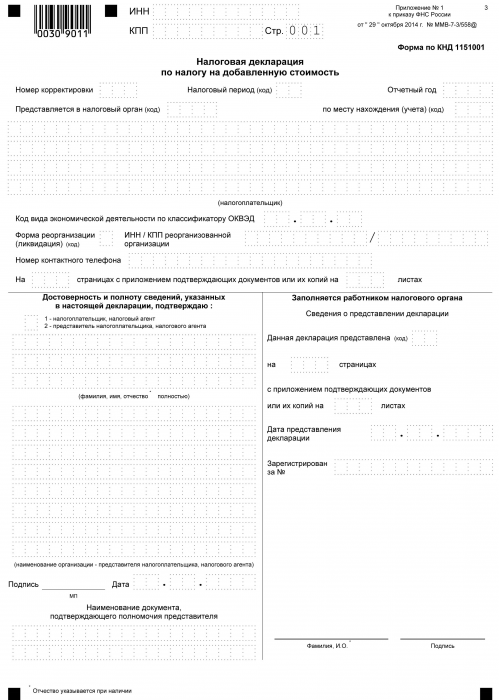

From the time the tax is paid to the state treasury and until the day of payment, each taxpayer working with VAT must report to the appropriate authority throughout the calculation procedure in the form of a declaration. This document is submitted quarterly. It indicates the details of the organization, the amount of calculation of the tax base, the type of rate charged and value added tax. The declaration form is a unified form approved in 2014. At the same time, it is important to know that since 2015 all organizations, regardless of the volume and types of production, are required to file a declaration in electronic form.

When defining the concept of what VAT is, the idea is formed that it is revenue multiplied by a certain percentage. In fact, this is so. But VAT is the sum of the increase in value. And therefore, when calculating it, it is required to take into account many nuances:

- Types of products, both taxable and non-taxable.

- The size of the tax rate.

- The moment of determining the tax base.

- Tax deductions and much more.