When a legal entity has available free financial resources, it has several ways of using them. You can create a reserve fund, you can spend them on the purchase of new, more modern equipment or invest them in another company. The latter option is called “financial investments in development” or, in other words, “investments”. This will be discussed later.

The role of financial investment

Investing your money in someone else's business is always risky. Before deciding to take such a step, you need to carefully study the market, the position of the company on it, what are its prospects and problems. If this is a new idea, then, of course, a business plan is considered in detail, forecasts and the time frame for a refund are analyzed. Sometimes in this difficult issue, one cannot do without the help of specialists who will assess the degree of risk and offer the most profitable options.

In any case, financial investment is the engine of progress. The larger the investment (no matter in which sphere), the more chances there are to improve, which means to increase your competitiveness, market position, quality of goods, wages and salaries to employees and so on in the chain. The most developed countries with a high standard of living are those that other states trust in their finances.

What can be attributed to financial investments

In accounting, it is considered that financial investments are:

- Securities issued by state or relevant municipal authorities.

- Securities of third parties, on which the maturity date and value with interest must be affixed.

- These may be simple contributions from other companies, even subsidiaries.

- Financial investments are loans from one organization to another.

- Deposits in banks.

- Contributions to the authorized capital of partnerships.

Conditions for the existence of financial investments

Accounting for financial investments in accounting will be carried out if certain conditions are met. Firstly, it is necessary to provide officially executed and signed documents proving the receipt of funds and obliging them to be returned with interest.

Secondly, any organization providing investments should understand that together with loans it receives financial risks:

- price increases and depreciation of money;

- insolvency of the debtor;

- bankruptcy announcements of a borrowing company, etc.

And the third condition, which financial investments must meet: they must bring economic benefits to the organization. Usually it is expressed as future income and takes the form of a percentage of the invested amount.

What can not be attributed to financial investments

Financial loans include various loans, but you need to clearly understand what securities may mislead accountants and considered investments, although they are not. The law clearly spells out what cannot be considered financial investments:

- Shares issued by the entity for resale or cancellation.

- Settlement for goods or services with a partner with a bill of exchange.

- Any investment in the development of your own enterprise. For example, the allocation of money to upgrade equipment or intangible assets that are the subject of a loan.

- Any precious items, antique items that are not the subject of the main activity.

Types of financial investments

There are several ways to classify investments. The most popular such division into groups:

- With respect to installation capital, financial investments can either form it or not touch it at all.For example, stocks and investment certificates are issued for the formation or replenishment of fixed capital, but bonds, savings certificates have nothing to do with it.

- The form of ownership may be public or private.

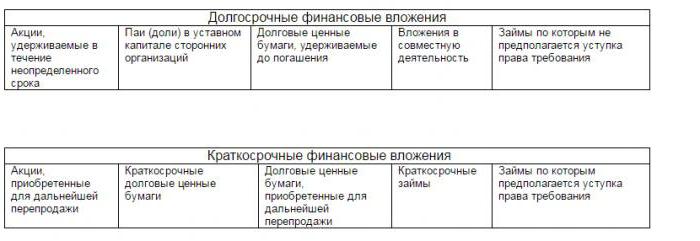

- Maturity also matters: long-term ones can last more than one year, short-term ones can last only up to 12 months. Examples of such financial investments are presented in the figure.

Types of Securities

Another important point is to understand what securities may be considered to be financial investments.

This is primarily a stock. Represents a security issued by an entity with the intent of formation of authorized capital. The owner of the share is entitled to receive dividends, that is, interest on profits, and may participate in general meetings for making managerial decisions.

The main debt obligation is a bill of exchange. This is a financial instrument with which you can manage the debtor, indicating how much and by what date he should pay the creditor.

Bond. Most often it is issued by state bodies. It has an initial price that the debtor must reimburse by repurchasing the bond. In addition, he is required to pay a fixed percentage for the right to own or use the bond.

Savings certificate - issued by credit organizations and indicates the opening of a deposit.

Accounts for accounting for financial investments

Accounting for financial investments should be displayed on the accounts. According to the regulatory documentation, the active account for displaying cash flows is 58 “Financial investments”. To display more specific operations, sub-accounts are opened:

- 58.1 - "Units and shares".

- 58.2 - "Debt securities".

- 58.3 - "Debt loans" (passive subaccount).

- 58.4 - "Deposits under the partnership agreement".

Primary value formation

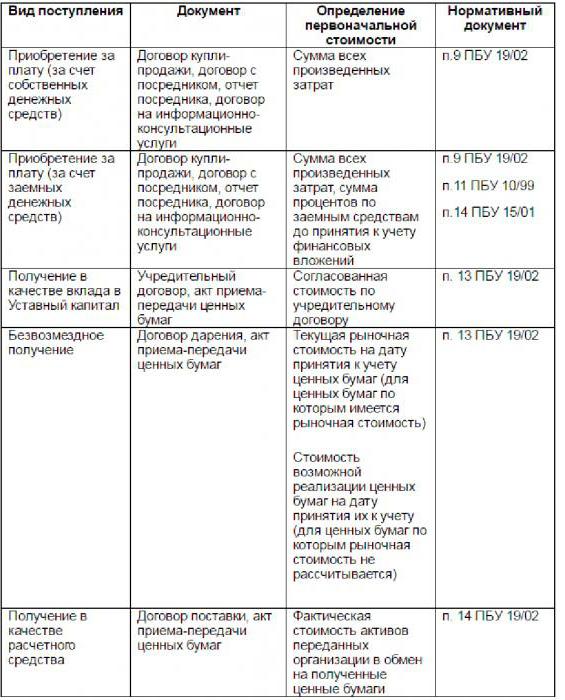

When an enterprise receives cash investments, the question arises of how to correctly evaluate them and on which balance to count. In many respects it depends on the sources of income. They can be different: purchase of securities, receipt of investments in the authorized capital, donation, payment order for goods delivered or services rendered, etc. The organization’s financial investments and initial cost estimation methods, depending on the source of receipt, are presented on the picture.

Any financial investment in the form of securities must be accepted by the organization in accordance with the norms and requirements. The document must have the following components:

- name of the company that issued the paper, name, series, document number and other details identifying it;

- nominal cost, the amount paid upon purchase and other expenses that may be associated with the acquisition;

- number of documents;

- date, month and year of acquisition, storage location.

Financial investment is an extremely important source of investment, which is a real engine of progress.