The tax code establishes certain requirements for entities receiving income. The legislation, in particular, stipulates the obligation to pay mandatory contributions to the budget from income that is subject to taxation. To ensure control of tax payments, authorized bodies require entities to provide official documents. They contain information not only about the income received, but also about the amounts of the accrued, withheld and paid fee. Regulatory acts approved unified forms of such documents.

Legislators periodically review current regulations. Since 2016, document 6-NDFL has been introduced - new reporting for all employers. It is provided not only by entities that have employees, but also enterprises that pay income to persons who are not their employees. Making entries in this document is currently accompanied by a number of difficulties. First of all, they are associated with insufficiently complete explanations given in the regulatory acts of the Federal Tax Service. Nevertheless, all enterprises need to deal with the new order. Consider further what constitutes a document 6-personal income tax.

New reporting for all employers

The order of execution, the description of the required format for the presentation of the document in electronic form is explained in Order of 14.10.15 No. MMV-7-11 / 450. However, this regulatory act does not answer all the questions that arose with the payers. Document 6-NDFL, the form of which is presented in the article, is compiled throughout the company or the enterprise as a whole. Many organizations use online services or special programs to simplify the process.

Where is the document provided?

It is sent to the same control body, where the tax itself is transferred. 6-personal income tax is provided:

- Russian organizations with separate divisions to the inspectorate at the location of these structural divisions.

- By individual entrepreneurs registered at the address of the activity and applying the patent system or UTII, to the control service at the place of registration.

- Large payers - to the inspection at the place of registration or registration of the relevant branch.

In what form is the document presented?

Those who pass the 6-personal income tax can send it by registered letter or present it in person to the inspection on paper. Such options are suitable for those business entities in which the average number of employees who received income in the corresponding period is less than 25 people. Other, larger enterprises should be provided with the calculation of 6-personal income tax in electronic form.

When do I need to send a document?

First of all, it is worth saying that the legislation provides for liability for the late provision of 6-personal income tax. The deadlines for sending the document are as follows:

- For 2016 - April 1, 2017

- For 9 months 2016 - October 31, 2016

- For the half year - August 1, 2016

- For the 1st quarter - May 3, 2016

The penalty for violation of the established periods is 1 thousand rubles. for every month. In addition, the control service has the right to freeze the settlement account of the enterprise if the delay in providing the document is more than 10 days. If form 6-NDFL contains false information, the fine will be 500 rubles. for every paper. It should also be borne in mind that if the date on which the documentation is required is the same as a holiday or a weekend, then the deadline is transferred to the next business day.

6-PIT: form

The Order mentioned above clarifies the main points regarding the preparation of the document. There are a number of requirements for the payer when applying for 6-personal income tax. The sample is compiled:

- In accordance with the data present in the accounting registers. These include, in particular, accrued and paid income, deductions granted, calculated and withheld tax.

- Progressive total. This means that at first the information is summarized for the first quarter, then - for the half year, after that - for 9 months. and for the entire calendar year.

Not all information that needs to be entered is always placed on one page. In this case, as many sheets as necessary are drawn up. Total indicators are reflected in such cases on the last page. Moreover, all sheets, starting with the title page, must contain the numbering ("001", "002", etc.).

Important point

Those who pass 6-personal income tax should be aware of the prohibitions regarding the processing of the document. In particular, it is not allowed:

- Correction of errors using corrective tools.

- Print on two sides of the same sheet.

- Binding pages, leading to damage to the document.

Filling of 6-NDFL is carried out with ink of violet, black or blue color. If the document is compiled on a computer, the Courier New font is used, the size of the letters is 16-18 pt.

Features record indicators

The following rules are established:

- Each parameter corresponds to one specific field. It consists of a fixed number of familiarity.

- Enter only 1 indicator in each field. An exception to this rule are parameters whose value is indicated as a decimal fraction or date. To record the latter, 3 fields are used in order: day (two familiarity), month (2 cells), year (four cells). They are separated by a dot. The decimal is indicated in two fields. They are also separated by a dot. The whole field fits into the first field, the fractional part fits into the second.

- Form 6-NDFL must contain sum indicators and details. If there are no values, the first is zero ("0").

- Numeric and text graphs must be filled from left to right from the extreme cell or from the edge of the field intended to indicate the value of the indicator. If for any parameter it is not necessary to use all the familiarities, a blank is put in blank sections. A similar rule applies to decimal fractions (for example, 123 ------. 60).

- Calculation and indication of personal income tax is carried out in full rubles. In this case, rounding rules apply (less than 50 kopecks. Is discarded, and 50 and more kopecks - should be rounded to the full ruble upward).

- The declaration of 6-personal income tax is compiled for each OKTMO.

- On each sheet in a designated field should be put the number of compilation and signature.

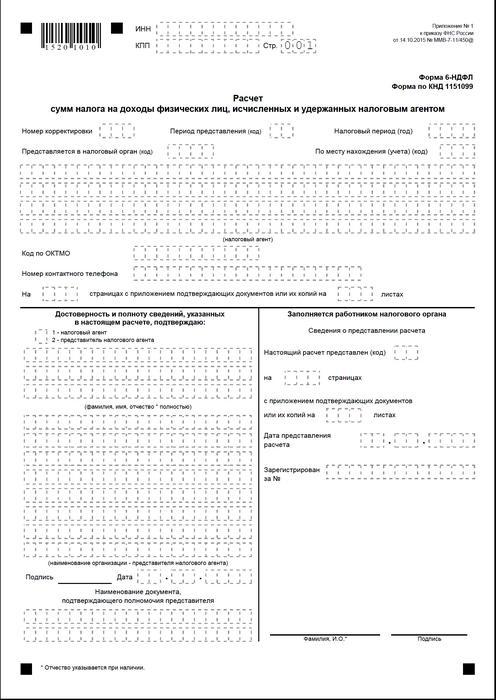

Title page

Form 6-NDFL contains the following fields:

- "INN". Individual entrepreneurs must indicate the information in accordance with their certificate of registration with the inspection. For organizations, the TIN consists of ten digits. In this regard, dashes are placed in the last two cells of the field: 1234567890--.

- "PPC". Individual entrepreneurs do not fill out this field. Legal entities indicate the checkpoint obtained at the IFTS. 6-NDFL for separate divisions contains the accounting code in the inspection at their location.

- "Adjustment number." If the quarterly form of 6-personal income tax is submitted for the first time, put "000", if the first correction - "001", the second - "002" and so on.

- "Submission Period". The code of the time period for which 6-NDFL reporting is provided is indicated here.

- "Provided to the authority." In this field, the code of the service to which the document is sent.

- "Taxable period". This line contains the year for which the information was provided (for example, 2016).

- "By location / accounting." The appropriate code should be indicated in this column.

- "Tax agent". Organizations should enter their full name according to the constituent documentation.Individual entrepreneurs line by line indicate the surname, name and patronymic.

- OKTMO Code. Organizations should enter information at the location or location of a separate structural unit. Individual entrepreneurs need to specify the OKTMO code at the address of residence. Individual entrepreneurs who use the patent system or UTII enter information in accordance with the municipality in which they are registered as payers of these contributions.

- "Contact number". In this field you must specify the number by which the control service can contact the payer.

- "On the pages." The number of sheets that make up the 6-NDFL form (for example, “003”) is indicated here.

- "With attachment of supporting documentation and copies." This column indicates the number of sheets that are attached to 6-personal income tax.

The sample document also contains a block confirming the completeness and reliability of the data. Let's consider it in more detail.

Confirmation block

In the first field, the IP should be set to "1", and the organization - "2". The remaining columns of the confirmation block indicate:

- Line by line head in the appropriate fields, if the document is provided by the organization. After that, the director of the legal entity puts the date and signature.

- Line by line representative of the enterprise, if the document is presented by an individual. After that, the subject puts his signature and date of compilation. In addition, he indicates the name of the document, which confirms his authority.

- Signature and date of compilation, if form 6-NDFL is provided by an individual entrepreneur.

- Line by line an authorized natural person of an organization acting as a representative of a legal entity in respect of which a document has been drawn up. In addition, the name of the company whose employee is this entity is indicated, as well as a document confirming his authority.

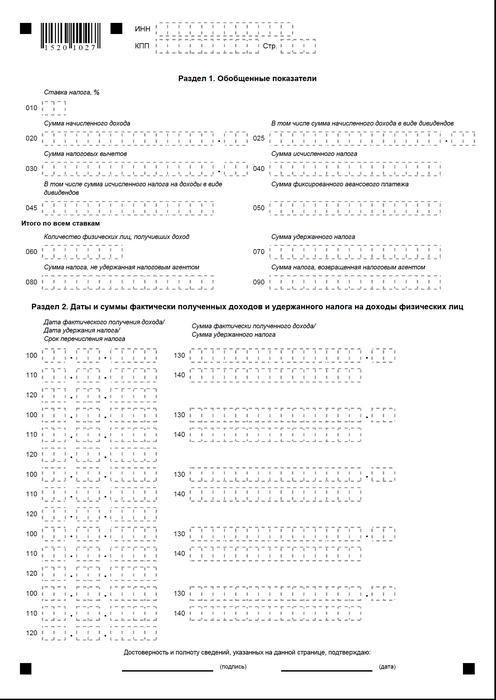

Section 1

6-personal income tax on the simplified tax system is compiled for all employees cumulatively from the beginning of the period at the corresponding rate. In the event that the income was paid at different rates, then the Section should be drawn up separately for each of them. The exception is lines 060-090. If all the required indicators cannot be placed on one sheet, as many pages as necessary are compiled. The total rates for bets (p. 060-090) fit on the first page. Help 6-PIT contains the lines:

- 010. It indicates the personal income tax rate.

- 020. It gives the amount of accrued remuneration for all employees on an accrual basis from the beginning of the period.

- 030. Here the generalized amount of the deductions provided is indicated, which reduces the income subject to tax. It is given cumulatively from the beginning of the period.

- 040. This line should contain the summarized amount of tax calculated for all employees. The value is indicated by the cumulative total from the beginning of the period.

- 045. This line contains the generalized amount of the accrued tax in the form of dividends. The amount is given on an accrual basis from the beginning of the period.

- 050. This line indicates the amount of fixed advances for all employees. It is taken to reduce the value of accrued personal income tax from the beginning of the period.

- 060. This line should indicate the total number of employees who received taxable income in the reporting period. When dismissing and hiring for one time period of the same employee, the number of employees is not adjusted.

- 070. This line indicates the total amount of tax that has been withheld. It is recorded on an accrual basis from the very beginning of the period.

- 080. This line should indicate the total amount of tax that was not withheld by the agent.

- 090. Here is recorded the amount of tax that the agent returned to the payers under Art. 231 Tax Code.

Section 2

It should indicate the numbers on which the employee actually received income, and mandatory deductions to the budget were withheld from them.Section 2 should also include the terms of the transfer, as well as summarized information for all employees about the remuneration paid to them and withheld amounts. In this block I have the following lines:

- 100. It should indicate the date on which the revenues reflected in p. 130 were actually received.

- 110. Here is indicated the number on which the deduction of the obligatory payment to the budget was made from the actually received income reflected in p. 130.

- 120. This line indicates the date no later than which the amount of tax should be transferred.

- 130. Here they give the amount of income received actually on the date indicated in p. 100. Moreover, the deducted tax is not deducted from it.

140. The generalized amount of the obligatory payment withheld on the date indicated on page 110 is written on this line. If different payment periods are set for incomes of different types, but having the same number of actual receipt, lines 100-140 should be drawn up separately for each transfer date . If income was not paid to employees and no deduction was made from them, the document must still be submitted to the supervisory authority. In this case, the indicators will be zero.

Example

In the first quarter of 2016, LLC accrued earnings to 19 employees. In accordance with labor contracts, remuneration is paid monthly on the 10th day. The tax rate that applies to income is 13%. The date of the actual receipt of earnings is the last day of the month for which it is accrued. This provision is given in Art. 223, paragraph 2, para. 2 Tax Code. Withholding tax from the income of the payer is necessary at the time of their actual payment - the 10th. This requirement is established by Art. 226, paragraph 4 of the Tax Code. Transfer of tax to the budget should be carried out no later than the day that follows the day the salary is issued, that is, no later than the 11th. 6-personal income tax is compiled for the first quarter:

For January:

- The amount of salary accrued to employees - 1,450,300 rubles.

- Personal income tax - 188 539 p.

- The date on which the income was actually received is January 31st.

- The date the tax was withheld is February 10th.

- The latest date for the transfer of personal income tax to the budget is 02/11/2016.

For February:

- The amount of income accrued to employees is 1,450,300 rubles.

- The amount of tax - 188 539 p.

- The number of actual earnings is February 29.

- The date on which the tax was withheld is Feb. 10.

- The last date the payment is paid to the budget is 11. 03. 2016

For March:

- Accrued to employees - 1,450,300 p.

- The tax amounted to 188 539 rubles.

- The number on which employee benefits were actually paid is March 31.

- The date on which the tax is withheld is April 8 (since April 10 coincides with the day off, the accountant transferred the income on the 8th and carried out the deduction on the same date).

- The last day of compulsory budget payment is 11.04. 2016 (the number was postponed from April 9 - Saturday to the nearest workday).

In addition, one of the employees, tax resident RF, February 8 received dividends. Their total amount is 20 thousand rubles. The date on which the tax is withheld is February 8, the last day of its transfer is February 9, 2016. The rate is 13%.

findings

The order of the Tax Inspectorate gives only a general idea of the rules for the preparation of document 6-NDFL. In practice, accountants have various questions that they have to decide on their own or to seek additional clarifications from the supervisory authority at the place of registration of the enterprise. Nevertheless, experts do not exclude that in the future, instructions for the preparation of new reports will be supplemented, or that the official structures will give comprehensive explanations on all issues.

However, it is now clear that the formation of the document is a process that requires special attention. Many accountants find it rather laborious. Nevertheless, they have to understand the situation, because for failure to provide or untimely submission of reports entails a fine.

Moreover, control authorities may block monetary transactions in the payer's account. Sanctions were also established for inaccurate data in the document. It should also be borne in mind that reporting 2-PIT has not been canceled. This means that it should also be sent to the supervisory authority. Currently, the Ministry of Justice is registering the Order of 10.30.15 No. MMV-7-11 / 485. He must be approved a new form of 2-personal income tax. It will be used by payers in the preparation of documentation for 2015.

Conclusion

According to many experts, it will be quite difficult for companies that plan to provide personal income tax reports on paper to summarize information about all employees and at the same time separately show data on rates, dates of payment of salaries, withholding and deductions of mandatory payments to the budget. In this regard, experts are now recommending the generation and submission of documentation in electronic form. Using special programs, you can make this process automated.

In this case, the participation of the accountant, as well as the number of probable errors and inaccuracies, will be minimal. Information for all employees will be reduced to documentation by the program, after which the report drawn up can be checked and sent to the tax authority through communication channels. If the company does not have the opportunity or the need to install special services, the accountant can fill out the documentation manually.

In this case, it is necessary to clearly follow the available instructions, not to make mistakes, inaccuracies. Particular attention should be paid to indicators of income, deductions, dates of payment. Keep in mind the transfer of dates from weekends and holidays to the next coming business days. This moment for some entrepreneurs can become crucial. It is worth saying that enterprises with more than 25 employees are not given a choice. They cannot submit paper reports. For them, only one order has been established - the sending of documents through communication channels.  Timely and correctly prepared and submitted reporting is the responsibility of the payer. Performing it, the business entity complies with the requirements of the law, eliminates the likelihood of bringing him to justice. In this case, deductions should be made not only on paper, but also really directed to the budget. For late payment or evasion of the duties of the payer, a person is also held liable. The regulatory authorities, in turn, are given the opportunity to carry out timely verification and summarize the information received.

Timely and correctly prepared and submitted reporting is the responsibility of the payer. Performing it, the business entity complies with the requirements of the law, eliminates the likelihood of bringing him to justice. In this case, deductions should be made not only on paper, but also really directed to the budget. For late payment or evasion of the duties of the payer, a person is also held liable. The regulatory authorities, in turn, are given the opportunity to carry out timely verification and summarize the information received.

Form 6-NDFL