If employees use the funds received from the cashier, they must submit a report. Based on this document, the accounting department of the company writes off money for operating or administrative expenses.

Essence

After three days from the moment of returning from a business trip, the employee must report on the funds received and spent. For this, compiled expense report of the reporting person, and documents confirming the expenditure of funds are attached to it: tickets for travel, hotel bills, etc. The form is approved by the head. Unused amounts are leased to the cashier on a receipt order. If the employee did not have enough funds issued, then the cost overrun is also compensated from the cash register, but on the expense order. If the employee has not provided a report on the use of funds at all, then this amount is deducted from his salary.

BOO

Reporting amounts are reflected in the balance sheet at account 71. The debit balance shows the employee debt of the organization. The turnover shows the amounts disbursed and the reimbursed overspending. The loan includes the use of funds and the return of the balance to the cashier. All amounts are recorded in the order book. Entries into it are made on the basis of FFP, RKO, advance reports. The latter are handed over to the cashier only after checking by the accountant arithmetic calculations and the intended use of funds. Consider the basic wiring.

- DT71 KT50 (51) - money was issued to the sub-report from the cash desk (current account).

- KT71 DT20 (26, 44, 71) - write-off of funds for the expenses of the main production (general business expenses, additional costs of implementation).

- KT71 DT07 (10, 15, 41) - accountable amounts were used for the acquisition of material assets.

- KT71 DT50 - refund to the cashier.

- KT71 DT94 - the amounts not returned on time are taken into account.

- DT70 KT94 - non-refunded amounts withheld from the accountable person.

Grounds

Since 2015, accountable amounts can be issued not only to employees of the organization, but also to persons with whom a civil law contract has been concluded. The operation is based on the application. This rule applies to all individuals without exception. Based on this document, the CSC is drawn up. In the application, you need to indicate the amount, date of issue, date and put your signature.

Check

The application first goes to the accountant. He checks if old settlements with accountable persons are closed. If an employee has not provided a report on previously used amounts, then new cash cannot be issued to him. Representation expenses, travel expenses, per diem - a document must be submitted for all the money spent. The results of the processing of the report show who owes whom, to whom and how much. If there is a difference between the issued and used funds, it means that the employer or employee has debt.

The provision of funds

The issuance of accountable amounts by transferring them to the employee's salary card is allowed. But for this you need to reflect in the order on management accounting the possibility of such a method of transferring funds. In the statement itself, the worker must write so that the money is transferred to his salary card, and provide the details. AT payment order the purpose of the payment should be indicated as the movement of the reported amounts. Documents for an advance report that an employee of an organization submits must include slips of all checks.

Example

Let's consider how calculations with accountable persons are displayed in NU and BU.

From the company’s cash desk on 04.25.16, an amount of funds was provided to the office manager of the conditional LLC in the amount of 2,000 rubles for a period of 4 days for the purchase of office supplies. On the same day, the accountant issued the reporting amounts on the basis of a statement signed by the head: DT71 KT50 - 2000 rubles.

04/27/16, the office manager purchased office supplies worth 1,000 rubles, filled out an advance report, submitted checks to accounting and returned the balance to the cashier. The accountant draws up such records:

DT50 KT71 - 1000 rubles. - the balance of funds has been paid to the cashier.

DT10 CT 71 - 1000 rubles. - stationery taken into account.

Reflection operation on a corporate card

To display the amounts spent on hospitality expenses related to business activities, you can use one payment instrument. The organization draws up a corporate card. Then, at the request of the employee, it issues it to a specific person, transfers the reporting amounts there.

The order of movement of payment instruments must be approved by order of the head. Sample:

LLC (name)

Director (last name, initials, signature) 03/14/16

I APPROVE: The procedure for using corporate cards

1. PIN information is confidential information. Holders of a payment instrument do not have the right to divulge it to third parties.

2. A business trip report or other document confirming the use of funds must be submitted to the director within three days from the date of making payments on the card (including withdrawal of funds) or from the day of returning to the workplace. The document must be accompanied by checks confirming the movement of money.

3. If there are no documents or the director did not confirm the report, then the amounts debited from the card are recovered from the employee’s salary.

4. The list of card holders is presented in Appendix No. 1.

5. The issuance and return of payment instruments is carried out in the accounting journal (Appendix No. 2).

6. If a card is stolen, its holder must immediately notify the bank.

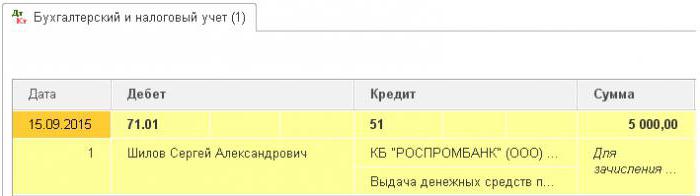

The moment of transfer of the payment instrument to the employee is not a cash issue. Entries in the BU are made at the time of withdrawal of funds. From the statement of the credit institution, you can find out the exact date of the transaction when the reporting amount was used. Account 55 is used to display transactions on a corporate card. A sub-account of the same name is opened to him. On the date of write-off of funds, a posting is formed in the control unit: DT71 KT55.

Example

On July 10, 2015, funds were paid to the corporate card of a conditional LLC, held by a marketer, to pay for online advertising. After 5 days, the marketer withdrew 3,000 rubles from the account. This transaction is confirmed by a bank statement. Accountant LLC must reflect the movement of funds by posting DT71 KT55.

Application deadlines

A trip expense report must be submitted to the accounting department within 3 days after return. Failure to comply with these deadlines will lead to additional accrual of personal income tax. The Inspectorate may consider that the reported amounts are the income of individuals. Therefore, the employee must report on each expenditure. The form can be developed independently or use a unified form. Reporting deadlines must be approved by order of the head. Sample:

LLC (name)

Order No. 15 on approval of the deadline for submitting an advance report

Belgorod March 15, 2015

Employees who receive money must submit a report on their use:

- huzhudam - no later than two weeks from the date of receipt of funds;

- travel expenses - within three days upon returning to work.

Issued funds must be used strictly for their intended purpose.

No more than 100 thousand rubles are provided for household expenses and the purchase of goods. and only by order of the director.

Responsibility for the implementation of the order, the rules for the preparation of documents rests with the chief accountant.

General Director ______________________ (full name)

Tax accounting

Until the employee has submitted a business trip report with documents confirming the movement of funds, expenses on NPP are not written off. Amounts paid do not reduce the tax base. Insurance premiums are not calculated and income tax is not withheld.

Personal income tax

The object of taxation is income, the economic benefit of the transaction, expressed in cash. The Tax Code does not explicitly say that funds issued under the report for which the employee did not report within the prescribed time are not recognized as income. According to Art. 807 of the Civil Code, such amounts cannot be attributed to an interest-free loan, since money does not become the property of the employee, and an agreement between an individual and a legal entity is not drawn up. Therefore, there is no income in the form of material benefits, which would accrue personal income tax.

But tax risks arise if the balance of the reported amounts is not returned to the organization on time or the report on the use of funds is not approved. In such situations, according to the Ministry of Finance and tax inspectors, an individual receives income in cash, which should be taken into account for personal income tax purposes. Judicial practice on this issue is controversial.

Work in "1C 8.3"

The issuance of money from the cash register is executed by an expenditure order with the same type of operation. The tabular part of the document prescribes the full name employee, amount, purpose of use of funds. Additionally, the details of which document will be printed. This is usually an employee’s passport. After the document is posted, the transaction DT71 KT50 is formed for the amount of the transaction.

If transferred to a current account, a bank statement is generated. Type of operation - “Transfer of funds to an individual”. The same fields are filled in it, but the account details are additionally indicated. This document forms the posting DT71 KT51.

All operations on the use of funds should also be included in the program. The reason for writing off money may be a plane ticket that the organization itself acquired. In this case, the document “Issue of cash documents” is formed in the “Bank and cash desk” section. It indicates the full name of the accountable person, and on the second tab the document itself, for example, reads as follows: “ticket for the Moscow-Belgorod-Moscow plane”. This operation generates a transaction from DT71 to KT50 in the amount of the cost of the ticket.

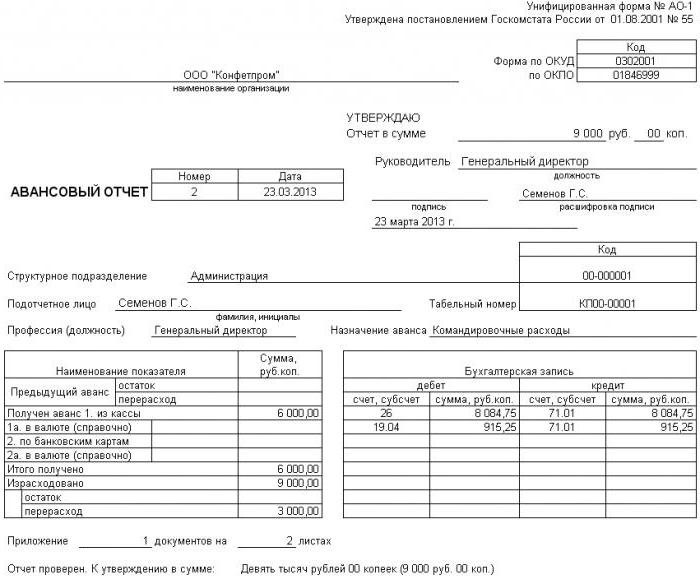

All calculations with accountable persons are documented by AO-1. Its printing form includes:

- amount transferred;

- directions of their use;

- details of supporting documents.

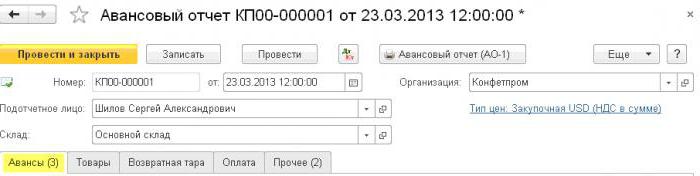

In the program, all these amounts are written off by the “Advance Report” document in the “Bank and Cashier” section. It consists of 5 tabs. The first is called Advances. It lists the documents on the basis of which funds were issued to the employee (PKO, bank statement). On the tab “Goods” indicates a list of directions for the use of funds. If necessary, "Returnable packaging" is filled. If the employee paid for the goods or services provided to the organization at the expense of the funds received, then these amounts are reflected in the “Payment” tab. After the document for these transactions is posted, the transaction DT60 KT71 will be generated. All other expenses, including daily subsistence allowance, travel expenses, and general business needs, are reflected in the Other tab. Fields filled here do not form postings, but are used in the printed form of the document.

Reporting Amount Refunds

Consider a situation where an employee received cash from the cash desk for household expenses, but did not fully use them or report back. Under the law, an employee must provide an advance report immediately upon return from a business trip or within three business days. The exact dates are indicated in the order of the head.

According to Art. 137 of the Labor Code, in order to pay off an unspent advance payment, the employer can withhold the amount from the employee’s salary for one month after the reporting deadline. This provision shall apply if the employee does not dispute the grounds and amount of deductions.Such a decision is made out in a separate order and must be confirmed in writing by the employee. The Labor Code of the Russian Federation stipulates that the maximum amount of deductions from each payment to an employee should not exceed 20% of the “net salary”.

Example

The manager of the contingent LLC received May 15, 2015 from the cash desk in the report 4 thousand rubles. to pay for the repair of household appliances in a service center. The amount of actual costs amounted to 2.5 thousand rubles.

In LLC, cash for a report for such purposes is issued for a period of 28 days. This is stipulated by a separate order of the head. Report on the use of funds is necessary within three business days. That is, the deadline for submitting data to accounting is June 14, 2015. On this day, an employee brought office equipment from repair, handed over a report, supplemented by reconciliation act completed work and cash receipt. However, the manager did not return the balance to the cash desk. On June 27, 2015, an employee signed an agreement to withhold 1.5 thousand rubles from salary.

The manager’s salary for June amounted to 24 thousand rubles. The accountant can hold the maximum: (24 - 24 x 0.13) x 0.2 = 4.176 thousand rubles. The non-refundable balance exceeds this amount. Therefore, deductions are carried out in full.

If an employee refuses to return the rest of the amount voluntarily, you will have to go to court. In this case, the costs of the enterprise will increase at least by the amount of payment of state duty. But in order for the judge not to have unnecessary questions, it is necessary to set the deadlines and the procedure for submitting documents on the use of funds by the employees of the enterprise in a separate order of the head and fix them in the accounting policy of the organization.