The book of accounting for income and expenses (KUDIR) acts as the main and only register for enterprises operating on the simplified tax system. The responsibility for its maintenance is assigned to all the indicated organizations and individual entrepreneurs, irrespective of the object of taxation chosen by them. Let us further consider how the book of income and expenses is drawn up.

General information

The book of income and expenses had previously been certified by the tax authority. This requirement has been canceled since 2014. However, this fact did not in any way affect the need for enterprises to conduct it on the simplified tax system. Individual entrepreneurs, reflecting the costs and revenues of KUDIR, are exempted from the obligation to conduct accounting. This circumstance is indicated by several letters of the Ministry of Finance.

Important points

The book of income and expenses begins to take shape from the date of transition to the simplified tax system. At the beginning of each calendar year, a new document is started. If an enterprise switched to a simplified regime in the middle of the tax period (for example, it was formed as a result of separation from another organization in the simplified tax system), then it is obliged to start conducting KUDIR from that moment. If there are several separate divisions, the accounting of income and expenses for them is carried out in one book. This document is located in the main office. Separately, for each unit, the book of income and expenses does not start.

Maintenance Form

KUDIR can be made in two forms:

- Paper.

- Electronically.

In the first case, the sheets can be printed by order of the person who approved the KUDIR. You can also purchase a ready-made sample book of income and expenses. KUDIR is stitched, sealed with a seal (if any). These events are held at the beginning of the year. Make notes using a ballpoint or fountain pen with blue or black ink. If an error is made, the incorrect text is crossed out, the correct data is indicated on the top or bottom of the line. Corrective means (putties, strokes, etc.) are not allowed. The corrected text must be certified by the head of the enterprise with the date. A seal is placed if available.

Electronic form

KUDIR sheets are printed and stitched at the end of the reporting period, when it will be filled. Information is entered into a special program. If errors are detected before printing sheets of a special order for their correction is not provided. Incorrect entries are simply corrected in the program. If inaccuracies are identified after printing, then the correction process is similar to the above. The choice of option is carried out by the enterprise itself. However, practice shows that it is more advisable to draw up an electronic version. This form is convenient both in terms of correcting errors, and in terms of the work with the document itself.

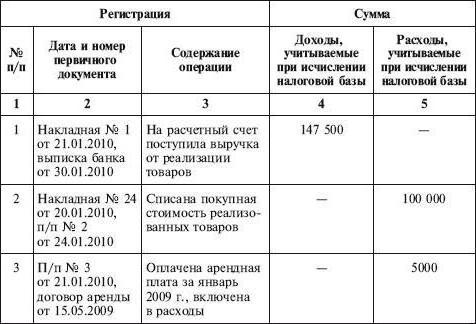

Filling in the book of income and expenses

KUDIR reflects all operations carried out in the tax period. However, one should be aware that not all revenues and expenses are included in the register, but only those provided by the simplified system and the selected taxable item. In the process transition from OSNO to STS It is necessary to take into account a number of points. In particular:

- If the company was used before transferring the company to the simplified regime, the accrual method was applied when calculating income tax, and after changing the taxation schemes, the company continued to fulfill the conditions of previously concluded agreements, and payment on them should be included in the KUDIR. If income was included in profit, then it is not reflected in the register. This provision also applies if the payment has passed after the company began to use the simplified tax system.This also applies to debt received on the OSNA, but repayable on a simplified system.

- Expenses are included in the book even if revenues are completely absent. This requirement is present in the letter of the Ministry of Finance dated May 31, 2010.

- If the entrepreneur did not conduct any activity in the tax period, he still needs to fill out the KUDIR.

- Information included in the register should be documented and justified.

- Reflection of income and expenses is carried out in chronological order as they are received by the positional method (as a separate line).

- Revenues are indicated at the time of payment (with the cash method), costs - after the payment.

As confirmation documents can be cash warrants, bank statements, payment orders, checks and so on.

Additionally

The accounting of income and expenses is carried out in Russian and in rubles. If the primary documentation contains information in foreign languages, they must be translated. Often, experts have a question regarding rounding indicators. On this occasion, the Tax Code does not contain a definite answer whether it is necessary to round off a unit of a business operation. The Ministry of Finance in one of its letters explained that all indicators in KUDIR are indicated in full rubles.