Entrepreneurs and organizations using the simplified tax system must keep track of the costs incurred and the revenues received. This allows the correct calculation of the tax base. At first glance, it seems that everything is quite simple. It is only necessary to timely fill out the book of income and expenses. However, in practice, this procedure is accompanied by a number of difficulties; accountants have questions that they find it difficult to solve. Let’s further consider how to fill out a book of accounting for income and expenses.

General information

The book of income and expenses for IP or LLC is a document drawn up in a special form. It is approved by order of the Ministry of Finance No. 135n. In accordance with it, the book of accounting of income and expenses of organizations can be maintained both on paper and in electronic form. The registration procedure in each of these cases will be different.

Important point

The book of accounting for income and expenses, drawn up in paper form, must be sealed with the seal of the tax service before filling in. Currently, there are disputes about the need to register the document, the mandatory nature of this process. Experts recommend performing this simple procedure in order to avoid disagreements with the authorized authority.

Electronic form

The book of income and expenses in the simplified tax system, drawn up in this form, should be transferred to paper at the end of the year. The document is numbered, it stamps the company and the signature of the head. After that, he must be registered with the tax authority. This procedure should be carried out no later than March 31 of the year that follows the reporting one. Individual entrepreneurs register a book no later than April 30.

Data entry specifics

The book of income and expenses under the simplified tax system is drawn up in a strictly established form. The definition and reflection of revenues and costs is strictly regulated by law. The procedure in accordance with which recognition and accounting of profit is carried out is established in paragraph 1 and paragraph 3 of Art. 346.17, p.p. 1-5, 8 tbsp. 346.18, clause 1, Article 346.25 Tax Code. Briefly, income can be described as revenue from sales and non-operating profit.

Payment by parts

In the practical activities of the enterprise, the question often arises regarding the time of accounting for a particular income. Revenues under the simplified system are recorded on a cash basis. In other words, upon receipt of money at the cash desk or to the current account, they should immediately be reflected in income. In this case, it does not matter whether the amount was received in full for the sold service, product or work performed, or an advance was credited. Prepayment is recorded in the tax period in which it was transferred. If the buyer pays for the goods or service in installments, then in KUDiR these amounts will be entered in the same amount on specific dates of receipt.

Exceptions

In the process of accounting for the income of an enterprise applying the simplified tax system, difficulties arise in determining the revenue required for tax assessment. To resolve this issue should refer to paragraph 1.1 of Art. 346.15 Tax Code. It provides a list of income excluded from the calculation of the single tax. For example, they include interest on securities participating in the turnover, dividends, etc. In addition, for enterprises that use both the simplified tax system and the UTII, they are not taken into account the proceeds from the implementation of activities that are taxed by the imputed income.

As part of the income, there is no need to take into account income that is not profit for the entrepreneur or legal entity and does not bear any economic benefit for them. Such funds may include, for example, the amounts mistakenly transferred by the counterparty or the banking organization to the account sent to the FSS of the Russian Federation to compensate for days of disability on existing sick leave, returned VAT payments sent during the period of using the general taxation regime and claimed for reimbursement, loans founders and so on.

Cost reflection

The book of income and expenses under the simplified tax system is compiled strictly in accordance with the provisions of the Tax Code. In particular, the costs are reflected in the document in accordance with paragraph 1 of Art. 346.16 of the Code. This paragraph provides a strict list of expenses to be recorded. Entrepreneurs and legal entities should focus on this particular list. The costs that reflects the book of income and expenses under the simplified tax system, must comply with a number of established requirements. In particular, they should be:

- Justified.

- Confirmed documented.

- Aimed at making a profit.

In practice, accountants often have difficulty reflecting the costs of acquiring a cooler and bottled water for employees. It is not difficult to confirm such expenses with documents. However, most likely, in the Federal Tax Service, such expenses will be recognized as unreasonable and not focused on obtaining benefits.

Special rules

Enterprises that use the simplified tax system are not considered VAT payers. That part of the cost of purchased products, which falls on this tax, should be indicated in column 5 in a separate line. This requirement is established by the letter of the Ministry of Finance No. 03-11-11 / 03. In order for the expenses that are directed to purchase bottled water for employees to become reasonable, you should take a certificate from the SES about the unsuitability of tap water for drinking. In addition, you can conclude a collective agreement. It can prescribe the provision of water to employees to ensure the necessary working conditions. In this case, the costs, referring to the TC, can be defended. However, most likely, this will only be possible in a judicial proceeding.

The same kind of problem arises for accountants, if necessary, to include in the costly part the purchase of a kettle, TV, refrigerator, and other "optional" purchases. Such expenses do not relate to the production cycle or to the direct activities of the enterprise. In this regard, the tax service does not accept them for accounting. According to paragraph 2, Article 346.17 Tax Code, the costs of a simplified system are recorded on the actual payment. As it is recognized, the termination of the obligations of the acquirer to the supplier (seller) related directly to the provision of services or goods, property rights, performance of work. In this case, you need to pay attention to the nuance. It should be noted that the costs of products subject to subsequent resale must be recorded at the time of their sale. The cost of materials is taken into account after their transfer to production. It is important to indicate the date of consumption correctly. If you make a mistake, your tax base may be underestimated.

Fixed assets

A sample of filling in the book of accounting for income and expenses provides a separate paragraph for the OS. The costs of the acquisition (manufacture, construction) of fixed assets, receipt or creation directly by the payer of intangible assets are established in the manner specified in paragraph 3, art. 346.16 Tax Code. The cost of fixed assets is not deducted at one time, but in equal shares for the reporting periods throughout the current year. In other words, if fixed assets were purchased in the first quarter, then their value is included in the expense as of 1/4 on January 31, June 30, September 30, and December 31. If the OS was received in the last quarter, then by December 31 the entire amount of the cost will be included in the costs. It must be remembered that the beginning of the write-off of the value of fixed assets as expenses is allowed only subject to a number of conditions.In particular, fixed assets must be put into operation, paid for, and ownership must be registered with authorized bodies.

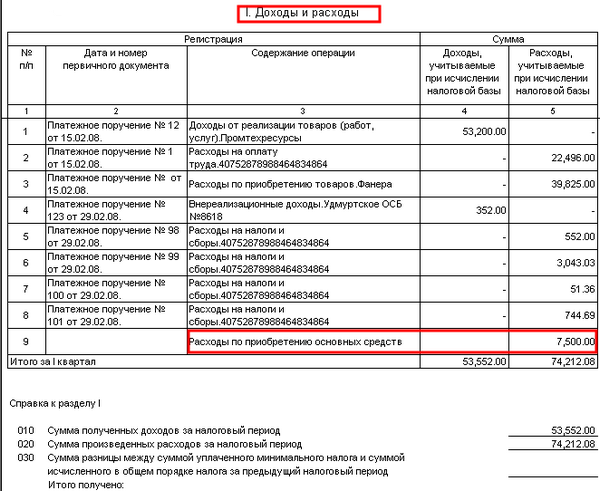

An example of filling out a book of accounting for income and expenses when paying in installments

In accordance with the contract, the company was in arrears for the materials supplied to it to the seller. The amount of debt - 100 thousand rubles - was repaid as follows:

40 000 p. - paid on December 30, 2003.

60 000 p. - listed on January 10, 2014

The seller, using the simplified tax system, made the following entries in KUDiR in section 1:

The amount of income - 60 thousand rubles - will be taken into account when calculating the tax for 2014.

Revenues of 40,000 p. included in the single tax for 2013

From the above records it is clear that column 2 does not reflect the payment order, but indicates waybill. This document confirms the revenues on line 31 and the costs on page 32.

Examples of the title page of a book: design description, photo

In the upper part, directly below the name, there is a line in which the year of maintaining the document is entered. Below are two more columns. They indicate the name of the company or full name entrepreneur. Further on the title page below there are 2 lines in the form of cells. They indicate the checkpoint of the enterprise or TIN IP. Information is entered only in those columns that are intended for a particular owner of the document. After that, fill in the lines "Unit of Measure" and "Object of Taxation". In the column below, the jur. company address or place of residence of the entrepreneur. Then there is a line in which the current account and the name of the bank where it is opened are entered. If the company serves several banking organizations, details for all of them are indicated. The latest information that must be on the cover page is the number of the notice indicating that the entrepreneur or legal entity is working on a simplified system, and the number of its issuance.

Rate

The size of tariffs for enterprises using the simplified tax system is established by 346.20 Tax Code. In 2015, they remained as they were in 2014. The rate for STS income is 6%, with the simplified system "profit minus costs" - 15%. By decision of the regional authorities, the latter indicator can be reduced to 5%.