The changes made to the property tax in 2014 became one of the most popular topics of discussion among accountants, managers, auditors, and ordinary citizens. This is due to the scale of the changes. He is really impressive. Innovations affected and objects of taxation and the tax rate and tax calculation principle. About how not to get confused by applying all these new property taxes, and not only not to incur losses, but in some cases to save, we will discuss this article.

Changes affecting legal entities and individual entrepreneurs

Since 2015, enterprises using special taxation regimes lost the ability to not pay property tax. Now all organizations are required to pay it, namely:

- located on the main taxation system;

- applying a simplified taxation system;

- organizations on a single tax on imputed income;

- individuals (individual entrepreneurs).

The only business entities exempted from the obligation to pay property tax of 2014 at all are individual entrepreneurs taxed single agricultural tax.

The difference between different tax systems

The difference lies in the calculation of the tax base for which the property tax of 2015 is calculated. So, legal entities applying the basic taxation system calculate the tax according to the general rules, and enterprises paying a single tax on imputed income and applying a simplified taxation system, - according to the cadastral value of the property.

For information

Under the general rules are understood adopted since 1969 and annually indexed inventory value of fixed assets. It is small enough, because the tax based on it was not a real oppression for enterprises. Cadastral value is closer to market value. It is calculated on the basis of mathematical models and evaluates the general characteristics of an object; I do not focus on its particular features. This cost is much higher than the inventory, therefore, a tax calculated from such a tax base can be an impressive item of expenses for the enterprise.

Property tax at IP

Individual entrepreneurs on the basic taxation system calculate new real estate taxes according to the general rules, and applying special taxation regimes - depending on what form of value is determined for each property. If the inventory value is determined, the tax is not paid, and if the cadastral value is determined, then it is paid. That is, such a situation is possible when an entrepreneur pays real estate tax for some properties in 2015, but not for others.

How to find out for which real estate what value is determined?

It is necessary to check the list of real estate objects with a certain cadastral value, approved by the law of the subject of the Russian Federation where the real estate is located. This document will be issued by the regional authorities a year in advance, which means that in 2015 it will not be necessary to verify it when paying, since this rule was not introduced a year ago.But starting from 2016, when calculating advance payments, it will be necessary to check the list and determine which of the fixed assets owned by the organization should be calculated at the cadastral value.

For information

You must also consider the following nuance. Premises located in buildings to which property tax is applied in 2014 are also taxed at the cadastral value, even if they are not listed as separate units. This applies, for example, to offices in business centers or shopping places in shopping centers. In this situation, the cadastral value will need to be determined by the organization’s accountant himself on the basis of the share of the premises in the total area of the building, this norm is spelled out in article 378.2 of the Tax Code.

What other ways to find out the cadastral value

There is also an alternative option for an accountant if he is afraid to make a mistake with this calculation. You can send an official request for each room owned by the company to the regional office of the Federal Property Management Agency. Employees of this department are required to inform the cost upon request.

Real estate tax less than a month in tenure

If the company owns the premises for an incomplete month, the property tax on the cadastral value of the property is calculated with a coefficient. All these nuances have significantly complicated the work of an accountant, especially in enterprises using special tax regimes.

Is it possible to reduce property tax for 2014?

In connection with the growth of the tax burden imposed on enterprises, the logical question seems to be how it is possible and possible, in principle, without violating the law, to reduce real estate tax 2015. Answer: "Yes, it is possible." The law provides for the application of special tax deductions for a certain size of the area of a taxable property. True, the decision is whether to introduce such deductions, in what amount and on what conditions? given to regional authorities. And, therefore, organizations located in different constituent entities of the Russian Federation are placed in different conditions: someone is more lucky, someone less.

Analysis of regional legislation in the field of taxation of real estate by cadastral value

Tax deductions for 2015 are provided only in 8 constituent entities of the Russian Federation.

- In the Trans-Baikal Territory, a deduction is granted for 150 square meters. m of space per taxpayer for one property, without additional conditions.

- In the Kemerovo region exempted from real estate tax 100 square meters. m of space per taxpayer for one object, also without additional conditions.

- In the city of Moscow are not taxed 300 square meters. m of area for one object, provided that the company is a small enterprise, has been operating for more than three years, has more than 10 employees and has revenue in excess of 2 million rubles per year per employee.

- In Primorsky Krai, 20% of the cadastral value of any object is exempted from taxation.

- In the Republic of Buryatia, 300 square meters are not taxed on real estate. m of space for one object and 100 sq. m for one room without additional conditions.

- In the Republic of Khakassia, 300 square meters of the facility’s area are not taxed, provided that the organization uses UTII, has been operating for at least two years, last year it had more than five employees and paid employees wages not lower than the industry average in the region.

- In the Tula region are exempt from tax 100 square meters. m of the facility’s area, provided that the organization uses UTII, has been operating for at least three years, the previous year had more than three employees, paid employees wages in excess of the regional minimum wage and not lower than the average wage in the industry.

- In the Tyumen region is not subject to 150 square meters. m of space for one property without additional conditions.

What other differences in taxation of real estate in different regions

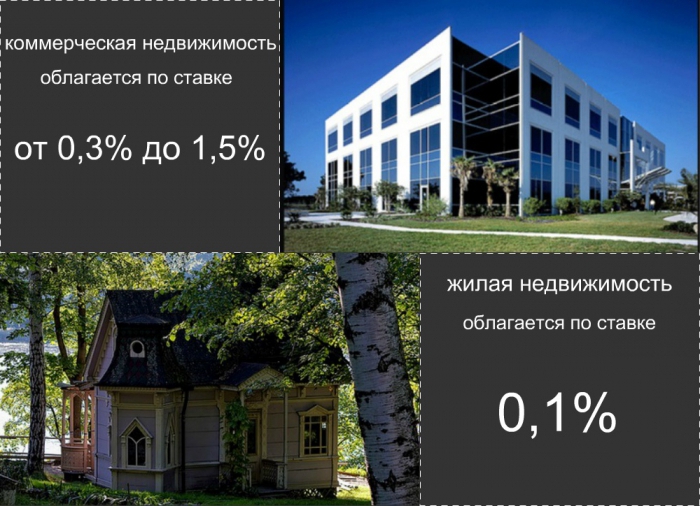

Also, in different constituent entities of the Russian Federation, the rates determining the real estate tax also differ. A record low rate was approved in Primorsky Krai: it is 0.3%. Rates in the amount of 0.5% and 0.7% are set in the Ivanovo, Magadan, Tomsk regions and in the republics of Altai and Buryatia. One percent of the cadastral value will be paid by entrepreneurs of the Trans-Baikal Territory, Sverdlovsk Region and the city of St. Petersburg. The rate of 1.2% is approved in the city of Moscow, the Republic of Tatarstan and Udmurtia. And, finally, organizations of other constituent entities of the Russian Federation will be forced to pay the highest rate of 1.5%.

Individual real estate tax has also changed

Since 2015, all individuals are required to notify the tax inspectorate of the real estate they own and acquire. In connection with this new rule of law, many have logical questions. What specific property should be reported? In what terms and in what form should this be done? And what measures of responsibility are assumed in case of non-compliance with these standards? Let us consider in more detail the answers to all these questions.

- You should report on all real estate owned by you, land and vehicles that are not yet listed in the inspection database. The presence in the database of real estate is indicated by previously sent notifications with the amounts of property tax due. Typically, tax authorities send them out before October 1 of the year following the reporting year. If such notifications came to all of your property, you do not need to inform anything further. And if not, you must fill out on special forms messages about the availability of real estate by individuals and send them to the address of the inspection.

- The form of communication is approved by law by order of the Federal Tax Service of Russia of November 26, 2014 No. MMV-7-11 / 598 and is called KND form 1153006. This form is sent to the tax authorities until December 31 of the year following the year in which the property was acquired. Or until December 31, 2015 for all ever acquired objects. You can submit a message either in person or send by mail. Be sure to attach copies of title documents to these real estate properties. You can also report via the Internet in your account on the official portal of the state. services.

- For failure to submit a message, a penalty of 20% of unpaid tax is provided. He will be charged from 2017 for the three years preceding him with the payment of penalties and the tax itself. In case of voluntary reporting of real estate objects, real estate tax on individuals will be accrued only for the last year of ownership, regardless of how much the object was actually in your ownership. The tax office will be involved in the tax calculation.

The real estate tax of individuals is planned to be introduced on a large scale since 2020. Its rate will be significantly lower than the rate for legal entities and, most likely, will not exceed 0.1% of the cadastral value of the property. In addition, tax deductions in the form of a tax-free area of a residential apartment or house will most likely be present. There will also be a significant portion of beneficiaries who are completely exempted from the obligation to pay property tax. Most likely, these will be socially unprotected groups of the population, such as veterans, disabled people, orphans.