Direct indemnification (PVU for short) in our country was introduced several years ago, along with another innovation - Europrotocol. The change seemed to be aimed at simplifying the receipt of insurance for compulsory motor third-party liability insurance. Let's study what its essence is, look at the application form filled out in these cases, and analyze whether it has become easier for drivers and the UK.

Legal basis

There is no law on PES. The norm is regulated by another law - “On CTP”, namely, article 14.1.

There are also "CTP Rules" and "Agreement on Direct Compensation of Losses under CTP", which describes the actions of the insured and the insurer.

The insurer carries out PES on the basis of liability insurance for both participants in an accident. Having recovered the loss, he turns to the insurer of the guilty party. The latter is obliged, in turn, to reimburse the loss to the insurer who paid the PAY. Payments are made on the basis of a document concluded between PCA members: “Agreement on direct compensation for losses”.

It seems that all the circumstances that can happen in an accident are clearly stated. However, in practice, questions still arise.

What does PVU mean?

By PVU, one understands the appeal of the injured party directly to their insurance company, and not to the company responsible for the accident, as it was before, to receive payment. Such a rule, like Europrotocol, was borrowed from the laws of Western countries. However, unlike them, in Russia, although they adopted a direct compensation for losses, they made their own changes. So, in Western countries, for all accidents, victims turn to their insurance company. At first, however, it was allowed to contact either the person responsible for the accident or one in the UK.

Since August 2014, however, the changes entered into force. According to them, the so-called non-alternative direct compensation for damages was introduced. Now, if there are clear signs of an accident, the PES should be reimbursed only at its insurance company.

When submitting an application for PES

The victim does not apply to his IC in all cases, but only when the accident meets certain criteria:

- Both drivers have not only a valid OSAGO insurance policy, but also have civil liability insurance.

- Damage is caused only to property. People did not suffer from an accident.

- One of its participants is guilty of an accident.

- The culprit insurance company has a valid business license.

Indemnification and Europrotocol

Sometimes, due to the presence of some similarities, the PVU is confused with the Europrotocol. However, these two concepts are completely different. Europrotocol - a document that is drawn up by one of the participants in the accident (front side) and signed by both drivers. Traffic police are not called upon. The document is submitted to the UK.

The direct compensation for losses under compulsory motor third-party liability insurance is not a document, but a rule of law, according to which the injured party sends an application for damages to its own insurance company. Moreover, filling out the Euro protocol is possible only if the amount of damage by mutual consent of the parties does not exceed 50,000 rubles. In other situations, the traffic police inspector must be called.

At the same time, in one and the other case of an accident there are similar features: the incidents are minor, had no consequences in the form of harm to human health and did not lead to death.

At the same time, the policyholder may refuse to indemnify in some cases. Consider when this happens.

Refund Denied

Even if the accident will have all the signs by which the insured must compensate the victim, he has the right to refuse this in the following cases:

- If the victim has already filed an application with the UK, the culprit of the accident.

- The participants in the accident drew up the Euro protocol and did not call the traffic police officer, despite the fact that they have different opinions about what happened.

- There are legal disputes due to traffic violations.

- The insurer was not notified in time about the occurrence of the insured event.

- During a traffic accident, the Central Bank, antiques, intellectual property, and objects of religious value were damaged.

- The policyholder wishes to recover non-pecuniary damage or lost profits.

How to get insurance benefits and what you can’t do

So, so that there are no problems with the payment, you should follow a certain procedure for damages. To do this, you must submit an application to the insurance company within the time limits established by law. Necessary documents are also collected. From his insurance company, the insured receives a referral for an examination and a list of companies where he can implement it. At this time, the insurer asks the SC of the guilty party of the accident for consent to payment. If a positive decision is made to the account indicated in the application, the victim receives money for repairs.

Further, insurers deal with the case without the participation of the insured.

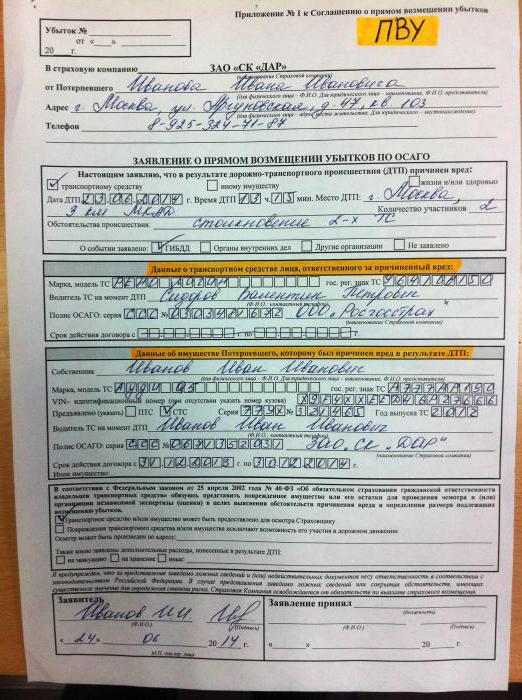

The application form, which must be completed, can be considered in the following photo.

Tip: in no case do not repair your car until the money arrives in the account. If you suddenly refuse, you can appeal the decision. If the amount is too small and does not cover all costs, various steps can also be taken to achieve full damages. However, if you hurry and repair the car earlier, then nothing can be done.

Features

There are rules in the PIA agreement that specify fixed amounts for various types of traffic accidents. Based on these amounts, the IC of the guilty person will reimburse your IC for a certain amount, which differs from the one that you receive.

Because of this rule, insurers can easily pay small amounts. Then both the insured and the insurer will be satisfied (with the exception of the IC of the guilty party). However, if the damage exceeds a fixed amount, your UK will seek out tricks so that you go directly to the UK responsible for the accident.

It is clear that insurance companies are trying to find opportunities to pay less. However, as a result of these manipulations, insurers suffer, that is, victims of a traffic accident who are clients of the UK. They are forced to spend their nerves and time to achieve a payment that will cover the cost of repairing a car.

How to deal with manipulation of SK

We will figure out what can be done if insurers refuse to pay, and how not to bring the situation to this.

All documents must be completed very carefully. Any incorrect information will result in delays awaiting you at best, and failure at worst. Corrections when filling out, for example, accident reports, are also unacceptable.

The right to PVU is obtained not only by the owner of the policy, but also by the injured party. In this case, the names included in the policy do not matter, and for whom the technical passport for the car is issued. The application for direct compensation for losses is submitted by the driver who was driving when the accident occurred. Of course, we are talking about those cases in which he had the right to be a driver in compulsory motor third-party liability insurance: that is, he was included in the policy or mandatory motor liability insurance implies the use of a car without restrictions.

Where to go?

If all the signs of an accident fall within the scope of a non-alternative PED settlement, however, both insurance companies have their licenses revoked or bankruptcy proceeding, the injured party must file a claim with the RSA. In this case, we will talk about compensation payments.

In addition, there are other situations when contacting the SAR, even if the conditions for obtaining the PES are not met.

For example, the Union of Auto Insurers will pay compensation if more than two cars were damaged as a result of the accident, but the license was revoked from the Insurance Company or it is in a state of bankruptcy.

The same applies when people are injured due to an accident.

PCA will pay compensation to the injured person when the perpetrator remains unknown, in the event that people are injured.

A cash payment awaits the victim if the culprit is not insured under compulsory motor third-party liability insurance (also only when people are injured).

Conclusion

If there is a nuisance and you get into an accident, it is best to immediately notify your insurance company via a hotline. If the accident meets all of the above conditions, all your actions were correct and a civil liability contract was concluded, compensation for losses according to the described system should be made.

Well, when the driver does not know how to behave in such situations, and makes mistakes, then the likelihood of receiving money to cover repair costs is extremely small.