It is time to clarify a rather new concept that has appeared in updated financial dictionaries - securitization. For ordinary people, this word is associated with security and safety services. And, in fact, this concept is connected precisely with protection, security, insurance, protection of financial transactions and not only with this.

What is securitization?

The securitization process may include an extensive range of special transactions, creating a complex of complex legal actions. In general, the definition can be formulated as follows: securitization is the process of creating securities (securities) secured by loans, with the help of which assets pooled into a pool are accepted as standard securities secured by the same pool. For the broadest perception, this is the process of increasing the importance of the Central Bank in the market with the aim of borrowing and lowering risks by redistributing financial instruments. The largest market for securitized assets is the mortgage securities, because it is the most predictable segment of the benchmark assets.

In a broad sense, securitization is the process of attracting borrowed funds by issuing securities.

If we consider this process in a narrow sense, the definition will be formulated as follows: securitization is a way of refinancing illiquid assets (accounts receivable and future profitability) by issuing securities. Simply put, in the amount of existing receivables or planned income, securities are issued, the security of which is this same receivable or planned yield.

Such transactions are made by financial institutions in order to reduce debt servicing costs.

Types of structural transactions and their risks

Structural transactions in the world practice are classified in too extensive ways, however, there are a number of the most typical types of transactions.

According to the type of assets, structural transactions can be divided into:

• securitization of future receipts (transfers, receipts from trade and export operations);

• securitization of existing assets;

• secured by the Central Bank with the help of commodity and automobile loans, leasing, credit cards;

• mortgage securities in the housing program;

• mortgage securities for commercial real estate;

• securitization of a pool of debt obligations;

• corporate securitization.

By the separation of pools from the originator, structural transactions are divided into:

• securitization through direct sales;

• securitization through the weakening or creation of assets.

According to the location of the issuer:

• internal structural transactions (issuer and originator are in the same country);

• cross-border structural transactions in which the issuer and originator may be located in different countries.

Any financial transactions involve a number of risks. This also applies to structural transactions. The main categories of structural risks.

1. The risk of confusion is the probability of confusion of the issuer's cash injections with the funds of the originator. The problem can be solved by introducing a service organization (service provider) that provides a current account for the execution of the transaction. The servicer monitors the movement of funds and is able to prevent the issuer from defaulting when it occurs with the originator.

2. Interest or currency risk arises in the event of a gap in the currency or interest of the issuer's payables or receivables.In this case, the profit from bonds depends on fluctuations in the exchange rate of currencies or a jump in interest rates. Such risks are hedged by means of swap mechanisms, however, in Russia such risks did not arise, since the issuer is rating foreign banks.

3. Country risks are taken into account when forecasting stress scenarios. It should take into account and analyze the scale of the economic recession:

• the state of the country's interbank system;

• level of volatility and exchange rates;

• provision by the state of a debt obligation in the event of mass defaults.

4. Legal risks in securitization are the legal purity of using the issuer's assets and the safety of its pool from the risk of default of the originator.

Securitization of financial assets

Consider the mechanism of asset securitization as an example of a mobile operator. For effective development and protection against competition, our operator needs to build several new base stations to cover the communication of a new region. At the moment, the telecom operator does not have the required amount of financial assets. He also cannot issue bonds or get a loan, because the obligations on the previous loan have not yet been fulfilled. A securitization deal may come in handy.

As security for the transaction, the operator takes into account future profits:

• income from existing subscribers using network services;

• income from subscribers who have concluded an agreement but do not use services;

• income from future subscribers who want to use the communication services of this operator.

The originating operator isolates cash flows, creating a pool of future financial claims. The originator then cedes these financial requirements to the service company. The servicer throws the securities secured by the originator's financial pool to the market and attracts investors (issuers). The proceeds from the sale of securities go to the account of the originator. It is advisable to insure these funds.

After receiving the benefits, the originator returns the funds received to the service provider. During the securitization transaction for future requirements, the operator managed to develop its business and get ahead of competitors. Issuers received a return on invested financial resources; the state economy benefited from a tax increase.

Why securitization is needed

Securitization is beneficial for the originator in such aspects:

• in attracting additional financing in the form of a purchase price;

• to limit the risk of loans for assets;

• to increase the balance;

• in gaining access to additional sources of financing;

• in lowering the cost of financing;

• in balancing assets and liabilities;

• in increasing competitiveness;

• in improving the performance of the initiator.

Benefit for investors from securitization:

• investing in assets secured by commodity or future profitability;

• Securities secured by future assets are less volatile;

• Asset-backed securities are more profitable than bonds;

• Asset-backed securities are not exposed to eventual risk.

“Narrow” and “wide” sense of securitization

Securitization can be divided into two large groups, depending on the type of financial flow generated. So, asset securitization is divided into:

• securitization of claims;

• securitization of future requirements.

In the first case, the requirements of the originator to customers already take place and are drawn up by the relevant financial documents. The amount of financial claims can be calculated, since the total amount of debt is determined.

In the second case, everything is a little more complicated. Future financial requirements can be calculated both from future contracts, and from already concluded. In such transactions, it is difficult to calculate the financial flows from the clients of the originator.

It follows that securitization is a very flexible process, in which it is very important to structure the securitization scheme for the real needs of its initiators.

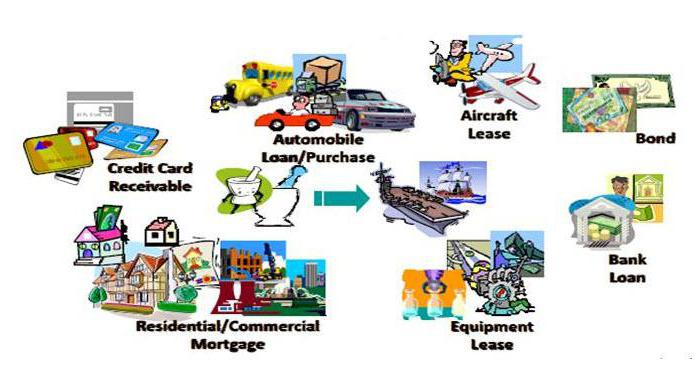

Securitization market

The most common securitization products are loans:

• non-standardized;

• automobile;

• commodity consumer;

• credit cards;

• annuity;

• mortgage.

In recent years, securitization of mortgage loans has been steadily increasing. These financial transactions are for refinancing purposes. They contribute to the typification of the market, since issuers buy only those loan products that satisfy the requirements of underwriting.

How to attract originators

Consider motivating factors for attracting originators, which have an undeniable advantage over unsecured bonds.

1. Reducing the cost of resources - securitization of loans is carried out by banks in order to reduce the resource base.

2. Diversification of the issuer is a great opportunity to gain access to global financing.

3. Credit risk reduction - the securitization process is able to completely protect the originator from credit risk by transferring it to other participants in the process.

4. Increasing liabilities and assets through consistent payment flows.

Analysis of the main risk categories

1. Collateral risks consist of the probability of default and the probability of payment of default loans.

2. Mortgage securitization requires an assessment of the probability of default on the assets of the pool of the originator.

3. The devaluation of the ruble may cause the likelihood of default, which increases the risks of payments to securitized assets.

4. Default loans entail a decrease in the probability of asset recovery.

Leverage

Any financial relations require constant improvement of legal relations in the legislation of the country. The fundamental reasons leading to the inhibition of the development of securitization in Russia:

• untypicality - distrust of the new economic lever of regulation;

• untimely legislative settlement of transactions.

In European countries, the securitization process has become part of the financial world market. However, Russian legislation is in no hurry to introduce a law on securitization. As soon as this process gets legislative settlement, we can talk about achieving the greatest effect of the development of securitization.