In practice, there are often situations such that a transaction completed at the cost of considerable effort subsequently creates serious problems for the company. For example, the deadline for fulfillment of obligations, and the company is not able to comply with the conditions. The current legislation provides for several options for terminating legal relations in such cases. As a rule, they come down to debt restructuring. As one of the acceptable ways to terminate relations between entities is the conclusion of an agreement on compensation. Using this option, the parties exit the transaction with the least loss. This, in turn, allows you to keep the partnership in the future. Let us consider in more detail the agreement on compensation.

Characteristic

The lease agreement is reflected in the accounting documentation. To correctly show the operation, it is necessary to clearly understand its significance. If the deadline for fulfillment of the obligation has come, and the company for any reason cannot repay the debt to the creditor company, the transaction may be terminated by mutual consent of the parties. The parties to the relationship themselves establish the procedure and conditions for this operation. In simple words: compensation for the debtor is a fee for refusing to repay the debt. For the lender, this is compensation for non-compliance by the other party with the terms of the transaction. In practice, the compensation agreement is signed after one of the participants was unable to pay the debt on time.

Compensation Methods

There are various conditions on the basis of which an agreement on compensation is signed:

- By transferring property.

- Cash payment.

- The provision of services.

- Production work.

The ability to use these options is confirmed in an information letter from the BAC Presidium. For example, the purchaser of the goods cannot make a cash payment, as agreed in the contract. To pay for products, he provides any services to the seller.

Important point

Business entities should clearly distinguish between an agreement on compensation and novation. In the first case, there is a full repayment of debt. Under the novation agreement, new obligations arise. For example, an entity, instead of paying off a debt, transfers its own bill of exchange to the creditor. Such an operation cannot be considered compensation. This is due to the fact that the bill itself acts as an obligation. Thus, instead of one debt, another arises. If the bill is bank, and not its own, then its provision to the creditor will act as a performance of obligations. Accordingly, this paper allows you to pay off debt without any consequences. In this case, the indentation takes place.

Documenting

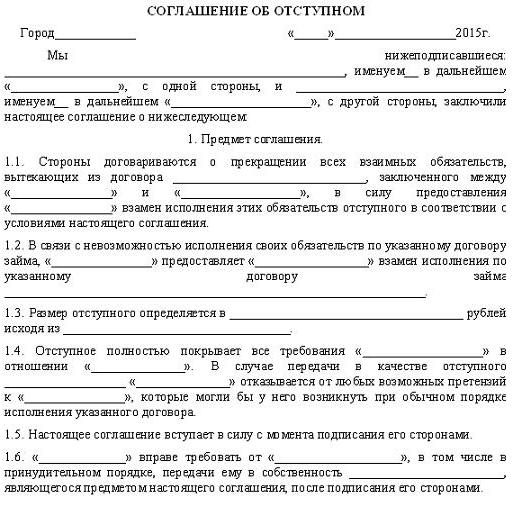

There are no specific requirements in the current legislation that the compensation agreement must comply with. A sample document is filled in this regard in accordance with the provisions of the Civil Code, which apply to the written execution of transactions. It should be noted that the signing of the document is carried out exclusively at the initiative of both participants. The lease agreement cannot terminate or modify the original contract.

Basic information

The lease agreement must contain:

- Type of compensation.

- Time of delivery. They may coincide or exceed the period allotted for the performance of obligations.

- The order of provision.

- Debt that is offset.

It is believed that the compensation fully covers the original debt. However, partial refund is permitted. This circumstance should also be documented. For example, an agreement on compensation under a loan agreement is signed. The parties decide that compensation may cover only a certain part of the debt or compensate for the forfeit. In this case, the obligation will be deemed to have been terminated in proportion to the reimbursement provided on the fact.

Nuance

Upon granting compensation, not only the main debt is repaid, but also the penalty. This is the case, unless otherwise agreed by the parties. Legislation does not prohibit the inclusion of a penalty in a document. However, if the agreement does not say anything about it, then the debt will be considered fully repaid. This position is confirmed by judicial practice.

Act of transfer

Accounts payable will be deemed repaid only after the actual provision of compensation. This means that for termination of obligation it is not enough to sign the corresponding document. It is necessary to really provide compensation to the lender. This fact must be documented. When providing compensation, an act of transfer is drawn up.

Additionally

By signing an agreement on compensation, entities stipulate that the interested party does not require repayment of the initial debt. The document must provide for the liability of participants in the transaction. In case of non-compliance with the terms of the agreement, the creditor has the right to demand repayment of the initial debt and apply sanctions to it established by law.

Reflection of the operation of the debtor

When maintaining accounting for transactions with compensation, it is necessary to take into account the provisions of paragraph 6.4 of PBU 9/99 and paragraph 6.4 of PBU 10/99. Costs associated with the receipt of work, products or services by the enterprise shall be reflected in the accounting documentation in an amount equal to the amount of payment or payables. Here it is necessary to take into account one caveat. If an entity enters into a lease agreement, the original payable should be adjusted for the value of the asset being disposed of. At the same time, its size is established by the principle of analogy. That is, the value of the asset to be disposed of is formed in accordance with the price at which, in similar circumstances, the company determines the cost of such funds. The income of the enterprise is an increase in economic benefits upon receipt of money, other material assets or repayment of debt, which leads to an increase in capital. It follows that the transfer of property in accordance with the compensation agreement will constitute profit. In paragraph 5 of PBU 9/99, it is established that revenue from the sale of goods, the provision of services, and the performance of work is recognized as income from ordinary types of activities.

Accounting with the creditor

Revenues are recorded in an amount equal to the amount of the receipt of money or other material assets or the amount of receivables. It is determined in accordance with the price established in the contract between the buyer / user of the assets and the company. When conditions change, the initial amount of receipts or receivables should be adjusted. The basis is the value of the asset to be received by the company. Thus, the creditor, when receiving services, products, works on account of payment for goods previously shipped, must adjust its revenue.

Tax payments

The field of how the acquired property will be accepted for accounting, if there is an invoice from the supplier, the company may accept a deduction of "input VAT". When providing a refund, value added tax is determined in a general manner.The calculation is carried out in accordance with the price, which is indicated by the parties in the compensation agreement. The amount of tax on services, products, works purchased as reimbursement, allocated in the debtor's invoice, is deductible by the taxpayer if they are supposed to be used for operations subject to VAT.

To calculate the deduction from profit in income, it is necessary to take into account the proceeds from the sale of products, services and works that were transferred as compensation, at the cost specified in the agreement. VAT is not included in the amount. If the original debt is repaid in full, income is determined in the amount of the primary obligation. In this case, expenses are taken into account according to general rules, depending on the nature of the object provided as compensation. The lender's property received in the form of compensation, work, services or rights are reflected in accounting documents at the value specified in the agreement concluded between the parties on the date of its transfer. If the initial debt is repaid in full, the cost of acquiring compensation is determined as its amount excluding VAT.

Conclusion

As can be seen in the taxation and accounting of operations that are associated with the repayment of debt by providing compensation, there are no particular difficulties. In practice, such transactions are quite common. Most companies cooperating with each other do not see any obstacles to concluding a compensation agreement when such a need arises. In this case, it is important to stipulate all conditions for the provision of compensation, to establish a specific period and procedure for compensation. It is also important to determine the liability of the debtor for non-compliance with the conditions. In the economic activities of entities there are various circumstances that may impede the timely repayment of debt. For such cases, the law provides for various norms that allow a peaceful resolution of the situation. Retirement provides an opportunity not only to pay off the debt with the least losses, but also to keep business partners.