If errors are identified in the reporting provided to the regulatory authorities, the filing of an updated declaration is necessary. In the Tax Code there is Art. 81, regulating the procedure for its provision. Let us further consider how the filling out of the clarifying declaration is carried out.

General issues

In some cases, after reporting to the Federal Tax Service, the payer discovers that the documentation does not reflect certain information or there are errors in connection with which the taxable base changes. Accordingly, this will affect the amount of obligatory payment. In accordance with Article 81 of the Tax Code, the entity must submit an updated declaration. First of all, the payer must establish whether reporting errors result in an underestimation of the amount of payment. In accordance with this, he will have the right or obligation to make adjustments to the document.

General rules

In accordance with Articles 81 and 54 of the Tax Code, if errors are detected in the current period when calculating the base relating to the previous time periods, the recalculation of obligations is carried out in the period of inaccuracy detection. Thus, the payer provides an updated tax return for the period in which the distortion was made. In addition to it, in some cases, the inspection requires a certificate of calculation. It reflects the reasons for making adjustments to the statements submitted earlier. In practice, certain difficulties often arise in the preparation of a document. When filling out the declaration, a number of specific points should be taken into account.

Nuances

The revised declaration should contain correctly calculated payment amounts, and not the difference between its correct value and the transfer already made. The results of inspections carried out by the inspection for the period in which errors are identified, there is no need to take into account the amended reporting. The deadline for submitting a corrective document to the Tax Code is not defined. In this regard, an updated declaration can be sent at any time after the detection of an error. The defect will be recognized as corrected only if the entity provides an updated declaration. If the control body begins or sends a notice of the appointment of the audit, then there is no sense in compiling a corrective document.

Example

The organization in the 2nd quarter of 2007 found a distortion in the 1st quarter. Accordingly, the accounting and tax returns were submitted with errors. The company must provide a corrective document. Thus, it is necessary to clarify the declaration of profit and other deductions for the 1st quarter. In accounting, error correction is carried out according to the rules of paragraph 11 of the Guidelines on the procedure for processing and reporting. They were approved by order of the Ministry of Finance No. 67n dated July 22, 2003. According to the Guidelines, if errors are detected within the reporting year, any corrections to the previously submitted statements are not necessary. Adjustments are taken into account in the month in which the distortion was detected. It should be borne in mind that if the tax amount decreases during the clarification, the control body may re-examine the period in respect of which changes are introduced. However, this is allowed if it is within the three years preceding the year in which the distortion is detected.

The specifics of the deadline

As indicated above, the Tax Code does not establish a clear period in which an updated declaration of income tax or other payments is provided.It follows that upon presentation of a corrective document in the current year for those periods for which the statute of limitations has expired, the control authority cannot refuse to accept it. However, an on-site inspection may cover only 3 previous years before the one in which the relevant decision was made. It follows from this that if the enterprise has detected an error in the period for which the inspection does not apply, there is no sense in correcting it. First of all, this is due to the fact that the Federal Tax Service will not be able to check this time period, even if there is an arrears in the payer. In addition, the subject will not be able to return or credit the overpayment if the amount of deductions decreases during correction. Revision of the payer's obligations, therefore, beyond the three-year period is not possible.

Controversial situation

According to Art. 78 of the Code, an excessively paid amount should be set off against future payments of this or other taxes, arrears of other deductions or returned. The corresponding application can be sent within three years from the date of payment. In such a situation, a problem may arise. The payer provides an updated declaration with a reduced amount of deductions and a statement of offset. On the date of sending the documents, the period in which the supervisory authority is entitled to verify the reporting has expired. Accordingly, the inspection has no reason to carry out full-fledged activities regarding documentation.

In this case, the FTS recommends that the territorial unit accept a corrective declaration. An application for a set-off or a refund shall be considered taking into account the supporting papers provided by the payer with the subsequent issuance of an appropriate decision. Thus, the burden of proof lies with the subject. If an updated VAT return is submitted and the amount of the deduction is reduced in it, the corresponding application for offset / refund will not be satisfied. For this payment, a different moment has been established from which the calculation of the statute of limitations begins. It is the calendar date of the end of the relevant period. If an updated VAT declaration is submitted after 3 years from the date of completion of the time period in which a positive difference is revealed, it will not be refunded.

Sample revised declaration

Registration is carried out on the same form that was used to make the initial information. The updated declaration on the simplified tax system or other taxation system includes the same sheets that were present in the original statements, with the replacement of incorrect information with correct information, as well as the addition of data not specified earlier. Sections 8-12 contain a special field. It is filled out only upon clarification of the declaration - 001 “Relevance of previously provided data”. Sections 8-9 are executed by the payer, 10-11 - by agents. In Sec. 12, information is entered by persons who do not pay VAT, but who have submitted invoices to customers. Column 001 can have one of the following values:

- 0 - if necessary, correct the reflected data in this section. In other fields with the sign 0 enter the correct information.

- 1 - if you do not need to make changes, since the previously provided data is correct. Other fields are marked with dashes.

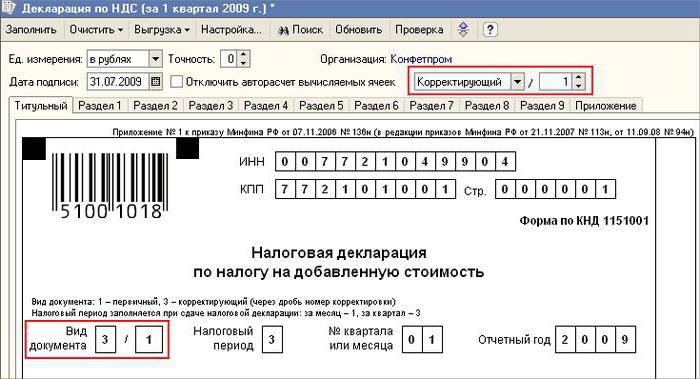

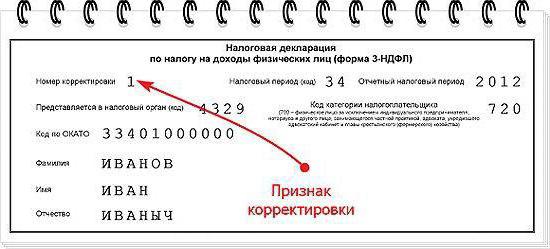

The cover page also has a required field - the correction number. A number is entered in it, which corresponds to the serial number of the indication of changes in the statements. In the case of the initial filing of the declaration, 001 is set. With each subsequent adjustment, the number changes in increasing order - 002, 003, and so on.

Succession Features

Some difficulties arise when providing a corrective document in respect of an enterprise that has ceased to exist, but its duties and rights have been transferred to another company. This situation is characteristic of the reorganization carried out in the form of accession.Here should refer to Art. 50 Tax Code. In paragraph 5 it is said that in case of joining one legal entity to another, the affiliated enterprise acts as the assignee regarding the obligation to deduct mandatory payments. If the successor identified in the reports provided by the company before the reorganization, distortions that led to an underestimation of the amount payable, then he must draw up a correction document and present it on his behalf. The updated declaration is sent to the place of registration of the affiliated organization.

Important point

Do not forget that the certainty with the place of provision of the corrective document does not exempt the successor from setting the budget, which should receive the amount. If this is the federal level, then there will be no difficulty. Problems may arise if the tax should be credited to the regional budget. Suppose, during a reorganization in the form of an accession, a legal entity located on the territory of one of the subjects of the country ceases to exist. During his work, errors were revealed in the previously submitted reports. The successor is in another region. He submits a corrective document to the address of his account, and repays the amount of the arrears to the budget of the entity to which it was to be deducted by the affiliate.

Additionally

In the event that false information and distortions are found in the statements that do not lead to a reduction in the tax amount, the provision of a corrective document is the right and not the obligation of the payer. In the previous edition of Art. 81 NK there was no such wording. As a result, the right of the subject was not always correlated with the obligation of the inspection to accept the amended reporting. At present, the illegality of the FTS refusal is becoming apparent. The control structure is obliged to accept the updated declaration and register it no later than the day (working day) that follows the calendar number of documents.

Disclaimer

The revised declaration can be used as a mechanism that saves the payer from imposing penalties. This situation is allowed under certain conditions. If corrective reporting is submitted to the inspection after completion deadline for filing a declaration and the period of deduction of payment, the subject is exempt from liability if:

- Documents were sent until the person found out that the control body revealed the fact of a decrease in the amount payable or the appointment of an on-site inspection. In this case, before the provision of corrective reporting, the entity deducted the missing payment and interest.

- An updated declaration was submitted after an on-site audit for the corresponding period, as a result of which no errors or non-reflection of any information leading to an underestimation of the amounts payable were revealed.

Exemption from liability implies the exclusion of penalties. In this case, the obligation to pay interest remains. This is due to the fact that they do not apply to tax liability measures. In addition, the Decree of the Supreme Arbitration Court of the Russian Federation No. 5 dated 02.28.2001 established that in these cases the exemption from liability defined in Articles 120 and 122 of the Tax Code is meant.

Conclusion

The issue regarding the offsetting of tax amounts according to the corrective declaration is decided by the control body after registration of the amended reporting. Inspection may refuse the subject. In this case, the updated declaration will only be registered and taken into account. If the decision is positive, the employee of the Federal Tax Service must take a number of actions. First of all, he is obliged to cancel the registration of the submitted amended declaration. After that, he applies a special procedure for fixing the correction document. If an error leading to a change in the tax amount is revealed after a three-year period, the entity may not submit an updated declaration.In this case, the provision of a corrective document is not an obligation, but the right of the payer.