In accordance with applicable law, no later than the 25th day of the month following the previous tax period, any company must compile a VAT return. Instructions for filling out should be known to every person authorized for this action, but some cannot understand individual features, and any errors here are quite unpleasant.

What it is?

A tax return is a special tax payer statement:

- about the expenses incurred and profit;

- various objects subject to taxation;

- tax base and benefits;

- main sources of income;

- calculated tax amount;

- other information that may serve as a basis for calculating and making tax payments.

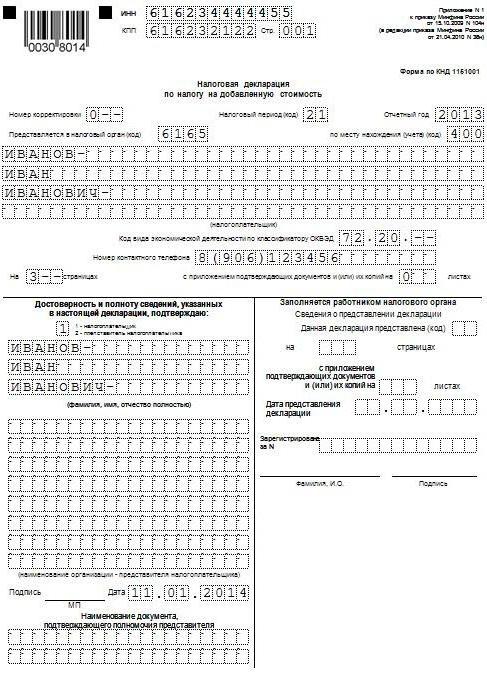

Each company at its place of registration with the Federal Tax Service in accordance with the established formats must be provided in electronic form with a VAT return. Instructions for filling out include all the basic requirements for the information posted in such documents. It is enough to do everything right and exclude any errors. It is also worth noting the fact that all relevant documentation must be attached to the declaration, the list of which is also determined by the current Tax Code.

It is important to know

Not everyone knows that since 2014, a new edition comes into force, according to which each taxpayer or tax agent without fail, must provide the Federal Tax Service at its place of registration with a specialized declaration in electronic form in the specified format through specialized communication channels using the EDI operator. However, there is no difference in how many employees work in the company - in any case, a VAT return must be drawn up. The instruction on filling out until December 31, 2013 stipulated the need to be guided by paragraph 3 of Article 80 of the current Tax Code, which allowed reporting on paper if the average number of employees was less than 100 people. Also, in electronic form, any documentation can be provided, which according to the Tax Code must be presented along with the declaration.

Who can take on paper?

If various organizations and individual entrepreneurs for the three previous months had in total revenue from the sale of any goods excluding VAT no more than two million rubles, then in this case they should not draw up the corresponding VAT declaration. The filling instruction also provides for the complete exemption of such persons from any duties of the taxpayer.

But at the same time, do not forget that if such a taxpayer decided to issue an invoice to the consumer, in which he allocated the amount of tax, then in this case it must be submitted to the state budget. Accordingly, in this regard, step-by-step instructions for filling out a VAT return should already be observed and the particularities of compiling this document should be taken into account.

Taxpayers who decide to switch to UTII, Unified Social Tax, USN, or PSN cannot be recognized as VAT payers, but those companies or entrepreneurs who use “imputed” -NVD or “simplified” -USN will still have to pay taxes on import to the territory of Russia of any goods.Among other things, in the case of using UTII, Unified Social Tax, USN or PSN, step-by-step instructions are also provided for filling out a VAT return if various operations are carried out under simple or investment partnership agreements, as well as trust management of any property or concession agreement.

If a company issues a VAT invoice in which the VAT is allocated, it must also pay this tax with the submission of a corresponding declaration. In other words, the organization that uses the simplified tax system with the “income” object of taxation issues an invoice to its customers where VAT is allocated, which automatically obliges it to fully pay this tax to the state budget and submit to the appropriate authority all the documents as This is required by the instructions for filling out a VAT tax return. At the same time, when calculating the single tax, the amount of VAT should not be included in the total profit.

Submission of a single simplified declaration

If a tax payer is not involved in any operations during which money is transferred through his bank accounts, and also does not dispose of any objects of VAT taxation, then in this case the instructions for filling out a VAT tax return provide for the possibility of providing them simplified declaration. The Federal Tax Service says that for such payers there is no requirement to submit all documents exclusively in electronic format.

What will happen if you do not imagine?

Any company must submit a VAT return in a timely manner. Instructions for filling out, specifics of the current legislation and legal norms - all this clearly indicates that the documents must be submitted on time, otherwise the company will be fined 5% of the tax itself. This penalty will have to be paid for each incomplete or full month of delay from the day that is set last for the filing of this declaration, while the total amount of the fine cannot exceed 30% of the total tax or be less than 1000 rubles.

Filling example

Next, we will present a standard example of how the VAT return is filled out (instructions for filling out). The conditions for submitting this document vary depending on the area in which the company operates and how large the business is. We use tax accounting data provided by Gazprom for the first quarter of 2015. All operations related to the sale of products are taxed at a rate of 18%, and all operations that must be taken into account in the process of preparing the declaration are indicated below:

- October 2014 VAT was paid to the budget, which is withheld from payment of rent of various municipal property in October, November and December 2014. Rental of property is carried out in accordance with an agreement concluded with a committee engaged in the management of property of the city of Mytishchi in the Moscow region. The total rental price is 600,000 rubles (including VAT in the amount of 91 525 rubles). On October 2, 2014, invoice No. 502 was issued for the amount of VAT, which was withheld from rent for the fourth quarter of 2014, which was recorded in the purchase book - 600,000 rubles. (including VAT in the amount of 91 525 rubles).

- January 2015 An advance was received from Gamma LLC for the future delivery of finished products in accordance with agreement No. 1. On January 14, 2015, an invoice was issued for advance payment to Hermes, which was recorded in the sales book - 2 360 000 rubles. (including VAT in the amount of 360,000 rubles).

- January 2015 According to the contract No. 2, OOO Master, finished products were shipped. On January 19, 2015, the “Master” was issued an invoice No. 2, which was recorded in the sales book - 590,000 rubles. (including VAT in the amount of 90,000 rubles).

- January 2015 VAT was paid to the budget, which is withheld from payment of rent of municipal property in January, February and March 2015. Rental of property is carried out in accordance with an agreement concluded with a committee involved in the management of municipal property of the city of Mytishchi, Moscow Region. The total rental price is 600,000 rubles (including VAT in the amount of 91,525 rubles). In the amount of VAT withheld from rent for the IV quarter of 2014, invoice No. 3 dated January 20, 2015 was issued, which was recorded in the sales book - 600,000 rubles. (including VAT in the amount of 91 525 rubles).

- February 2015 An advance payment is transferred to the materials supplier, who is Modus LLC, in accordance with agreement No. 3. On February 3, 2015, Modus compiled and submitted invoice No. 45, highlighting the amount of VAT that was registered in the purchase book for a total of 236,000 rubles (including VAT in the amount of 36,000 rubles).

- February 2015 The materials necessary for the manufacture of products in accordance with Agreement No. 4 were purchased and accepted from Modus LLC. All materials in the IV quarter of 2014 were paid in advance, and from this advance was accepted for VAT deduction in the IV quarter of 2014. On February 5, 2015, invoice No. 150 was received from Modus, which was recorded in the purchase book. On October 22, 2014, an invoice for prepayment No. 1230 was issued, which was recorded in the sales book for a total of 1,770,000 rubles (including VAT in the amount of 270,000 rubles).

- March 2015 In accordance with agreement No. 5 concluded with RAO EU LLC, finished products were shipped. On March 16, 2015, RAO EU LLC issued invoice No. 4, which was recorded in the sales book for a total of 1,062,000 rubles (including VAT in the amount of 162,000 rubles).

In accordance with paragraph 3 of the current procedure, the report does not include sections 4, 5, 6, 7, 10, 11, 12, as well as separate appendices to sections 3, 8, and 9, that is, they should not include VAT return. The filling instruction (filing conditions) provides for a ton of other subtleties that also need to be taken into account.

Key Features

Filling of the 10th and 11th sections should be carried out only if invoices were received or issued within the framework of the activity in the interests of other persons, based on:

- on commission agreements or agency agreements;

- freight forwarding agreements, if according to them, only income received as remuneration is taken into account as part of the income for which the VAT return must be submitted, instructions for filling out (basic rules);

- performing various functions of the developer.

It should be noted that in this case, not everyone should submit a VAT return. Instructions for completion (rules) provide for the fulfillment of these obligations in the event that the entrepreneur (organization) with whom this document is filled out meets one of the following conditions:

- is a tax payer;

- released from the duties of a taxpayer related to the establishment and payment of VAT, or, in principle, is not a payer of this tax, but at the same time acts as a tax agent.

This list does not include persons who are not payers of this tax (if they are not tax agents) and who, accordingly, should not draw up a VAT return. Instructions for completion, deadlines and other nuances by such persons should not be taken into account, but if they issue some invoices in the process of conducting intermediary activities on their own behalf, it will be necessary to submit to the tax authority a detailed journal of accounting for issued and received invoices in electronic form form using telecommunication channels. This must be done no later than the twentieth day of the month following the expiring quarter.

Error free filling

Instructions for completing the declaration for VAT refund to many people it may seem quite complicated, therefore, in order to avoid mistakes, the tax service has developed and shown on the official website all the necessary control ratios. It is worth noting that it provides not only arithmetic control of various reporting indicators, but also logical. In the overwhelming majority of cases, such ratios are laid into their products by developers of specialized accounting programs, with the help of which the VAT declaration is more easily filled. The instructions for filling out (see the sample declaration above) on the official website provide an approximate understanding of how inspectors can respond in the event of any discrepancies in the 2016 VAT declaration.

It is also worth noting that on the website of the Federal Tax Service of the Russian Federation you can find control ratios for a number of other taxes.

Instruction manual

The Federal Tax Service of the Russian Federation has developed its own guidelines on how to fill out a VAT return (instructions for completion). The detailed instructions include a recommended list of actions for taxpayers to follow after submitting a special requirement. It is worth noting that this requirement is sent if the tax authority identifies any inconsistencies or contradictions, and at the same time contains a complete list of transactions for which discrepancies were detected.

Procedure

The order itself is as follows:

- A receipt is handed to the tax authority stating that the requirements for the TCS were electronically accepted within six days from the moment the request was sent to them;

- Regarding all the records indicated in the received request, a detailed check of the correctness of filling out the declaration is carried out, and the record reflected in it is checked against the drawn up invoice. Particular attention is paid to the correctness of filling in various details of records for which discrepancies were found. It can be numbers, dates, the correctness of calculating the amount of tax, sum indicators. If the deduction of the invoice was carried out in parts (that is, several times), then in this case, an additional check of the total amount of VAT is carried out, which was accepted for deduction for all records of this account, including also accounting for previous periods.

- It seems clarified declaration which indicates the correct information in the event that any errors are identified in the declaration that lead to a decrease in the total amount of tax payable.

- If the error indicated in the declaration did not affect the amount of VAT, then in this case, detailed explanations are provided with the correct information. Updated declarations are also recommended. Explanations can be presented in free form on paper or have a formalized form through the operator EDI. In order to send explanations in a formalized form, you first need to make sure that the EDI operator or the developer of the accounting system you use has such an opportunity.

- If after checking the correctness of filling it was not possible to find any errors, a notification about this will be sent to the appropriate tax authority through the submission of explanations.

It is also worth noting that when exporting to the countries of the Customs Union, the instructions for filling out the VAT return (Belarus and Kazakhstan) must also be followed, and this should also be taken into account when filling out papers during such transportation.

All these features must be taken into account when filling out such documents. A lot of attention is paid to the preparation of the tax return, as well as the correctness and availability of small details, so you need to make sure that all of them are present, and your company was not ultimately fined due to some minor flaws.In addition to penalties, re-filling and double-checking all the documentation is an additional loss of time that no one needs either.