A tax return is an official statement by the payer about the income received by him for a specific period, the benefits and discounts that apply to them. This document is submitted to the authorized body in a special approved form. Based on the information contained in it and the tax rates applicable at the time of delivery, the Federal Tax Service monitors the amount of the fee payable. The legislation contains many different options for creating an enabling environment for entrepreneurs. Those subjects who for one reason or another were forced to suspend their activities did not go unnoticed. For such entrepreneurs, a single simplified tax return is provided. Consider this document in more detail.

General information

The single simplified tax return, the model of which is presented in the article, was approved by order of the Ministry of Finance No. 62n. This document is submitted to the authorized control body by entities that are payers of several fees, but did not carry out activities during the reporting period, did not carry out any operations that entailed the transfer of funds at their cash desks or bank accounts, and which do not have objects of taxation on these deductions. Simply put, a single simplified tax return is a form of summary information on zero reporting. The procedure for its submission is regulated by paragraph 2 of Art. 80 Tax Code. Document form on KND 1151085.

Important point

The single simplified tax return form is intended for those entrepreneurs who, during the reporting period, did not have any movement of funds on their accounts or at the cash desk. Some subjects misunderstand this rule. A number of entrepreneurs believe that a complete lack of funds is a lack of income. It should be noted that the costs of the enterprise act as the movement of money. In accordance with the provisions of chapters 21, 25, 30, 24 of the Tax Code, the payer is not exempted from the obligation to pay fees to the budget if he did not sell services, work, goods.

Features

The single simplified tax return for individual entrepreneurs, in essence, replaces the reporting of three mandatory payments:

- VAT.

- Deductions from income.

- Property tax.

But there are situations when a payer who does not conduct business and does not receive income cannot use UDMD. For example, fixed assets are leased, the payment for which affects the amount of profit and should be reflected in the corresponding declaration. In this case, a non-operating enterprise suffers losses. Lease can be paid with r / s and be indicated with VAT. In this case, the organization submits reports on the tax on ext. cost. If an enterprise has an employee, it is paid a salary. This, accordingly, entails the expense of the organization. In such cases, a single simplified tax return cannot be used.

Single case

A single simplified tax return is submitted by a newly created company that does not conduct business, has not yet opened a bank account and does not have fixed assets on its balance sheet. This means that the authorized capital of the organization should be formed from assets that are not subject to taxation.

General order

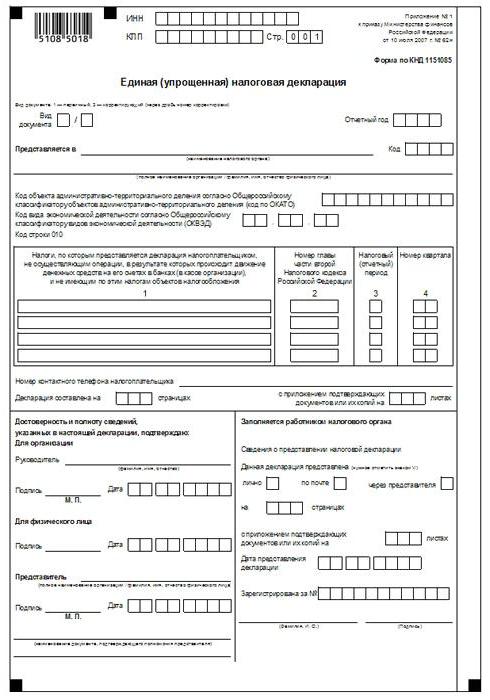

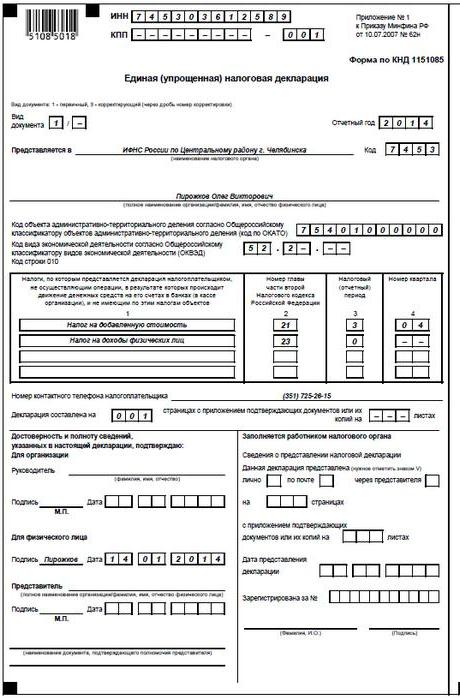

The single simplified tax return consists of 2 sheets.The first indicates those types of deductions for which, in fact, reporting is provided. The second sheet contains information about the payer - an individual who is not an entrepreneur. The quarter is the reporting period for which a single simplified tax return is presented. The deadline is no later than the 20th day of the month that occurs after the end of the period. The document is presented to the Federal Tax Service at the location of the organization or the address of the individual. Reporting is submitted in electronic or paper form.

The payer may come to the Federal Tax Service in person or send his representative to the service. The law also allows the sending of documents by mail. If the payer misses the deadlines for submitting a single simplified tax return, a fine is imposed on him under Article 119 of the Tax Code. When sending a document by registered mail, it is necessary to draw up an additional inventory of investments. In paper form, 2 copies of reporting are provided. In electronic form, the declaration is submitted directly through the website of the Federal Tax Service or by agreement through EDI. If the document is presented by the representative, he must have a power of attorney confirming the relevant authority.

Single simplified tax return: sample form (rules)

In general, the document is not much different from regular reporting. Nevertheless, when compiling it, you should adhere to a number of rules. A single simplified tax return can be filed on a computer or manually. For individual entrepreneurs, information should be entered only on the first page. When filling, it is allowed to use black or blue ink. On both pages of the reporting information must be entered to individuals who are not entrepreneurs and do not indicate TIN. Corrections in the declaration are not allowed.

Page 1

In the "INN" field, organizations and individual entrepreneurs should indicate their taxpayer number in accordance with the certificate issued by the Federal Tax Service for registration. Individual entrepreneurs do not fill out the “KPP” column. Accordingly, information here is provided only by organizations. The column "Type of document" is completed as follows:

- If the reporting is provided for the first time - put "1 / -".

- If the first correction, indicate "3/1".

- If the second correction is "3/2".

In the column "Reporting year", respectively, indicates the year in which UDMT is provided. In the line "Provided in ..." enter the name of the department of the Federal Tax Service, which provides a simplified declaration. If a person submits a document, his full name are indicated without abbreviations (in full, according to passport data). Organizations enter their full name. In the line "OKATO Code" indicate the OKTMO code (changes introduced since January 1, 2014). In the column "Code of the type of economic activity according to OKVED" enter the digital designation by classifier. Codes are present in the extract of the USRLE or the USRIP.

Tables

Columns 1 and 2 indicate line by line the name of the taxes for which a simplified declaration is submitted. Deductions must be made in accordance with the established numbering of the chapters contained in the second part of the Tax Code. Further, the document contains Appendix 1. In its second column indicate the number of the relevant chapter of the Tax Code. If as tax period the quarter appears, in the cell three boxes are marked 3. The fourth line indicates, in fact, the number of the quarter itself for which reporting is submitted:

- The first is 01.

- The second is 02.

- The third is 03.

- The fourth is 04.

For budget deductions, the tax period of which is established in a year, and for reporting - half a year, a quarter, nine months, in the corresponding cell of line 3 enter the period value:

- Quarter - 3.

- Year is 0.

- 9 months - 9.

- Six months - 6.

A dash is put in the column itself.

additional information

In the line "Payer’s contact telephone number" indicate the number in any format.In the column "Declaration framed on the pages" enter the number of sheets that make up the document (002, for example). In the line "with the application of certifying (confirming) documents or their copies" indicate the number of sheets attached to the statements. If they are absent, a dash is put.

Validation

The completeness and validity of the information must be certified:

- Only by the signature of the payer, if he is an individual (including an entrepreneur).

- The name of the document confirming the authority (power of attorney), if the document is presented by a representative of the subject.

- Signature of the head with decryption, seal, if the declaration is submitted by the organization.

In all cases, the date of compilation of the document is necessarily set.

A responsibility

The legislation establishes various sanctions for entities that violate the deadlines for filing a tax return. In case of untimely submission of reports to an individual entrepreneur, a fine of 1 thousand rubles may be imposed - in case mandatory contributions were made to the budget. If the tax has not been paid, then a penalty is charged additionally in the amount of 5% of the amount owed, but not less than 1 thousand rubles. It should also be noted that if the entrepreneur did not have the right to submit a simplified declaration, but handed it in, he faces a fine on unrepresented reports regarding those taxes on which he should report.

What should I do if IODN is presented by mistake?

In practice, there are situations when a simplified declaration has been submitted, and then on the current account or at the cash desk the movement of funds has begun or an object of taxation has been identified. What to do in this case? In this situation, you should file clarified declarations for taxes reflected in a simplified document. In this case, the adjustment number will be 1. The primary reporting in this case is a simplified declaration submitted earlier. No clarifications are provided for UDM. This provision is based on letters from the Ministry of Finance and the opinions of the courts.

Conclusion

Cases when it is allowed to submit a single simplified reporting are clearly defined in the legislation. First of all, this is the lack of cash flow at the cash desk or on the accounts of the enterprise. It is not only about the receipt of profit, but also about the commission of expenditure operations. The lack of cash flow on the cash desk and settlement accounts is actually a suspension of any activity of the enterprise. That is, in this case, neither income nor expenditure operations can be carried out. This point must be clearly understood in order to avoid problems with the tax service.

The legislation does not contain any restrictions on the number of UNDM grants. This means that an entrepreneur can file simplified tax reporting over several periods. The introduction of this document into circulation can significantly save time as a control service, and the payer. A simplified declaration consists of only two sheets, the completion of which, as a rule, is not accompanied by any difficulties.