Different methods are used to evaluate long-term assets (fixed assets, stocks, etc.). One and the same object can be characterized by several numerical values of its value. The key concept in accounting is book value. With its help describe the financial situation of the company and make its assessment. In the article, we consider the features of the definition of this indicator and its characteristics.

OS carrying amount

Form No. 1 is the most important document necessary for the analysis of the economic activity of an enterprise. It is he who gives an idea of the assets and liabilities of the subject. Assets comprise the assets of the enterprise - current and fixed. Accounting for the latter is sometimes difficult: they are repeatedly and continuously used, which affects their cost, but it still needs to be calculated. To simplify this procedure, the concept of book value was introduced. It is used to record the movement of assets and their presence in the enterprise.

The carrying amount of an asset is the amount of its initial cost minus accrued depreciation. Based on the definition, it is clear that for the calculation it is necessary to know two more indicators. The key is the concept of historical cost, because it is also used to calculate depreciation. It is defined as the sum of all expenses for the acquisition or manufacture (construction) of an object, including delivery and installation costs and excluding the amount of reimbursable taxes. Thus, in order to take the asset into account, it is necessary to deduct the accrued depreciation from the initial cost of the object. The balance of the amount is the carrying amount, which is often symbolically referred to as the residual value.

Revaluation of OS: reflection in the balance sheet

Once a year the company carries out revaluation of fixed assets. This is necessary so that accounting data does not lose its reliability and relevance. OSs have the ability to become morally and physically obsolete, which is why their cost also changes. If after revaluation of the property it is found that the price of the asset has decreased or increased, the residual value is recalculated as follows:

- Determine the replacement value of the object at the valuation date.

- If the value of the property has decreased, a markdown is made. In the balance sheet indicate the calculated amount minus depreciation.

- In the event of an increase in value, fixed assets are reassessed by restating depreciation. Changes are made to the balance sheet.

Property revaluation results are attributed to Extra capital, i.e., either its increase or decrease occurs.

Real estate in the balance sheet

Valuation of real estate is performed to determine its value before selling or buying, leasing and in many other cases. Depending on the direction of activity of the enterprise, objects can be recorded according to their initial cost minus depreciation, or at the current market price.

Investment property is recorded at the end of the reporting period at fair value as determined by the international valuation company. Sometimes it is not always possible to compare the objects of the enterprise with the market, which leads to a deeper analysis. The book value in this case is determined taking into account the profitability of the property.

The residual value of intangible assets

Intangible assets are property that does not have a tangible form. They, like fixed assets, are non-current assets and can be used in the production, marketing or management process.Intangible assets, according to IFRS, evaluate one of two methods:

- at historical cost (cost of acquisition or manufacturing) less depreciation;

- at replacement cost calculated as a result of revaluation, less accumulated depreciation charges.

All costs of intangible assets arising after the moment of their acceptance for accounting are recognized as other expenses. If the funds are used to improve the properties of the asset, which ultimately leads to an increase in their profitability, capitalize the costs.

Description of assets in the balance sheet

The carrying amount of assets is the sum of all funds of the company, which are reflected in accounting form No. 1. Its value is indicated in line 1600. If it is necessary to calculate the residual value of one of the assets, they perform the steps described above: they determine the initial or replacement value (in case of revaluation) and deduct the depreciation amount from it.

Depending on the purpose, it is possible to calculate the value both for an individual object and for their group. The concept of book value of assets is also widely used. Its indicator perfectly characterizes the financial well-being of the enterprise, which is interesting to third-party organizations (investors, lenders). The book value of assets is the aggregate of all funds, which is calculated as the sum of lines 1100 and 1200 of form No. 1 of the financial statements.

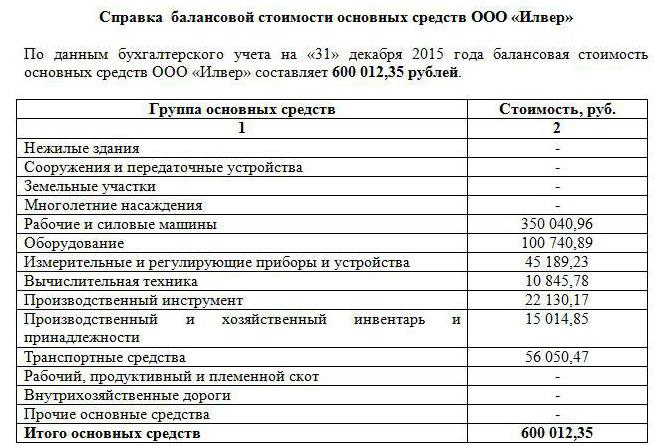

Asset residual value statement

As mentioned above, the asset value indicator is very informative. Any company interested in this can request data. Usually in their role are potential investors, lenders, buyers. At the request of third-party individuals and legal entities, a statement is drawn up on the book value of the assets of the enterprise.

The established form for its filling does not exist, but usually it is formed like the old balance. For this, the value of each group of assets at the beginning and end of the period is indicated line by line. If necessary, the data is specified, in more detail describing certain types of funds. The main thing is that the information is true.

The certificate must contain the name of the company, the date on which it was compiled, as well as the signature of the head and chief accountant. Content can be presented in a table (like a balance sheet) with a breakdown into the necessary groups of assets or in the form of a solid text. Regardless of the chosen method of compiling the certificate, it is necessary that the residual value of the company's funds at the beginning and end of the reporting year be indicated in it.

Book value

In the economic analysis, in addition to the indicator of enterprise funds, the value of net assets is also used. For its calculation, the sum of lines 1400 and 1500 is deducted from the value of line 1600 of the balance sheet. Thus, net assets show the amount of funds of the enterprise formed at the expense of equity and not burdened with obligations.

When calculating the book value of a security, they speak of a shareholder in the capital of an enterprise. The indicator is defined as the ratio of net assets to the number of issued ordinary shares. Moreover, the residual value of securities often does not coincide with their valuation in the market. It should be borne in mind that they do not take into account their own shares repurchased from shareholders.

If the company possesses not only ordinary, but also preferred shares, then the calculation will be somewhat more complicated. The carrying value of securities in this case is defined as the difference between net assets, dividend arrears and the cost of redemption of preferred shares.

Residual value of the enterprise

An organization is also a kind of property that can be valued or sold.To study the effectiveness of economic activity, annually compile form No. 1, which reflects all the means of the enterprise and the sources of their education. On its basis, the book value of the enterprise is calculated. Use the following formula: Bst = Hbut - Nbutwhere:

- Hbut - net assets;

- Nbut - intangible assets.

Net assets can be replaced by the difference in equity and liabilities of the enterprise.

So, the carrying amount is a value that reflects the original acquisition price less depreciation. Its value is indicated in the balance sheet for each type of property. If necessary, reassess the funds, and then recalculate their residual value. In determining the carrying value of shares and enterprises use the concept of net assets.