Conducting accounting involves the mandatory inventory of enterprise funds. An exception was not made by such type of assets as work in progress (work in progress). These are the remains of objects of labor that did not manage to go through all stages of processing and did not become finished products. An inventory of work in progress is a reconciliation of accounting data with the actual presence of unfinished products and their completeness.

What is work in progress?

This is a kind of asset group, which no longer applies to materials, but also does not constitute a finished product. Accounting standards give them a clear definition. According to PBU, work in progress is products or work that has not passed all stages of the process, acceptance or testing. This also includes:

- incomplete products;

- orders outstanding;

- self-made semi-finished products not related to the finished product;

- services and work not accepted by the customer;

- semi-finished and processed materials;

- units, parts, assembly connections.

To account for the costs of the production process, active bills 20–29. Expenses are collected in the debit, and they are written off (distribution) on the loan. The balances on these accounts at the end of the month characterize the cost of work in progress.

Assessment Types

In accounting, data are reflected in physical and monetary meters. To accept or write off funds, you need to know their value. Work in progress assessment is carried out by:

- Actual costs incurred (in unit production).

- Actual cost is the most reliable and common way. The volume of work in progress is determined. Then its quantity is multiplied by the average unit cost, thereby determining the actual production cost of all work in progress at the end of the month.

- Standard cost - applicable for serial and mass production. The accounting price of the wage unit is applied. Additionally, the deviation of the planned value from the actual value is kept.

- For articles of direct costs - the price of a unit of work in progress is calculated by summing the direct costs of its creation.

- Costs of refineries - in the cost of refineries include only materials, raw materials or semi-finished products. The method is mainly used in material-intensive production.

The company itself must choose the most appropriate method for assessing the income tax and write it in the accounting policy. The rest of work in progress is estimated on the basis of the primary documentation, and its size is established after the inventory at the end of the month.

Long-cycle products

Industrial production sometimes produces products that go through several stages of processing. At the same time, enterprises can recognize the fact of sale at different points in time: at certain stages of the work or after its complete completion. The second option is usually used.

If the products are handed over in stages, then there is a need to use account 46. The debit indicates the parts of the work paid by the customer and completed by the enterprise.After all the stages are completed, the value of the object accumulated in account 46 is debited to the account “Settlements with customers and customers”.

Organization of inventory of work in progress

The specifics of the inventory is indicated in the accounting policies of the enterprise. With the exception of mandatory checks, the following organizational issues are established regarding the planned calculation of the number of assets:

- list of property subject to procedure;

- the total number of inventories that are planned to be carried out in the reporting period and their dates;

- composition of the commissions;

- other information.

A compulsory inventory of work in progress is carried out when a fact of damage or theft of labor objects in its composition, the change of responsible persons and some other cases is revealed.

Regardless of the reasons for the inspection, the process is carried out according to the instructions of the Ministry of Finance (order No. 49). First of all, the manager issues and signs an order that contains information about:

- reasons for the audit;

- groups of property falling under the process;

- the composition of the commission involved in the inventory;

- start and end date;

- the period during which documents must be submitted to the accounting department.

The order is a kind of task for the inventory commission. It consists of accountants, administrative staff, and other specialists. A prerequisite is the presence of financially responsible persons. Representatives of an independent audit service may also be involved. The presence of each member of the commission is mandatory, otherwise the results of the audit are considered invalid.

The procedure for conducting an inventory of work in progress

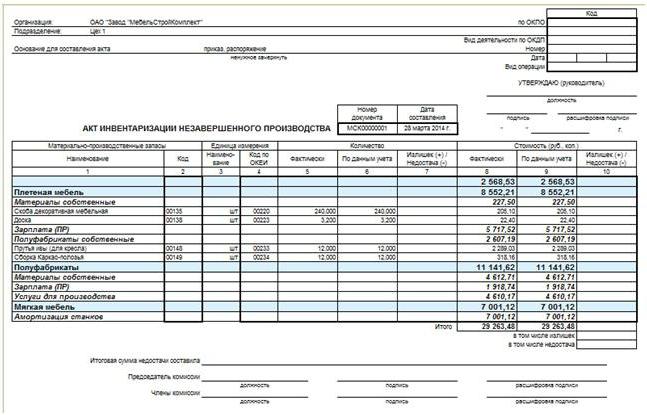

The chairman of the commission puts visas “Before the inventory on the n date” on all expenditure and receipt documents received for the inventory. This is necessary to record data on property balances before the start of the audit. Materially responsible persons provide receipts that all primary documents have been handed over, the property received is capitalized, and the retiring property is written off as an expense. Then an inventory of work in progress can be carried out.

Begin the calculation of the actual availability of property. Information on its quantity is recorded in acts or inventory records, which are at least in duplicate. The document is numbered, it indicates the date of the audit, the date and release number of the order of the leadership about its organization. Next, tables are compiled for each workshop and the location of work in progress. After filling out the document, members of the commission and financially responsible persons sign it. The latter additionally provide a receipt that the verified volume of work in progress has been accepted for safekeeping.

Unfinished Construction Inventory

Inspection of capital construction objects is carried out for each structural element, type of work, equipment and its other components. In this case, the commission needs to find out:

- whether the objects transferred to installation works, but not yet touched by them, are included in the number of work in progress;

- In what condition are the objects on conservation and the construction of which is temporarily stopped.

Separate acts are drawn up for commissioned, but not properly adopted buildings. A similar measure is also applied to facilities whose delivery deadlines are delayed for some reason.

Separate acts are drawn up for commissioned, but not properly adopted buildings. A similar measure is also applied to facilities whose delivery deadlines are delayed for some reason.

WIP inventory and industrial production

At enterprises of this type, the commission checks the availability of all materials, raw materials, as well as the completeness of units, backlogs and installations. All unnecessary inventories are delivered before inventory from the workshop to the warehouse. For each separate unit draw up an act or inventory.Separate documentation is subject to raw materials, materials and semi-finished products that have not been processed, but were located near workplaces. The inventory of landlords does not include rejected items.

An inventory of work in progress at an industrial enterprise is carried out in order to verify:

- the presence of backlogs, aggregates, units, parts;

- quantities of unfinished products;

- completeness of units, assemblies, parts;

- balances of work in progress for orders whose execution is canceled or suspended.

Backlogs, components, assemblies and parts are counted, measured and weighed. Data is entered in the relevant acts or inventories.

Work in progress at the enterprise, which is a mixture of different raw materials or heterogeneous mass, is characterized by two indicators: the total quantity and the part attributable to each item in its composition. The calculation procedure is regulated by industry instructions, and in their absence is prescribed in the accounting policy.

Reflection of inventory results

The acts and lists of inspections are transferred to the accounting department within the prescribed time. Discrepancies found during the inventory between the data of the primary documents and the actual availability of property must be reflected in the accounts.

In the case of excess surplus income, it should be capitalized at market value by the date of the audit. Work in progress in accounting is recorded on accounts 20–29. The amount recorded in the debit of the account on which the excess was found: Dt "Auxiliary production" CT "Other income."

The shortage or damage to the work in progress is shown in the credit of the accounts for the accounting of production costs. At the same time, accounting entries look like this: Dt “Shortcomings” Kt “Servicing production”, Dt “Losses from damage to values” Kt “Main production”. If the detected shortage does not exceed the rate of natural loss, then its amount is attributed to the distribution costs: Dt “Main production” Kt “Shortages”. Such write-offs are made on the basis of the calculation recommended by the accounting policy.

Reflection of shortages in excess of established standards

Accounting policy the enterprise establishes certain standards, including a part of the loss of property is considered acceptable. In cases where the shortage occurs due to damage to the work in progress, there are two options for reflecting the results in accounting:

- If the perpetrators are identified, then restore the shortage at their expense. Accounting entries are as follows: Dt “Calculations for damages”, CT “Lacks”, Dt “Calculations for damages” Kt “Losses from damage to property”.

- If the court refused to recover damages from the guilty persons, or those have not been established, then the deficiency is written off as a financial result: Dt “Other expenses” Kt “Shortages”.

- If a damage to property occurred due to an emergency and force majeure, the order of reflection of losses is similar to paragraph 2.

Amounts of shortages above the norm oblige the inventory committee to conduct an internal investigation in order to identify the perpetrators.

Work in progress in accounting has a special place in the assets of the enterprise. This is no longer raw materials, but also not finished products. Control over its quantity is as important as for any other property. In order to verify the data of the primary documents with the actual availability of work in progress, take inventories, as a result of which the indicators are adjusted, if necessary.