To account for production costs in the BU, several accounts are used. The expenses of the main auxiliary production marriage, reserves for future expenses. Direct costs are displayed on accounts 20 and 23, and indirect costs 25 and 26. Let us consider the main production in more detail.

Accounting accounts

All expenses that are directly or indirectly associated with the production and manufacture of products are charged to its cost. They accumulate on accounts 20-29 balance. At the end of the month they are recalculated and distributed between the main and auxiliary production, individual types of products and work performed.

Primary production

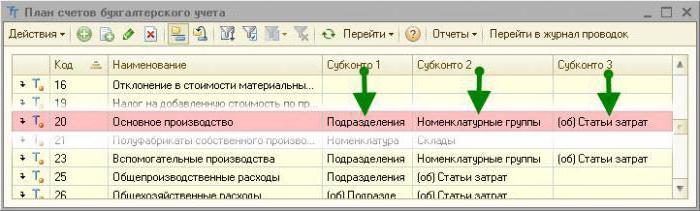

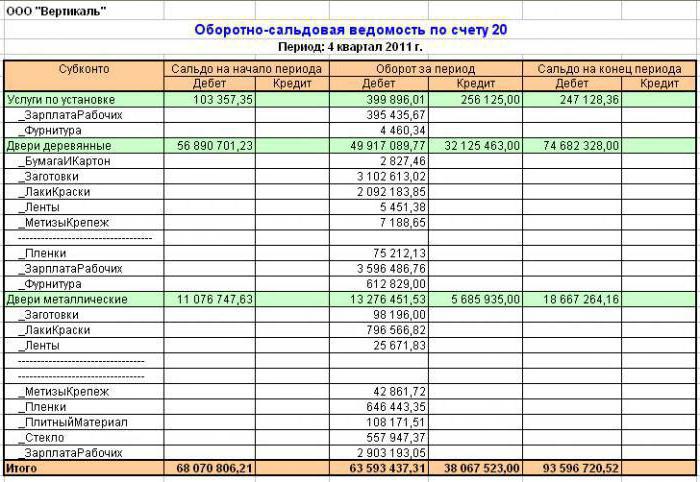

Account 20 in accounting is used to display information about the costs of production, which was the goal of creating the enterprise. Direct costs that are directly related to the production process are subject to accounting. These include the cost of materials and the cost of paying wages to workers.

Correspondence 20 accounting accounts

Consider typical wiring:

- DT20 KT10 - materials are written off.

- DT10 KT20 - return of raw materials to the warehouse.

- DT20 KT10-2 - semi-finished products were released into production.

- DT20 KT10-3 - fuel is written off for technological purposes.

- DT20 KT60 - the cost of electricity used in production was taken into account.

- DT20 KT70 - payroll workers.

- DT20 KT69 - insurance premiums taken into account.

- DT20 KT23 - the costs of auxiliary production are taken into account.

- DT20 KT69 - a reserve has been created for the payment of private pension funds and holidays.

- DT20 KT25 (26) - overhead (general) expenses were written off.

- DT20 KT28 - losses from marriage are displayed.

In the process of activity, an organization may attract services (products) of its own production. In this case, the 20 and 21 accounts are used. Semi-finished products of own production are debited from KT21 in DT20. The final balance shows the value of work in progress (WIP). Analytics is carried out by type of cost, product, units. Account 20 in accounting is reflected in the balance sheet in the second section of assets on the line “Inventories”.

Overhead costs

Indirect costs associated with servicing industries are accounted for in account 25. These include:

- depreciation of machinery and equipment;

- OS maintenance costs;

- remuneration of employees;

- insurance premiums;

- rent;

- utility costs for production facilities;

- expenses for the repair of machinery, buildings for general production purposes, etc.

Within a month, the actual costs are collected for DT from the credit of the accounts for stocks, materials, settlements with personnel: DT25 KT02 (05, 10, 60), etc. Then they are written off to account 20 in accounting. This is reflected in the wiring of the DT20 KT25. That is, the final balance in the middle. 25 equals 0. Analytics is carried out by units and expense items.

General running costs

Indirect costs associated with servicing the organization are displayed on account 26. These include:

- administration salary;

- deductions for social insurance;

- communication expenses;

- costs of maintaining security;

- administrative costs;

- Depreciation of fixed assets for administrative purposes;

- office rental, etc.

Monthly expenses accrue according to DT26. At the end of the month, these amounts are debited to account 20 in accounting or 90-2 in full.

Typical postings to account 26 are filed in a table.

| Operation | DT | CT |

| Depreciation accrued on fixed assets, intangible assets | 26 | 04, 02, 05 |

| Submitted materials for general business needs | 10 | |

| Electricity costs included | 60 | |

| Accrued salary for workers associated with OS maintenance | 70 | |

| Accrued premiums | 69 | |

| Vacation reserve created | 96 | |

| Written off overhead costs associated with auxiliary production | 23 | 26 |

| Written off overhead costs associated with the main production | 20 | 26 |

Non-manufacturing organizations use account 26 to display information on the costs of doing business. Amounts of expenses at the end of the month are debited to DT90 “Sales”. Analytics on account 26 is carried out for each article of the estimate, cost center, etc.

Auxiliary production

Account 23 is used to summarize the information about auxiliary costs:

- energy services;

- fare;

- OS repair;

- manufacturing of tools, building parts, structures.

DT23 reflects expenses directly related to the release of goods, indirect costs and losses from marriage. In this case, the following transactions are formed:

DT23 reflects expenses directly related to the release of goods, indirect costs and losses from marriage. In this case, the following transactions are formed:

- DT23KT10 - materials are written off in auxiliary production.

- DT23KT70 - the salary of production workers was taken into account.

- DT23KT69 - insurance premiums are accrued.

- DT23KT25, 26 - indirect costs are included.

- DT23KT28 - losses from marriage are written off.

KT23 reflects the actual cost of production. These amounts are then debited to account 20 in accounting, sub-accounts "Plant Growing" (20-1), "Livestock" (20-2), "Industrial Production" (20-3), "Other Production" (20-4). The balance of account 23 displays the value of the wage. Analytics is carried out by type of production.

Loss accounting

Defective products are those that do not comply with standards or contracts in quality. If it is possible to bring the products to the desired parameters, then such a marriage is considered correctable. According to DT28, the cost of decommissioned products is displayed. According to KT28 - the amount to be withheld from the culprits, suppliers, the cost estimate of the cost of restoring the product.

Let's consider typical postings (for convenience we will again present them in the form of a table).

| Operation | DT | CT |

| Remedy materials rejected | 28 | 10 |

| Accrued salaries to employees correcting products | 70 | |

| Accrued premiums | 69 | |

| Written off the cost of rejected products | 20 | |

| The cost of marriage is deducted from the salary of the perpetrator | 70 | |

| Defective parts are capitalized | 10 | 28 |

| Claim submitted to suppliers | 76-2 |

The cost of defective products is debited from DT28 to account 20. Closing an account means that all losses from the barge are compensated. Analytics is carried out by units, articles costs, types products, culprits and causes of marriage.

Service Farms

Score 29 Designed to display information about the costs of production not related to the manufacture of products, the provision of services:

- Housing and communal services (operation of houses, hostels, baths, etc.);

- workshops;

- buffets and dining rooms;

- child care facilities;

- holiday homes;

- research units.

DT29 reflects the costs associated with the performance of work, which are then debited to the account of auxiliary production. According to KT29 - the cost of work, goods.

| Operation | DT | CT |

| Materials taken into account | 10 | 29 |

| Charged off the costs of units-consumers of services of service industries | 23, 25, 26 | |

| Goods sold to third parties | 90-2 |

Balance account 29 displays the value of the wage. Analytics are conducted for each production, cost item.

Selling expenses

On account 44 displays information about the costs associated with the implementation. Manufacturing enterprises can use this account to display costs for:

- product packaging;

- delivery, loading of products;

- commission fees;

- maintenance of storage facilities;

- advertising;

- entertainment expenses, etc.

Trade organizations on this account display the costs of:

- transportation of products;

- salary;

- rent;

- maintenance of buildings, equipment;

- storage of goods;

- promotion of products;

- hospitality costs, etc.

Amounts of expenses are accumulated according to DT44, and then debited to account 90-2. Analytics is carried out on products and cost items.In case of partial write-off, the costs of transportation and packaging are to be distributed between months (in equal amounts, regardless of actual expenses). All other articles relate to the cost of production monthly in full.

Costing

The final stage is the determination of the cost of production, taking into account the balances of work in progress.

At the end of the month, costs recorded in accordance with DT23 are distributed between basic and general production costs. Then, overhead costs are deducted to account 20 in accounting if short records are kept, and all costs if full cost accounting is kept. That is, the total cost is displayed on this account. Formula:

C / C = NZP beg. + Costs - WIP end.

Actual cost is recorded at CT 20. Costs are written off depending on which valuation method is selected. If the products are taken into account at the standard cost, all expenses are charged to account 40 by posting DT40 KT20. If actual cost is applied, costs are written off to account 43. This is how account 20 is used in accounting.