Cash limit is the maximum allowable amount of money at the cash desk for each working day. The need to constantly monitor surplus cash at the checkout made life difficult for many accountants. From 1.06.14, changes were made to the cash register: some enterprises were exempted from the mandatory establishment of a cash limit.

Need limit

Most transactions, especially those related to the handling of large amounts, are carried out using bank transfers. The cash desk limit was created just to control and reduce cash turnover. Exceeding established standards is allowed only in some cases.

In order to establish real figures for the maximum cash at the cash desk, the frequency of the limit review is not limited to the Bank of Russia. At his discretion, the head has the right to change the size of the limit amount at the cash desk during the month, quarter, year or other necessary period.

Order of Establishment

The cash balance limit is set by the organization independently. The document governing the conduct of cash transactions comes into force after signing by the head of the enterprise. You need to understand that the absence of a establishing document can lead to liability, because the limit will automatically be considered zero, and all amounts in the cash register will be considered super-limit.

The Bank of Russia regulates the setting of a cash limit at the cash desk (By Order No. 3332-U of 03/11/14). The bank, which is obliged to check the data of cash transactions at least once every 1-2 years, monitors compliance with the accepted standards. If inconsistencies and violations are found, a request is sent to the tax service.

Organizations exempted from the established cash limit

After making changes to the procedure for cash accounting, some organizations were exempted from the mandatory establishment of a limit on cash at the cash desk. These include small business entrepreneurs and entrepreneurs. In order to exercise the right to unlimited cash circulation at the cash desk, an enterprise must meet the following criteria:

- the average number of employees for the previous year is not more than 100;

- the amount of revenue excluding VAT for the last year is not more than 800 million rubles;

- share in the authorized capital of third-party legal entities - 25% or less;

- the share of funds in the authorized capital of various funds, organizations or associations does not exceed 25%.

Individual entrepreneurs and small businesses have the right not to comply with the cash limit at the box office from 1.06.15. Organizations registered as small businesses after this date may not set a limit from the moment the status of entrepreneurial activity is recognized.

Refusal of the enterprise from the cash register limit

To refuse to establish the limit value of money at the box office it is not enough just to declare it. Like any enterprise action, it should be documented in the following order:

- If, prior to the refusal, an order to establish a cash register limit was in effect, it must be canceled.

- Prepare and approve the order to eliminate the established cash limit from a certain date.

Drawing up a document on the absence of a limit amount of money at the box office is very important, because when scheduled inspection non-observance of the cash limit will be unreasonable and will entail administrative liability.

Types of fines for violations of the cash desk limit

In cases where the storage of excess amounts is not allowed, the company faces fines under article 15.1 of the Code of Administrative Offenses.Depending on who is responsible, the amounts may be in the amount of:

- 4-5 thousand rubles are paid by individual entrepreneurs and small business officials;

- 40-50 thousand rubles are levied from legal entities (i.e., from an enterprise).

In order to avoid penalties, one should carefully monitor cash transactions and transfer over-limit amounts to the bank on time.

The company may be held liable in cases of such violations as the storage of funds at the cash desk without issuing a receipt order, as well as in case of delay in payment of the amounts allocated from the wage fund.

Legal storage of excess funds at the checkout

According to the instruction of the Bank of Russia, there are cases when the cash register limit of an enterprise can be legally exceeded. The list includes the amounts:

- for payment in salary fund (payment for labor, scholarships, social benefits);

- formed on holidays and weekends, if the organization makes cash payments at this time.

It should be borne in mind that the funds coming from the payroll must be paid within 3-5 days, including the day during which the funds were received at the cash desk.

How to comply with the cash limit?

It is necessary that the management of the enterprise is attentive to the issue of conducting cash business. The limit should be entered according to the cash turnover at the checkout. The determination of amounts not justified by calculations is likely to lead to frequent limit violations.

The rest of the money in the cash register can be seen in the cash book. If a limit amount is found, it should be deposited with the bank. An enterprise has the right to independently determine the frequency of sending funds for crediting to a current account. Only limit amounts are subject to compulsory collection, the distribution of the balance is at the discretion of the organization.

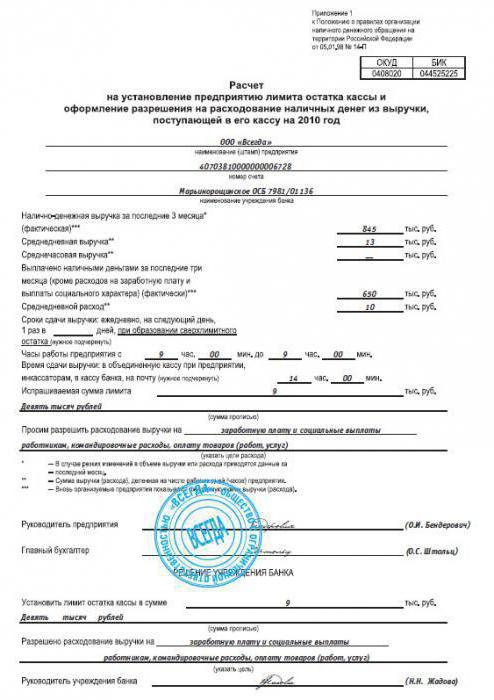

Cash limit calculation

There are 2 methods on the basis of which the maximum allowable amount of cash is calculated at the checkout. If the limit was calculated before 1.06.14, in order to avoid problems with the tax service, it is better to cancel the old order and issue a new one. The cash limit at the cash desk is deduced on the basis of the planned revenue or cash expenses.

The period according to which the cash limit is calculated is set by the enterprise independently. Usually use a quarter:

- preceding the one for which the calculation is made;

- with an indicator of maximum revenue;

- similar to last year.

The billing period includes all the working days of the quarter in question, but should not contain more than 92 days. The resulting limit amount can be rounded up to rubles up or down.

Calculation based on revenue

The method is used when the company receives or plans to receive revenue in cash. To calculate the cash limit, based on the amount of proceeds from economic activity, use the formula L = Ob ÷ Traces × Tinwhere:

- L - limit of funds at the box office;

- About - the amount of revenue received in cash for the period under review;

- Traces - settlement period (quarter) in days;

- Tin - the frequency of delivery of funds to the bank (collection).

Example of revenue calculation

Consider how to calculate the cash limit using the following data: the cash of the trading company “X” receives revenue daily. Billing period recognized the first quarter of last year. Revenue is leased once every 4 days. The company works seven days a week. Perform the steps:

- We calculate the number of working days in a quarter. The condition states that the company carries out activities the entire working week, therefore, the settlement period consists of 90 days.

- The amount of revenue received, which was identified on the basis of data accounts 50, 90 and 62, amounted to 4 856 548 rubles, namely: in January - 1 558 884 p., In February - 1 240 058 p., In March - 2 057 606 p.

- We calculate the cash desk limit for the first quarter: L = 4 856 548 ÷ 90 × 4 = 215 846 p.

Based on the results, the head of the company issued an order approving the limit.

Cash Expense Calculation

If the company uses only non-cash payments, you can set the daily maximum amount of cash at the box office using the amount of cash for administrative expenses. It should be borne in mind that in no case take into account the amounts received from the wage fund.

The cash desk limit calculated for future cash expenses is set using the formula L = Ob ÷ Traces × Tinwhere:

- About - the amount of the issued amounts from the cash desk for general and administrative expenses;

- Traces - Settlement quarter in days (but not more than 92);

- Tin - collection period.

The procedure for rounding the results is the same as in previous calculations.

Sample cash limit calculation based on cash expenses

Consider an example: the organization carries out only non-cash payments. Cash withdrawn 1 time in 3 days. The first quarter of last year is recognized as the billing period. The organization operates 5 days a week. The volume of cash expenses for the indicated period amounted to 1,600,000 rubles. Perform the steps:

- We calculate the number of days in the quarter under consideration: in January there were 15 working days, in February - 19, in March - 22. Total: 56 days.

- According to accounting data, the amount of expenses for January amounted to 520 thousand rubles, for February - 268 thousand rubles, for March - 812 thousand rubles.

- We calculate the cash desk limit for the first quarter: L = 1,600,000 ÷ 56 × 3 = 85,714 p.

Based on the calculations, the head of the enterprise established the maximum permissible amount for each working day in the amount of 86,000 rubles.

In cases where the organization does not make expenses from the cash desk and does not use cash payments, but only pays dividends, the limit is set based on the amount of money issued according to a similar formula. At the same time, it is not necessary to indicate all days of the quarter, because usually funds are withdrawn 1 time per period. The collection period for the calculation use a maximum of 7 days.

Cash Limits for Separate Divisions

An organization with structural divisions sets a cash limit at the box office based on the collection method. For branches geographically independent of the head office, a limit may be set:

- separate - in cases where funds from the cash desk are transferred directly to the bank;

- aggregate - which is part of the head office limit - in cases where cash is leased to the main department.

In the case of the transfer of funds from the cash desk of the units to the central office, the limit should be set taking into account the proceeds of each of the separate departments and distributed according to its share.

The procedure for drawing up the order of cash limit

The document establishing the organization of cash accounting is compiled by each organization independently. A standard form for the order has not been established, but information on:

- release date of the order;

- the amount of the established limit;

- the method and procedure for calculating the limit amount;

- if necessary, cancel the previous order indicating the document number and date.

All other criteria of the official paper of the enterprise are compiled on the basis of the main rules of documentation. Consider the resolution of the head of the enterprise, indicating how to calculate the cash limit. The sample order can serve as an example for drawing up a document in the conditions of another enterprise:

Premium LLP

Order No. 25 dated 09/30/2015

“On Establishing a Limit on Cash Balance at the Cash Desk”

Based on the Bank of Russia Ordinance No. 3210-U dated March 11, 2014,

I ORDER:

- To accept the cash desk limit set for the fourth quarter of 2015 in the amount of 548,985 (Five hundred forty eight thousand nine hundred eighty five) rubles based on the data for the fourth quarter of 2014.

- Set the collection period in the servicing OJSC “Russia-Bank”: 1 time in 3 business days.

- To invalidate the order "On establishing the limit on cash balance at the cash desk" No. 16 dated 06/30/2015.

- To appoint a cashier as the person responsible for observing the cash limit, who is obligated to check the amount of money at the cash desk at the end of the working day on the basis of the data in the cash book.

Gene. Director Signed A. A. Nikolaev

Familiarized with the order:

Chief Accountant date / signature M.P. Andreev

Cashier date / signature P.A. Sovushkina

In an additional order, an enterprise may indicate a calculated sample of a cash register limit.

Based on the above examples, we can confidently say that calculating the cash limit and issuing the corresponding order is not a difficult task in accounting. Paying due attention to the calculation of excess amounts, the company will be able to avoid financial offenses and administrative liability.