Any employee who is directly related to material values can tell what a collation sheet is. He is also able to explain the importance of compiling this document.

Basic concepts

Work with material values is simple only at first glance. It has many features and pitfalls. Here they are trying to find a document called a collation statement. What is it and why is its value rated so high? To begin with, it should be noted that any enterprise constantly keeps records of all available types of values. These usually include:

- fixed assets;

- inventory items;

- finished products;

- intangible assets.

Each of these species in its own way affects the production process. Therefore, for the proper organization of work, it is necessary to have a clear idea of their actual availability. For these purposes, inventories are constantly conducted, based on the results of which then a collation statement is formed.

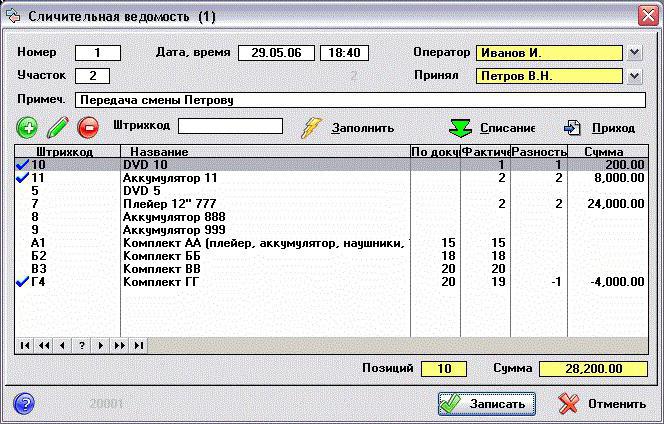

Why is this done and what allows you to see such a document? Almost a comparison sheet allows you to record the fact of a possible discrepancy between the actual availability of specific values obtained as a result of the inventory, and their quantitative indicator according to accounting data.

Correctness of registration

Back in 1998, the Goskomstat of Russia issued Decree No. 88, in which, after making some changes, it approved several unified forms. They were supposed to facilitate the process of conducting primary accounting and increase production control at each of its stages. In this document, the form of collation is presented in two different forms:

- INV-18. It is compiled based on the final results of a preliminary inventory of fixed assets of the enterprise and its intangible assets.

- INV-19. On it is a comparative accounting of all inventory items.

The order of formation of both forms is almost the same. First, the responsible employee, in the presence of a commission specially created for this, conducts an inventory. Then its results are checked with the data that are currently available in accounting. As a result, a new document is formed.

It contains a detailed description of all identified discrepancies. Moreover, each position is signed in detail indicating the reason for the discrepancy. Forms are prepared immediately in 2 copies. One, as a rule, remains with the accountant, and the second takes the materially responsible person.

Checking fixed assets

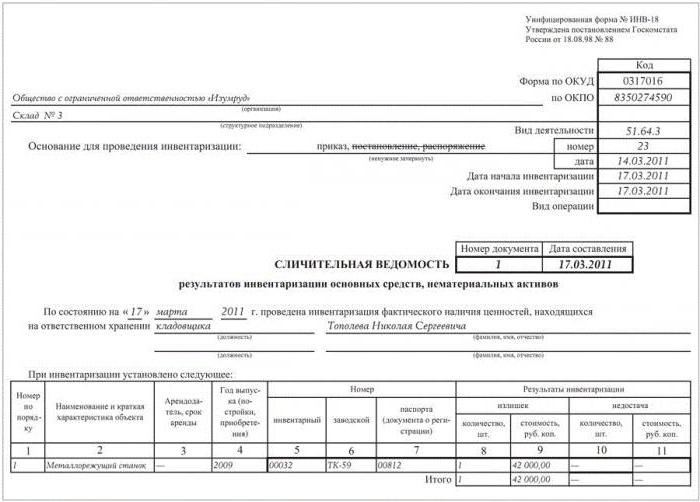

Inventories in enterprises should be carried out continuously. This makes it possible to monitor the status of each indicator and keep abreast of the real situation. For verification of fixed assets and intangible assets, the forms No. INV-1 and No. INV-1a, approved by the same resolution, are used, respectively. After completion of work, a collation statement is drawn up. The sample is a form placed on standard A4 sheets.

On the first page all data about the enterprise are indicated:

- name of the organization and the structural unit where the audit is being conducted;

- codes (OKUD and OKPO), as well as the type of its activity.

Next, the basis for the event (order or order) is indicated with its number and date. Here, the beginning and end of work is recorded.This is followed by the name, date and number of the document itself. Under it is indicated, as of what date the check is carried out, as well as financially responsible person (F. I. O. and position). After this is a table that is placed on both sides of the statement. It includes eleven graphs that fully describe each item being checked. On each page, the inventory result is calculated by calculating the identified surpluses and deficiencies. The statement is signed by both employees, each of whom takes one copy of the form.

Material Check

In a similar way, a comparative statement of the results of an inventory of available inventory items is compiled. An inventory is preliminarily carried out, the results of which then form the following documents:

- INV-3, where the total presence of goods and materials is visible.

- INV-4, which shows the shipped materials.

- INV-5 records the values accepted for safekeeping.

Summarizing all the data obtained, a statement is generated in the form of INV-19.

A “cap”, in which the basic information about the enterprise is indicated, is filled out similarly to the previous form. The following is a table in which there should be thirty-two columns. Each material (product) is signed for all available indicators:

- Columns 1 to 7 contain its description (name, codes, unit of measure, inventory number and data of the technical passport).

- Columns 8 to 11 contain information on deficiencies and surpluses in quantitative and monetary terms.

- Between 12 and 23, columns show the result of deviation control and re-grading data.

- From 24 to 32 columns, the final shortcomings and surpluses of the audited materials are recorded.

The statement is signed by both participants of the audit, each of whom leaves with him a copy of the generated document.