An inventory inventory, a sample of which will be described later, is a primary document that reflects a specific situation. She is represented by the relevant facts of the state. The document is compiled according to the assessment of field residues that are identified in the process of rediscounting. Next, we consider in more detail how an inventory inventory of material assets is compiled.

general characteristics

An inventory inventory, the form of which is approved by law, is essentially the same document as an invoice, waybill, act, and so on. Like other paper, it may contain some deviations from the actual state. If we compare the reality of the reflection of information, it should be said that the inventory inventory has a lower coefficient of representativeness than the usual packing list. In order to correctly conduct a re-registration, it is necessary to know the property that is being checked. Qualitatively, such work cannot be performed by an accountant. This is due to the fact that the specified specialist has no idea about the mass of goods, the specifics of stock accounting. In this regard, when conducting an audit, employees who are incompetent in this matter, making a primary document, make mistakes. Inventory inventory - reporting form, legal act. It shows the amount of responsibility that the agent bears before the owner.

State fact

The company has a certain economic situation. This refers, in particular, to the state of the assets, which are reflected in the inventory. The fact of the state is information about the property that is registered in the original document. The core is a value expressed in natural units. From the moment that each of them is endowed with value expression, they move into a special economic layer. Values, therefore, reflect the characteristics of the inventory of the enterprise.

Document Role Specifics

Inventory inventory reflects the relations of legal strata. In particular, on the part of property law, legal possibilities are revealed that stipulate the use, disposal and possession of property. In this case, the primary document clearly separates the categories of values. In particular, property held in storage or at the disposal of a company should not be confused with that which is property.

This provision predetermines the legal aspect that discloses the content of paid and unpaid stocks. At the end, the inventory is administrative in nature. It reflects the fulfillment of obligations by the responsible person to the owners and the manager.

Inventory inventory reflects the time layer of the fact of the state. In particular, it helps to identify stale products and products with normal sales periods. However, the real value of the fact of the state is established in the information aspect of the document. The larger the deviation indicator, identified as a counterbalance to the estimated value based on the results of the rediscounting (as a rule, this is done according to the comparison sheet), the more informative the fact.

Categories Used

The inventory list includes the characteristics of the values available at the enterprise. In their capacity is everything that should and can be the subject of compilation of the primary document. Recounting is carried out by removing field residues.It is a remeasurement, recounting, outweighing and taxation (multiplying the number of goods by the value of their units).

Inventory inventory: INV-3 form, general information on compilation

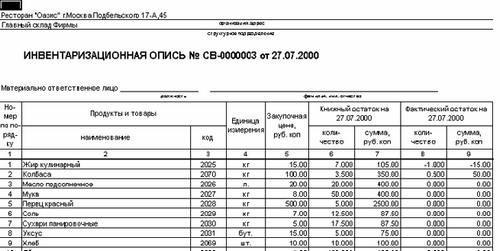

At the top of the original document contains a receipt. It is taken from all employees who are responsible for performing the inventory. Each specific name is entered in the document indicating the quantity, article, group, type and other necessary data. By weighing, measuring, recalculating, the actual availability of values is determined.

The preparation of the document is carried out in two copies. Both of them are signed by members of the inventory commission and materially responsible employees. One of the copies is sent to accounting. There is compiled collation statement. The head of the warehouse retains another copy. If expired, unusable, defective or damaged, as well as finished, but not previously considered products, are found, the act of writing off or inclusion in the statement (for finished products) is filled out.

Features of filling

If the inventory is compiled automatically, then entering information into the first nine columns is not necessary. The document is already issued with filled lines. Inclusion of non-reflected materials and equipment in the inventory is done on site. In this case, an appropriate protocol should be drawn up and an assessment made.

Important point

One of the necessary conditions when filling out the inventory is the inclusion in the document of the exact numbers of all equipment available at the enterprise. In addition, it is mandatory to include in the statement a description of its technical condition. No numbering errors should be made. After the inventory is carried out and inventories are compiled for all departments of the enterprise, the data obtained are summarized in a common statement.