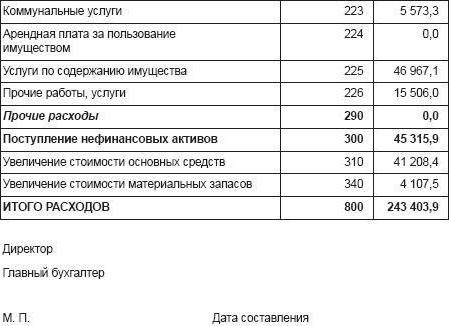

Cost estimate - a summary plan of all costs of a business entity for the future period of production and (or) financial activities. Using this document, the total amount of production costs is determined in terms of subspecies of resources, stages of production, levels of management at the enterprise and other expenses.

Definition

The cost estimate includes the costs of both the main and auxiliary production which are associated with the manufacture and subsequent sale of goods, products. This document includes the costs associated with the maintenance of administrative personnel, the implementation of certain works and services, which do not include basic production costs.

Cost Estimation

Cost planning is carried out in monetary terms for the production programs provided for in the projects for the year, with specific goals and objectives, selected economic resources and technological means of their implementation. Cost estimates in the context of planned targets and indicators should be specified. In other words, it is an estimate of costs in monetary terms, framed in the form of relevant results.

A sample cost estimate looks like a plan of projected costs in the context of work performed with applicable resources. For example, the estimated income for the future establishes the planned cash inflows with the corresponding expenses for the same period. The estimated cost of production shows the planned levels of stocks, volumes of production, as well as the cost of certain types of resources. The final estimate (code) should show the total costs in comparison with the results in the context of the main sections of the plan for socio-economic development for the coming year.

Estimation Methods

In the process of forming this document in production within the framework of Russian science and practice, the following methods are quite widely used:

- estimated, based on the calculation of costs within the enterprise according to the source data of other sections of this document;

- consolidated, based on the summation of the estimates of the production processes of some workshops (with the exception of internal turnover);

- costing, based on planned calculations for the nomenclature of finished products with the expansion of general items into simple costs or their elements.

Estimated Method

This is the most common method in domestic enterprises. Its use makes it possible to ensure coordination with bringing into the general settlement system in the form of a comprehensive planning document. The organization’s cost estimate using this method provides for the accumulation of all production costs for specific elements within the special sections of the annual plan. Estimated costs are determined in the following order:

- The costs of basic materials, components and semi-finished products are determined on the basis of the planned annual demand for material resources. In this case, the estimate should include only those costs that during the planning period can be expended with subsequent write-off in production. In other words, the need for material assets is accepted without taking into account any changes in stock balances.

- The formation of expenses for auxiliary materials is carried out on the basis of plans for their need for a year.The structure of these costs is the value of the tools, as well as household equipment spent in the planning period.

- Fuel in terms of value in the estimate should be planned in relation to its needs.

Summary method

To understand how to make an estimate of costs using this method, it is necessary to first develop and reduce the total costs in the context of the workshops of both the main and the service industries.

Costing method

This method of budgeting provides for the development of a production planning document based on calculations or costing of all types of products that are planned in the annual production program at the enterprise, as well as future expenses and work in progress balances. On the basis of the cost price of some products in accordance with the annual production volumes, a specific chess sheet is developed that contains economic elements and costing.

As soon as the chess table is formed, a general revised (consolidated) cost estimate is developed, which is planned for the future period. To form the cost of production from the consolidated estimates, it is necessary to exclude the costs of work that are not related to production.

Other costing methods

In addition to the methods discussed in this article, attention must be paid to methods such as process and custom costing.

In addition to the methods discussed in this article, attention must be paid to methods such as process and custom costing.

So, the process-based method of forming estimates provides for the planning of production costs in the context of individual structural units, production processes. General expenses are summed up under certain items of expenses, including the cost of labor and material resources.

A custom method of forming an estimate of expenditures provides for the determination of costs for the production of finished products in the context of individual orders, work performed and planned contracts. For each individual order, its own costing should be compiled, which displays both direct and overhead costs that relate to this type of work carried out in the production process.

Conclusion

Summing up the material presented, it should be noted that the estimate is a financial plan that determines the volume, distribution of appropriations within the specific allocated funds for the maintenance of the enterprise. The legal value of the cost estimate is to determine the rights and obligations of enterprise managers in the intended use of funds that were laid down in the preparation of this document.