As you know, each company carries out its activities for profit. Only when this goal is achieved can a firm ensure the stability of its work and the basis for expansion. The company's profit is expressed in the form of dividends on invested funds. The profitability of the company attracts investors, contributes to an increase in its capital. One of the most important aspects of the activity is the breakeven concept. It is considered the first step towards accounting, and then economic profit. Let’s further consider what the break-even point is.

Theoretical aspect

In economic science, the break-even point is understood as the normal state of the company in a modern competitive market, which is characterized by a long-term equilibrium. At the same time, economic revenue is taken into account - income at which the firm’s costs include the average market rate of return on invested funds. Normal company earnings are also taken into account. Under these assumptions, the break-even point definition is as follows:

- This is the volume of sales of goods at which profit from sales fully covers the costs of its production, including the average market interest on own assets and entrepreneurial (normal) income.

Performance

If the company receives accounting profit (the balance of its income from sales and cash costs for the release of goods is positive), the breakeven point may not be reached economically. For example, revenue may be lower than the average market interest on capital. It follows that there are other, more profitable options for using your own assets that would allow you to get more income. The breakeven point of the enterprise, therefore, acts as a criterion for evaluating the effectiveness of entrepreneurial activity. A company that does not reach it does not work well in the prevailing market conditions. But this fact, of course, cannot be considered an unambiguous reason for the company to exit the business. To resolve the issue of termination of the company, it is necessary to study the cost structure in detail.

Revenue maximization

It is necessary for the optimal functioning of the company. The process of maximization is the calculation of the breakeven point in economic terms. In the study of this procedure, the following concepts are used:

- Marginal revenue. It represents the amount by which the total profit of the company changes with an increase in the output of goods by 1 unit.

- Marginal cost. They express the amount by which total costs change with an increase in production by 1.

- Total average costs are the sum of fixed, variable and sunk costs per unit of output.

From a certain moment (when a certain volume of output of goods is established), the curve of variable costs will increase, and the marginal income, respectively, decrease. To maximize profits, the fundamental relationship is between profit and costs with an increase in output by 1. It is clear that when marginal costs are less than income, with an increase in the quantity of goods, profit becomes larger. If costs are more than revenue, then a decrease in output will contribute to an increase in income. Thus, we can formulate a criterion under which the profit will be maximum: it is achieved when the marginal indicators of revenue and costs are equal.

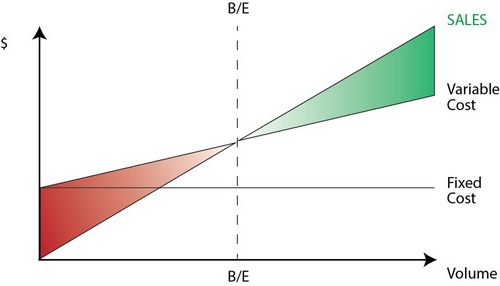

Break-even point: how to calculate?

There are several points that you need to pay special attention to. First of all, the problem is to establish a critical volume of goods at which the breakeven point of production is reached. There are three approaches to solving this problem:

- The equation.

- Establishment of marginal income.

- Graphic image.

Of particular importance will be the analysis of the breakeven point (forecasting) for changes in assumptions.

The equation

This breakeven point method involves the following scheme:

- Income - Variable expenses - Fixed costs = Net profit.

The last indicator can be designated as P. P is the selling price of a unit of goods released, x is the volume of manufactured and marketed products for the period, and fixed and b are variable costs. Using these notation, you can make the following equation:

- P = P * x - (a + b * x), or P = (P - b) * x - a.

The last equality indicates that all factors are divided into criteria that depend and do not depend on the volume of sales. In the process of determining the parameters, the costs were divided into sold and manufactured products. This difference is considered the most significant in two approaches to management accounting: Direct costing and Absorption costing. In the latter case, the costing is performed with the distribution of all costs between the goods sold and its balance. In other words, fixed costs are stock intensive. When using the second method fixed costs relate fully to implementation. According to the first equation, you can easily calculate the breakeven point. To do this, carry out simple mathematical transformations. From the condition П = 0, the volume of production of goods is established at which the break-even point is reached in the company. The formula is as follows:

- x0 = (P + a): (P - c) = a: (P - c).

Example

Consider a hypothetical company that produces electronic components. The cost of one unit of goods is 5 thousand dollars, variable costs (the price of components, staff salaries and so on) for 1 product - 4 thousand dollars, fixed costs - 20 thousand dollars. We find the maximum volume of production at which the company break-even point. The formula would be:

- ho = 20,000: (5000 - 4000) = 20 (units of production).

The time for which the found quantity should be released and sold will correspond to the period for which the value of fixed costs will be found. Using the equation in the previous paragraph, you can determine the size of the volume of output that should be achieved to obtain a specific amount of profit at which the break-even point will be reached. How to calculate the company's income, for example, at 10 thousand dollars? To do this, release:

- x = (10,000 + 20,000): (5000 - 4000) = 30 (units).

Profit margin

This method is considered a modified version of the previous method. Marginal profit will be considered the income that the company will receive when releasing one product. Using an example, we find it:

5000 - 4000 = 1000 per unit.

To more accurately represent the area of relevance, we should list the assumptions that are used in the construction of the described models.

General expenses and revenue

The behavior of these indicators is linear within the scope of relevance and is rigidly defined. This provision is true only when the change in output is small in comparison with market capacity of this product. Otherwise, the linearity of the dependence of output indicators and revenue will be violated.

Expenses

All costs can be divided into fixed and variable. The former are independent of output within the scope of relevance. This assumption greatly facilitates the analysis. However, along with this, it significantly limits the scope of relevance.Indeed, under this assumption, the volume is limited by the available fixed assets. However, it is impossible to increase or rent them. More realistic is the assumption that fixed costs change in stages. But it greatly complicates the analysis, since the schedule of total costs becomes discontinuous. Variable costs remain independent of output as part of relevance. In fact, their value is presented as a function of production volume, since there is the effect of a drop in the maximum productivity of factors. In this regard, under the assumption of independence of fixed costs from the volume of output, variable costs increase with its growth.

Selling price

The assumption that it also remains unchanged is considered the most vulnerable point. This is due to the fact that the selling price depends not only directly on the work of the company, but also on the structure of market demand, the activities of competitors, and so on. The costs of the enterprise for the promotion of its products, the formation of its distribution network and much more also have a significant impact on the change in the indicator. Here, therefore, it is necessary to investigate many factors influencing the subsequent assessment. But such an analysis is quite complicated and requires an individual approach in a particular situation.

Other assumptions

The assumption that the services and materials used in production remain unchanged is also highly controversial. However, it greatly facilitates the assessment. The following assumptions also apply:

- Performance does not change.

- There are no shifts in the structure. On this assumption, it makes sense to dwell in more detail. Above we considered the release of one unit of goods. Accordingly, there were no problems in allocating costs for different products, setting their prices, or determining the effectiveness of a particular production structure. In conditions of variability, the assessment requires the use of additional criteria. The breakeven point of sales is precisely set only with a specific structure of the release of goods.

- Only the quantity of manufactured goods has a relevant effect on costs. This assumption is of particular importance for analysis. In this case, we should ignore the influence of external factors and include in fixed costs all costs that are not dependent on the quantity of products.

- Production and sales volumes are equal or changes in initial and final stocks are insignificant.

Sensitivity Rating

The above assumptions are of little use in the real world. However, they can be adapted to reality through sensitivity analysis. This method involves the use of the "what will happen if ...". Within its framework, one can get an answer to the question of how the outcome will change if the initially designed assumptions are not achieved or the situation with them changes. The security margin acts as a tool in this analysis. It represents the amount of revenue that is at a level lower than the breakeven point. This amount shows the limit to which income can decrease so that there is no minus. After making basic assumptions regarding changes in the initial assumptions, it is necessary to establish the corrections of the security margin and marginal income caused by them. In management accounting, a continuous assessment of cost behavior is carried out and break-even point is periodically identified. At its core, sensitivity generates margin elasticity with respect to tolerances.

Cost and price estimates for future periods

The operating company takes these indicators from its own statistics and the behavior of the cost of production, taking into account the expected changes in the economy. In particular, seasonal fluctuations, the activities of competitors, the emergence of substitute products (especially in high-tech markets) should be taken into account. New companies cannot rely on their experience because it is absent. Thus, for them, the calculation will be relevant by analogy with already existing firms in this industry. Along with this, you can use a variety of background information. The most difficult thing is to create a company that will operate in a non-existent sector. In this case, a thorough costing, marketing research should be carried out. For such firms, it is advisable to use cost-plus pricing. The price in this case is obtained by adding a fixed margin to the amount of costs. In this embodiment, the size of the marginal income is known, therefore, the breakeven point is easily found.

Conclusion

Considering methods of establishing a breakeven point, it is thus assumed that the costs of producing a unit of product and the selling price act as external factors. In other words, by the time the required indicator is found, these values are known and cannot be changed. The establishment of these key parameters, their in-depth analysis allows, in turn, to explore the break-even planning of the company.