After countries underwent the global financial crisis, a fairly large number of various changes in the financial sphere occurred. In the current crisis, problems such as a risk management system have become one of the most important. In particular, this applies to the economic activities of financial institutions, as well as their various counterparties, which have become especially relevant today.

Why is it important?

One of the main reasons why financial institutions have undergone a crisis, advanced economists say that most companies have underestimated the importance of the risk management system associated with the use of new financial instruments. Thus, we can say that earlier risk management was not as relevant as it is today. In Russia, the crisis affected most of all precisely those banks in which the risk management system was poorly developed, since there was no opportunity to influence the adoption of any tactical or strategic decisions, while specialists working in business units did not could realize the completeness of the risks of the decisions they make. The role of those departments that were involved in risk assessment was to evaluate the decisions already made and subsequently generate a report.

The crisis affected least of all those banks that built a competent risk management system and which for more than a decade have been collecting, processing, analyzing information and then evaluating risks. It is such banks that consider risk management as the main strategic principle, as well as a source of their own competitive advantage long before the tipping point. Thus, in the current conditions, the priority in commercial banks is often given to the so-called risk management.

What is included here?

In the context of the developing financial crisis, the enterprise risk management system is becoming more and more relevant, which provides for an operational assessment of the state of companies that are in the loan portfolio. At the same time, an objective approach is also important in order to work out the most optimal conditions for the transaction and informed decision-making on the issue or taking of a loan. The solution to this problem is simply impossible if a competently constructed risk management system is not used at the enterprise.

What is she like?

Today, such systems exist in a different form in almost every financial or even non-financial institution, but in the vast majority of cases they are just a formality, as a result of which they are absolutely ineffective. When the company does not have a properly built risk management system in customs and other business matters, this ultimately becomes the reason for its inefficient work and subsequent bankruptcy.

The rather high probability of changes in the current financial market of Russia necessitates the construction of a truly effective risk management system, which should have analytical, organizational, operational and, of course, computer support.

For example, in domestic banks the role played by a competent management system is often underestimated. risks (risk management). The task of organizing a truly competent system is far from the first among the existing areas of development, and this is due to the fact that domestic specialists often simply do not have enough practical and methodological experience in this area, because such issues began to be addressed only in the early 90s of the last century .

How to build a competent system?

The use of international methods and standards allows for the significant development of risk management, turning it into a truly effective tool that provides an opportunity to really assess all the risks that a company has and assumes.

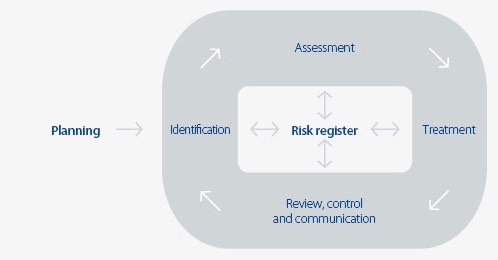

Risk management system in customs or any other issues should solve several basic problems:

- Determine the rating of the company, which is taken or which will be granted credit, and whether there will be a probability of default when making certain decisions.

- To substantiate the decisions made.

- Improve the quality of the loan portfolio.

- To form the possibility of providing continuous control over the state of the loan portfolio.

- Reduce the proportion of problematic solutions.

- To increase the efficiency of the organization of work, as well as minimize time costs due to automation and standardization.

- To create opportunities in order to constantly monitor and, if necessary, timely respond to problems that may arise with customers.

Credit risk management system

If we are talking about the banking sector, then in this case there are several main blocks, which includes a risk management system (risk management).

Loan Portfolio Assessment

The management bodies of the bank, as well as any other financial structure, must carry out an assessment of the loan portfolio, and do this constantly. Thus, it will be possible to improve the existing risk management system, which will correspond to the current scale of the company’s activities, as well as strategic plans.

The assessment of the risk management system of the bank’s loan portfolio is based on the credit risk of each individual category of borrowers, as well as the distribution of loans for all these categories. The basis of grouping the loan portfolio depending on the degree of risk today is the basic requirements that are established by Regulation No. 254-P of the Central Bank. In accordance with it, the loan portfolio may contain loans of five risk groups:

- Doubtful.

- Distressed.

- Hopeless.

- Standard.

- Non-standard.

Based on the results of the assessment, as well as analysis of the loan portfolio, the bank is already developing the new credit policy. If necessary, adjustments can be made to an existing system.

Credit Risk Forecasting

Modern banks that carry out lending activities, in the course of their work should not only ensure the implementation of a risk management system, but also predict them. Today, from this point of view, the most important problem is that modern banks do not have effective tools for predicting the level of risk of the loan portfolio. This problem is especially acute in difficult economic conditions, when the audit is carried out in accordance with international financial reporting standards, and managers try to reduce the level of general risk to global average. The most optimal solution to this problem will be the use of qualitatively new approaches to forecasting - electronic computing equipment, as well as economic and mathematical methods.

Thus, the objectives of the risk management system will include the ability to plan the structure of the loan portfolio, which is extremely important when it comes to liquidity of a banking institution.

Determination of the maximum possible level of credit risk

The maximum possible level of credit risk for a bank should initially be recorded in the credit policy of this institution. In this case, its value will directly depend on what kind of strategy the bank follows in the field of risk management. In the process of work, it will be possible to revise this indicator depending on the current financial situation of the bank, the current economic situation in the country, as well as the external economic situation.

Building an optimal loan portfolio structure

The optimal structure will directly depend on which maximum risk level has been chosen. This structure will be formed on the basis of a credit risk optimization model.

Direct loss risk assessment

The economic risk management system is assessed by the quantitative and qualitative probability of occurrence of events that may lead the company to losses, while predicting potential losses in advance. It is also quite simple to estimate the direct, that is, the measured losses, which are quantified. Such risks are characterized by the following:

- Reduction or complete loss of the value of assets due to theft, fraud, any losses, as well as failures and all kinds of operational errors.

- Losses that are the result of errors in the payment details, as well as write-offs or in relation to incorrect counterparties, which ultimately failed to be returned.

- Losses on compensation to customers of their payments.

- Losses due to various legal circumstances that are directly related to litigation or all kinds of legal errors in signed documents.

- Loss of tangible assets due to certain circumstances, which may be a fire, theft and much more.

- Penalties prescribed by regulatory and control authorities as a result of violation of certain regulatory acts.

- Penalties under the instructions of the tax authorities and other losses that result from improper adjustment of own tax payments, as well as violations of established tax accounting rules due to various operational errors.

Risk assessment

The risk management system in the organization is also quantified, that is, when the possible future of the company is predicted. The calculation relies in this case on various statistical methods, and the value directly depends on what level the accepted confidence probability is at. As a quantitative assessment of the risk management system there are several basic statistical parameters:

- Assessment of the probability of an adverse event occurring at a particular risk object due to the fact that a specific source was implemented.

- A statistical assessment of the result of an adverse event, as a statistical assessment of the magnitude of possible losses, depending on their type, which may appear at a given risk object.

- A statistical assessment of the occurrence of possible deviations with a certain level of confidence probability from the assessment of possible losses.

Probabilistic-statistical technologies are used to determine the sources of operational risk that are in the nature of queuing elements.Among these, one can distinguish: the occurrence of technological failures or the failure of electronic equipment, errors on the part of the operators in the process of servicing a large number of applications from customers, and much more.

Difficulty or inability to quantify

Operational risks can by no means always have a clearly defined quantitative assessment. For example, due to an imperfect technology for passing documentation or not too good qualifications, a bank employee will have to spend much more time in order to service the operation on the part of the client. The fact that the bank ultimately will incur losses from the most inefficient use of the resources it has is obvious to everyone, but in fact, these losses are not so easy to express in value terms.

In such a situation, the bank will have to conduct an indirect assessment, that is, calculate the so-called unmeasured losses. Such a risk management system in an organization is not found so often in the form in which it should be, but in fact it is necessary in many companies. Such a system of losses is calculated from sources or objects of operational risk, in the case of which it is not possible to unambiguously determine a certain number that can characterize the probable level of losses.

In particular, such losses may occur due to:

- Reducing the quality of services or the services provided, which inevitably leads to a reduction in the customer base.

- Shortfall in revenue.

- Loss of quality of ongoing banking processes, which provokes the need for the allocation of additional funds.

- Loss of reputation, which also ultimately leads to a loss of customer base.

- Stoppage of the company due to various adverse events. For example, a technological malfunction of some important equipment can pass this event.

How is the assessment carried out in this case?

Qualitative assessment in this case is carried out expertly. In order to ensure the effective application of the risk management system, in this case, it will be necessary to determine the criteria and risk factors that will be relevant to indicate in a specialized table, which contains a rating scale.

It is quite useful to use qualitative assessments in order to identify areas of increased risk, as well as to understand how well the procedures for performing certain operations correspond to the established practice.

Improving the risk management system led to the fact that the Basel Committee also proposed to assess the conditional losses, that is, losses that the company could have incurred in the course of its work, but which it could avoid due to the emergence of certain favorable circumstances.

What could be the loss?

Losses from operational risks in this case are divided into two main categories:

- Small ones that occur quite often and are expected or average.

- Large, which occur less frequently, as a result of which in the overwhelming majority of cases are unforeseen.

It is often possible to predict average losses based on the personal experience of the company, so the development of a risk management system inevitably involves replenishing it with such forecasts. In order to determine such losses, it is necessary to initially conduct a thorough analytical accounting of expenses that were caused by operational risks in certain categories.

Unforeseen losses cannot be estimated based on the standard average statistics of your company.

In order to conduct a full risk assessment, the bank may use some technologies that it developed independently, based on the vulnerability to potential operational risks.Such a process is predominantly internal, and often contains various checklists and workshops that identify weaknesses and strengths of the operational risk sphere.

However, in the overwhelming majority of companies today, technologies for measuring operational risks are only at an early stage of development even in the basic elements of a business, not to mention how the customs risk management system or other more subtle issues look like. Most foreign banks use specialized formalized measurement technology, while the rest are only on their way in this direction. It’s worthwhile to understand that the methods used today are relatively simple and mainly represent experimental structures, although a well-developed risk management system is often found, for example, Customs in which carefully examined and studied during the interaction. Often such systems are backed up with appropriate software.

RAROC

RAROC technology, which today is actively used by the most advanced banks operating in the international market, has become quite widespread. Such a system is used in calculating the level of return on investment, and provides for taking into account the amount of risk by changing the profitability itself, and not the amount of capital investment that the company provides in the process of its work.

It is worth noting that in domestic banks the ARIS system is actively used, with the help of which not only existing business processes are described, but in addition to this, it is also possible to use classifiers of various operational risks with further calculation of losses for each individual risk category.