Summarized accounting of working hours is a fairly common mode of operation of modern companies. But at the same time, many leaders may not even know how to draw up this norm correctly.

What it is?

There are different types of working hours, but in this case, a specialized mode is considered, which is based on shift schedules, including also rolling weekends.

The basis for the introduction of such a regime is the specific conditions of production in the company or in the process of performing certain works that do not provide the opportunity to comply with the specific working hours established initially for this category of employees. Such specific conditions of production, which may serve as a reason for using the summarized accounting, can be called the general seasonality of the company or the similar nature of the work performed.

How is it administered?

The order in which the types of working hours are changed is determined in accordance with the current internal labor regulations, but these rules themselves must be approved by employers, taking into account the views of the representative bodies of employees or if a collective agreement is signed.

The following information must be specified in these rules:

- The fact that the working hours are changing and this mode is introduced.

- The duration of the accounting period.

In the event that a new employee is hired and his duties are fulfilled in accordance with the rules of summarized accounting, he must also be aware of these rules and must sign in a specific document that he really was introduced. If this mode is not introduced for the whole company, but only for a certain category of employees or even for various types of work, then in this case the working mode for these employees becomes individual, and at the same time, a prerequisite for the drawn up employment contract. The most common wording in this case is as follows:

- For the employee, a normal schedule of working hours is determined, based on 50 hours weekly with a cumulative accounting.

The decision that a certain part of the employees is transferred to summarized accounting also provides for a change in certain conditions of the drawn up contract.

Graphs

The main feature of this regime is that the calculation of working time from day-to-day or weekly provides for certain deviations of the duration of work from the originally established standards for this category of employees. Moreover, within the boundaries of a specific period, the total duration should not exceed the normal number of working hours established for this period.

In this regard, the implementation of the standard labor standards that is, working out the time standard is provided not over a week, but over a longer period. AT employer responsibilities the organization of work is included so that the employee, for whom a different calculation of working time with summed up accounting is now used, ultimately fully worked out his own norm during the accounting period.It is for this purpose that an individual shift / work schedule for a specific period is developed, and the time of the beginning and end of the working day, the rest time between shifts, and also their duration are initially set in accounting.

At the same time, one must correctly understand that the total duration of work on such a schedule cannot exceed the norm of working time that is determined for this accounting period. At the same time, a defect to the noted norm is also not allowed.

Among other things, in the process of scheduling a shift, do not forget that it is forbidden to conduct work for two shifts in a row, and the shift schedule must be approved by the head of the company or the person authorized by him, taking into account the opinion of a certain trade union body of the company (if if any), and then it is brought to the attention of the workers, which should be done no later than a month before it takes effect.

Norm

If summarized accounting of employee’s working hours is used, then in this case, for a certain established period, the norm of time established by each employee should be distributed. Moreover, in different months or weeks, an employee can perform a different number of hours (overtime on one day, part-time on the other).

The introduction of a long accounting period is advisable for the reason that in this case, overtime is minimized and, for example, seasonal overload of employees is smoothed out. At the same time, if the company does not have a shift schedule or certain employees work for two or even more shifts in a row, all these actions by the labor inspectorate will qualify as administrative offenses, and responsibility for this is already provided for by the relevant code.

How to determine the accounting period?

For example, in accordance with the current PVTR (internal labor regulations), a normal working day is:

- Mon-Fri: 08:00 - 16:00;

- Sat: 08:00 - 14:00;

- Sun: day off.

In other words, the total working week is 40 hours.

Due to the fact that the duration of work is determined in accordance with a five-day working week, employees who perform their duties under the described regime actually work out per month:

- in July - 172 hours;

- in August - 181 hours;

- in September - 174 hours;

- in October - 172 hours;

- etc.

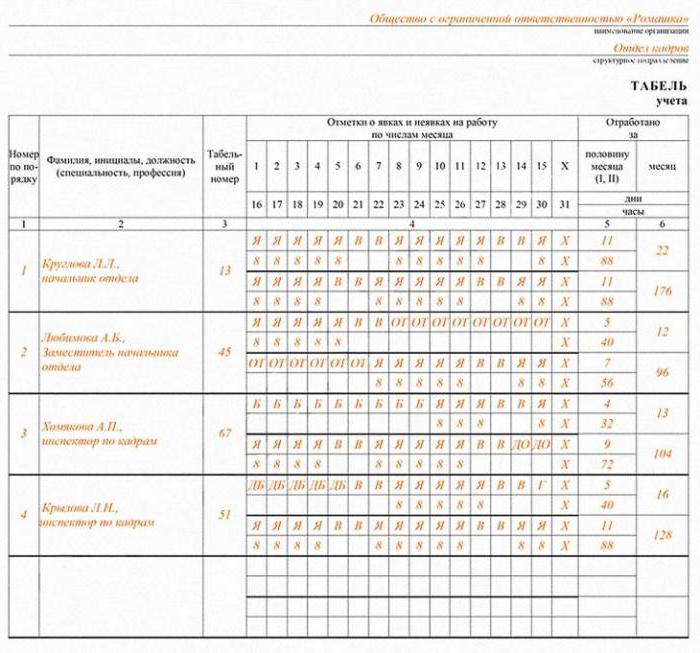

You can see a sample of time tracking above.

What do you need to know?

First of all, it is necessary to figure out whether in this case we are obliged to keep a summarized record for employees with this mode of work if the marked working week is respected, or if we need to introduce a weekly record. If this is permissible, then in this case you need to figure out how to understand how the time sheet for these employees should be handed over so that they can normally pay for working hours, since a month can exceed or be less than the norm.

If, nevertheless, it is necessary to introduce summarized accounting, and at the same time consider the year as the accounting period, then in that case there will be approximately 16 overtime hours in one year. Due to this, the employer will observe the normal duration of work for a week, and at the same time, at the end of the year, he will have to pay his employees overtime hours. In this case, many are wondering if it is possible for the year to adjust the working time a little so that ultimately the established time norm is not violated, and therefore, it would not be necessary to pay extra overtime hours, and whether PVTR situations.

In general, the use of summarized accounting does not constitute an immediate obligation of the employer. But at the same time, one must correctly understand that certain regulatory legal acts provide for the introduction of this regime without fail for that category of workers who, for example, work on a rotational basis, as well as for drivers of vehicles and crew members of various vessels.

If the company does not have an obligation to use summarized accounting based on special regulatory acts, then in this case the possibility of introducing this regime is established if the production conditions as a whole do not make it possible to create a specific schedule for employees.

Important Features

If an employee does not fulfill the costs of working time set for him, then in this case the employee’s basic salary, namely his remuneration for labor, should be calculated in proportion to the time that he actually worked.

The peculiarity of summarized accounting in this case is that, in contrast to weekly or daily labor time accounting, it provides for certain deviations from what is initially set for this category of workers. Moreover, if there is some kind of processing on certain days or weeks, it can be compensated for by shortages during other weeks or days in such a way that, ultimately, within a certain accounting period, the total duration would not be more than the normal number of working hours. In this regard, the normalized number of hours is worked out not within a week, but over a longer period.

It is worth noting that at the moment there is a specific procedure for calculating the working time standard, in accordance with which the duration of hours is established, which must be worked out by different categories of employees during the week, month or other time period. That is why the number of hours worked must comply with the norm that is established by this Procedure. In this case, it is possible by any means to vary the duration of the work throughout the accounting period, but the most important thing is to balance it within the general framework.

The uniform procedure for determining the standard of how hours of work are set, equalizes the situation of workers with normal working hours with those who work on the summarized report of working hours, and ultimately ensures full equality of rights for employees.

Working out the total number of working days should be provided by the employer during a certain accounting period. If this employee does not comply with labor standards due to the fault of the employer, and he has less work hours in the year, then he must pay him a salary for the time actually worked or the work done, but the pay should not be lower than the average wage employee fees calculated for a given time period.

Basic concepts

The normal working hours in accordance with current practice is 40 hours per week. At the same time, if, according to the production conditions, the company cannot observe the daily or weekly duration established for a specific category of employees, it is possible to introduce such a rule as summarized accounting of working hours.

Its use in practice in most cases raises a rather large number of questions. Initially, you need to correctly understand how to establish the procedure for determining and paying for overtime hours, as well as how to properly document them.In addition, the summarized recording of working time causes a rather large number of disputes in terms of regulatory acts of employers, which quite often enter such provisions that cross-over the current legislation. It is for this reason that it is necessary to correctly understand the basic provisions and subtleties of the design of this mode.

The introduction of such accounting

Quite often, such situations occur when a company hires a certain employee, and as a result, the employer decides to introduce a summarized record of working time. In this case, it is necessary to use as the basis of Article 7274 of the Labor Code of the Russian Federation on the introduction of various changes to the composition of the employment contract.

In this case, one of the most important conditions is that changes to the employment contract must be made with prior notification of this to employees no more than two months before these corrections enter into force. At the same time, employers are far from always aware of the consequences of non-compliance with established standards. For this reason, it is worth considering several examples of court decisions on such issues so that employers are cautioned against violating applicable laws.

Example

It is known that a woman worked at a certain substation of medical care in the MUSIC. In accordance with the original employment contract, a reduced work schedule was specified, i.e. normalized working day in accordance with a specific shift schedule, as well as components of working time. Moreover, in accordance with the PTRA of this institution, for all employees who work with various medical care, monthly work hours are used based on 68 hours of work during the day, as well as a five-day work week.

In accordance with a subsequent order of the head physician of this institution, the standard for working hours for the next year is approved, and at the same time, a shorter working day is provided, providing days off according to a rolling schedule. In the same way, amendments are made to other rules of the contract, as a result of which the year, and not the month, is already considered as the accounting period.

Since the woman was not notified in writing of this in a timely manner, the court ultimately arrives at the justified conclusion that she is in arrears of arrears in payment for all overtime hours that she worked during the year. In addition, in accordance with applicable law, the plaintiff is also charged with compensation for the fact that the employer delayed the payment of wages.

In certain situations, the amounts that are collected from the employer are quite small, and by and large it is a pity to waste time, but there are also situations in which employees are awarded quite impressive amounts that could really be excluded if the employer acted in accordance with laws and regulations.

How to keep records?

When a time sheet is written, many people often have various disputes over how to properly calculate hours worked. After all, far from always employees of the company understand the features of summarized accounting, as a result of which they will not assert their rights in court. If the employer complies with the current legislation to the full, then the decision of any court will ultimately be recognized in his favor, and that is why it is best to understand these subtleties in advance, and then not return to them.

Defective payment

There are also situations when questions arise about securing an additional payment in the event that the employee did not work the required number of hours during the accounting period.If they were not worked out solely through the fault of the employee, then in this case this does not cause any disputes, but the situation is different if such working out should be carried out through the fault of the employer.

What do you need to remember?

- If you want to compile a summarized time sheet, you need to be based solely on the norms of Chapter 12 of the Labor Code of the Russian Federation. When properly observed, the risk of someone else being able to and even willing to challenge the actions of the employer is substantially reduced.

- In the process of calculating working hours for a certain employee, periods when the employee was not at the workplace, but at the same time his workplace was kept, should be excluded. The list of such time includes the time of holidays, sick leave and many other situations. Already based on these numbers, the total number of overtime hours should be determined.

- In order to pay for unfinished hours, you first need to figure out why a person worked part-time. If this situation occurred due to an employee’s fault, then unearned hours should not be paid, but if the employer is to blame, then unearned hours should be fully paid in the amount of 2/3 of the established salary (downtime) ), as well as in the amount not lower than the salary, if subsequently the employer did not provide his employees with the opportunity to work this time.

- Hours that an employee works beyond the norm must be paid for in accordance with the rules of Article 152 of the Labor Code of the Russian Federation. Overtime hours are calculated at the end of the accounting period, and at the same time they directly depend on the norm that must be worked out by the employee during this period. It should be noted that the first two hours should be paid in the amount of 1.5 from the norm, and the rest - in double.

- In a slightly different way, overtime work is carried out for railway employees. The duration of hours that have been worked overtime, and at the same time must be paid in one and a half times, should be determined by multiplying two hours by the total number of days that are working for a particular reporting period as a whole. After that, hours are calculated from the amount of overtime during the accounting period, which must be paid in the amount of one and a half standard payments. The resulting difference will be those overtime hours that will be paid twice as much as the standard salary. But in fact, this method of conducting calculations causes a lot of controversy, so it is better for legislators to get additional clarifications.

Given all these concepts, you will be able to determine the required duration of work, as well as be able to more competently manage the work of your employees in order to ultimately avoid any violations of applicable law and, accordingly, all kinds of litigation.

Competent specialists, however, always understand how to properly use this mode of work and what advantages it provides to the employer, and therefore actively use it if necessary.