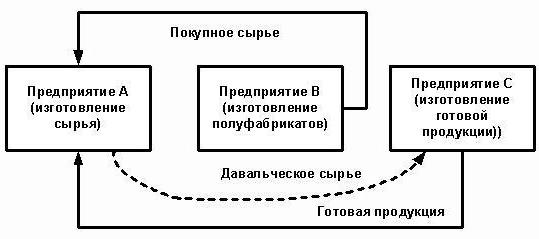

Subcontracting is an accounting term. Its essence is that the contractor takes custody of the customer’s materials and undertakes to produce products from them and receive payment. Consider in more detail how the accounting of tolling at the enterprise takes place.

Legislative regulation

The organization that commissions the manufacture of goods from raw materials supplied by the customer acts as the customer, and the manufacturer as the contractor. These transactions are governed by Art. 713, 714 of the Civil Code of the Russian Federation. The regulatory act says that work is performed from the materials of the contractor, his forces and equipment. If the customer instructs to make products from their own raw materials, then such transactions will be governed by the general rules described in Sec. 37.

The contractor is obliged to use the material economically, and at the end of the work, submit a report, return the rest of the raw materials or reduce the cost of the work at its cost. If, as a result of the activity, finished products with defects that make it unsuitable for further use were released, and the reasons for their occurrence are associated with the provision of low-quality material, the contractor may require payment for previously performed work.

Art. 714 provides for the responsibility of the contractor for the failure to preserve the materials provided and other property. The procedure for calculating the price of works from tolling materials is described in Art. 709, 711, 720. From the above norms in the Civil Code, one can distinguish the following characteristics of operations:

- customer-supplied materials, as well as products made from them, are the property of the customer;

- the contractor is responsible for the raw materials from the moment they are received, during the manufacturing process and until the release of the goods;

- the cost of the transferred raw materials is not included in the price of the contract.

Tax nuances

In operations with the manufacture of products from tolling, there is no transfer of ownership of the products. Therefore, for tax purposes, such transactions are classified as work. In Art. 38 of the Tax Code of the Russian Federation there is an explanation of such operations: work is an activity that has tangible results that can be used to meet the needs of the organization. An acceptance certificate is issued for the products. The transfer of raw materials by the customer for processing, as well as the receipt of goods, is carried out without transferring ownership of them. Therefore, such transactions are not subject to VAT and NPP (income tax).

Subcontracting: Documents

All the nuances of the operation should be prescribed in the contract. In particular:

- the exact name and description of the materials transferred, their quantity, quality and cost;

- the procedure for the transfer of materials and acceptance of the processed product;

- raw material consumption rate;

- terms of payment;

- the presence of technological losses (waste), the procedure for their accounting;

- other conditions.

Irrevocable production waste is equal to material costs. All of them must be documented. The basis for their write-off is the consumption rate, which is indicated in the contract.

When materials are issued, an invoice is issued in the form of M-15. It indicates the raw materials that are transmitted on tolling terms. In the event of incorrect paperwork, the tax inspectorate may regard the transfer as gratuitous and charge additional VAT. After completing the work, the customer should receive from the contractor:

- report on consumed materials and waste;

- act of acceptance of work.

The organization independently develops forms of documents.The quantity of material used must correspond to the calculation. On the basis of the same document, the accounting records write-offs of raw materials.

Recording of operations by the contractor

Let us consider in more detail how the contractor displays transactions in 1C. Subcontracting raw materials are recorded in the balance on account 003 “Materials in processing” and 002 “Materials and materials for repository storage”. Analytical accounting is carried out on tolling facilities, names, quantity, storage and processing places. Raw materials that are transferred for processing are accounted for at the warehouse of the M-15 consignment note and a receipt order, which contains a note on tolling conditions.

Production costs are recorded by the contractor on account 20 “Production”. If the processor simultaneously produces his own products, he must keep separate records. Waste is displayed in the balance sheet as property received free of charge. They are part of non-operating income (Article 250 of the Tax Code of the Russian Federation) after signing the acceptance and transfer of raw materials. They are displayed in the control unit at CT98 “Deferred income”, and then are debited to account 91 “Other income”. Since income in OU arises earlier than in OU, there is deferred tax asset.

Processor Postings

For greater clarity, the material of this block is placed in the table.

| Operation | DT | CT |

| Raw materials received | 003-1 | |

| Written off materials | 003-2 | 003-1 |

| Reflected production costs | 20 | 02 (70, 10) |

| Products accepted at the warehouse | 002 | 003-2 |

| Submitted work to the customer | 62 | 90-1 |

| Tax Reflected | 90-3 | 68 |

| Cost accounting | 90-2 | 20 |

| Transferred products | 002 | |

| Residues transferred | 003-1 | |

| Capitalized waste | 10 | 98 |

| Reflected it | 09 | 68 |

| Implementation (write-off) of balances | 98 | 91-1 |

| Repayment SHE | 68 | 09 |

| Reflected financial result | 90-9 | 99 |

| Tax Reflected | 99 | 68-4 |

Example

The construction company received from the customer subcontracting materials in the amount of 100 thousand rubles. and uses them to make goods. The agreed cost of work is 35.4 thousand rubles. (VAT 18% - 5.4 thousand rubles). Acceptance of raw materials is executed by order No. M-4 with a note on tolling conditions.

Accounting for operations in the processor by the processor

Let's look at the table again:

| DT | CT | Amount, thousand rubles | Operation |

| 003 | 100 | Reflected the cost of tolling | |

| 20 | 70-69 | 20 | Processing costs included |

| 62 | 90-1 | 35,4 | Reflected the cost of processing |

| 90-2 | 68-2 | 5,4 | Tax included |

| 90-2 | 20 | 20 | Write-off of expenses |

| 51 | 62 | 35,4 | Payment from the customer is considered |

| 003 | 100 | Write-off of the cost of materials during the transfer of goods to the customer |

The processing of transactions with the processor is carried out on account 003 without double entry. If waste occurs during processing, it will either be returned to the customer or retained by the contractor. In the second case, an entry is made according to КТ003 for the sum of the cost of materials with their acceptance for accounting on the main account “10”. Then the waste is written off at market prices: KT10-6 DT98-2.

Customer accounting

Finished products belong to the customer. In a report, he arrives at account 43, and also draws up an invoice in the form No. MX-18. The transferred raw materials are the property of the customer. Therefore, it displays such transactions in the sub-account 10-7. In the cost structure of goods, the cost of raw materials and processing works is taken into account. Additionally, transportation, travel expenses, intermediary services, overhead costs.

The processing agreement may stipulate the following payment options: money, materials, goods, combined forms of payment. If the service is paid in kind, the contract is mixed in nature, the dalts will have an obligation to remit the amount of VAT. If the contractor has the waste left, then the customer and the control unit must reflect the operation for the gratuitous transfer of values, which is equivalent to sales and is subject to VAT.

Subcontracting raw materials: postings in control unit at daltse

Let's look at the table:

| Operation | DT | CT |

| Transfer of materials to processing | 10-7 | 10-1 |

| Written off materials on GP | 20 | 10-7 |

| Refund Reflected | 10-1 | |

| Processing cost accounting | 20 | 60 |

| VAT Reflected | 19 | |

| Accepted for tax deduction | 68 | 19 |

| Waste Included | 10-12 | 20 |

| Manufactured goods accepted | 43 | |

| Transferred goods to pay for the service | 62 | 90-1 |

| Accrued tax | 90-3 | 68 |

| VAT listed | 60 | 51 |

| Offset requirements | 62 |

Accounting in accounting is carried out depending on the nature of operations.

Refinement of materials

The customer transfers the raw materials in order to bring it to a state in which it can be used in production activities. The processor in this case returns to the contractor not products, but modified materials. Their customer comes to account 10 and increases their cost due to the cost of the contractor's work.

Example

A furniture factory bought wood worth 354 thousand rubles. (VAT 54 thousand rubles). After equipment failure, the factory signed an agreement with a woodworking company. The factory ordered the manufacture of boards, which then used to produce cabinets. For the work you need to pay 118 thousand rubles.

| DT | CT | Amount, thousand rubles | Operation |

| 60 | 51 | 354 | Payment made for forest |

| 10-1 | 60

60 |

300 | Forest accepted |

| 19 | 54 | Highlighted tax | |

| 68 | 19 | 54 | VAT accounting |

| 10-7 | 10-1 | 300 | Submitted materials for revision |

| 10-1 | 10-7 | Boards received | |

| 60 | 100 | The cost of refinement is allocated to the cost of boards | |

| 19 | 18 | Highlighted tax | |

| 60 | 51 | 118 | Transferred to a processor |

The book value of the boards at which they are put into production is: 300 + 100 = 400 rubles.

Material Transfer and Product Release

This is the standard scheme. The customer transfers the raw materials and receives products, which are then sold. The cost of materials is written off to production at the time of receipt of the goods. Processing works are also included in production costs and are taken into account when forming cost.

Example

LLC acquired fabric worth 472 thousand rubles. (VAT 72 thousand rubles) and transferred it to another organization for tailoring a coat. The cost of work is estimated at 236 thousand rubles. VAT included.

| DT | CT | Amount, thousand rubles | Operation |

| 10-1 | 60 | 472 | Fabric accepted for accounting |

| 19 | 60 | 72 | VAT allocated |

| 60 | 51 | 472 | Payment paid to the supplier |

| 68 | 19 | 72 | VAT deducted |

| 10-7 | 10-1 | 400 | Submitted materials for processing |

| 20 | 10-7 | 400 | Charged materials |

| 20 | 60 | 200 | Charged processing costs |

| 19 | 60 | 36 | VAT allocated |

| 60 | 51 | 236 | Paid processing of raw materials |

| 68 | 19 | 36 | Tax deducted |

| 43 | 20 | 600 | Accepted finished products (400 + 200) |

Cost of production includes the cost of materials and processing. To simplify the calculations in the example, the organization had no other production costs. In practice, the cost of the product may additionally include transport, travel expenses, intermediary services, part of general production costs.

Transfer of goods and receipt of other products

The refinery is handed over for processing, which are recorded with the customer on account 43. The result of the processing transaction is also the product, but in a different state. Such a scheme is often used when oil refining. Black Gold is a product for oil producing organizations. It is listed on account 43-1 "Cost of production." When transferring materials to processing, account 43-2 “GP in processing” is opened. The resulting products are returned to the customer on account 43-3 "GP after processing."

Example

The organization transfers on a commission basis oil for refining. The cost of production is 1 million rubles. The works are estimated at 472 thousand rubles. VAT included. As a result of processing, two types of products with an oil content of 30% and 70% were produced. Other expenses associated with the production of goods amounted to 200 thousand rubles.

To account for operations in the BU, sub-accounts are used:

- 43-1 "Cost of production";

- 43-2 "GP for processing";

- 43-3 "GP after processing."

| Debit | Credit | Amount, thousand rubles | Operation |

| 43-2 | 43-1 | 1000 | Oil transferred to refining |

| 43-3 | 43-2 | 300 | Product No. 1 accepted (1000 x 30%) |

| 700 | Accepted for registration product No. 2 (1000 x 70%) | ||

| 60 | 51 | 472 | Paid processing |

| 20 | 60 | 400 | Costs Included |

| 19 | 72 | Highlighted tax | |

| 68 | 19 | 72 | Tax deducted |

| 43-3 | 20 | 120

280 |

The cost of processing is included in the cost of production:

product number 1 (400 x 0.3); product number 2 (400 x 0.7). |

| 60

140 |

A part of other expenses is included in the prime cost:

product number 1 (400 x 0.3); product number 2 (400 x 0.7). |

The total cost of production after processing is:

No. 1: 300 + 120 + 60 = 480 thousand rubles .;

No. 2: 700 + 280 + 140 = 1,120 thousand rubles.

Advantages and disadvantages

It is advantageous for the contractor to produce goods from tolling raw materials.If there are many orders, but there is not enough own production capacity, he can transfer part of the orders to a third-party enterprise. Small trade organizations often use the services of contractors to pack their goods in company containers.

The processor does not bear the costs of implementation, there is no risk that the manufactured goods will not be in demand. Processing is carried out at the expense of customer materials. The manufacturer is responsible for their safety and must:

- warn the customer on the unsuitability, poor quality of the material;

- submit a report on the consumed raw materials and return the balance.

Nuance

The account 003 has been allocated specifically for accounting for tolling raw materials. For violation of this rule, a fine of 5 thousand rubles is provided. However, if the contract does not indicate the cost of the transferred materials, then there is no reason to account for the transaction as an economic one. The cost of raw materials does not participate in the formation of an asset, liability, is not income or expense. Therefore, its non-reflection on account 003 is not a tax violation.

If the processor is a payer of NPP and VAT on a common basis, receiving materials, it reflects them as tolling raw materials on the off-balance sheet account. He also does not deduct tax, especially since the seller does not issue an invoice during the transfer, but forms an invoice without VAT.

When selling goods made from tolling raw materials, the basis for calculating the tax is determined as the cost of their processing, other transformation without VAT. When accepting the work, the contractor issues an invoice. The cost of work is subject to VAT at a rate of 18%, since the object is the work, and not the sale of goods.

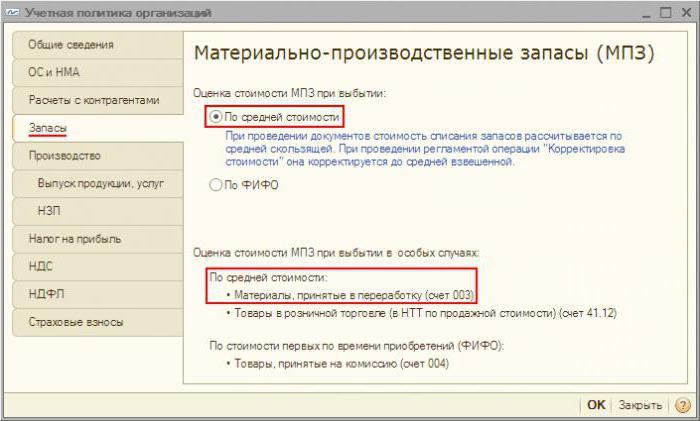

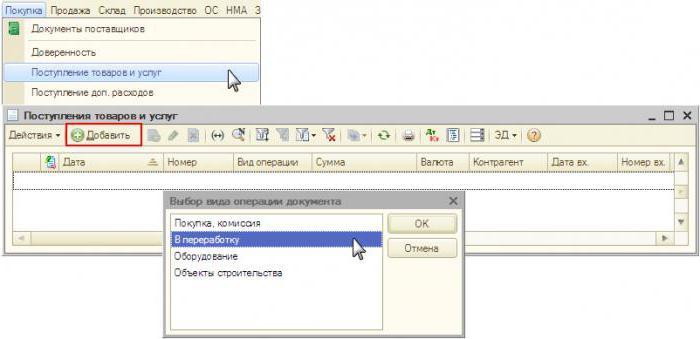

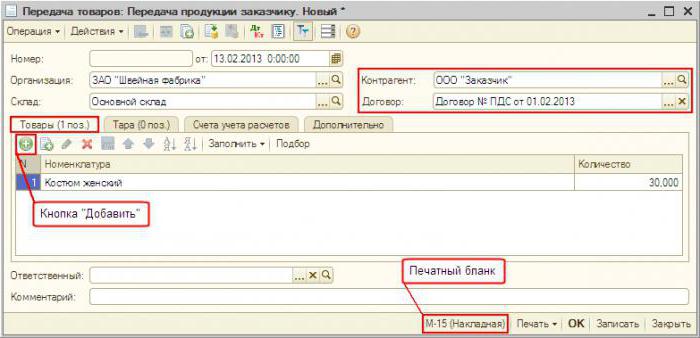

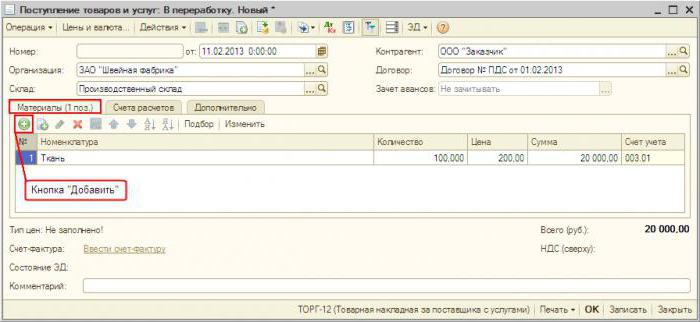

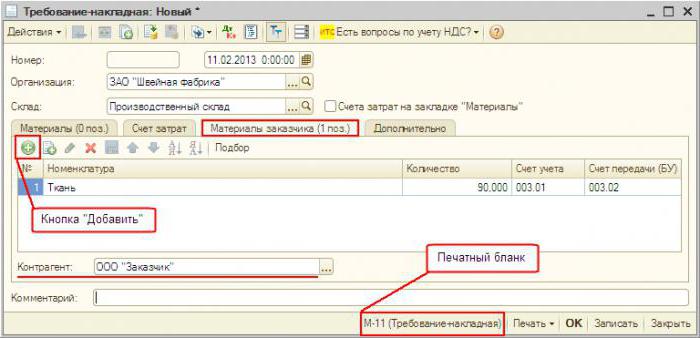

Accounting in "1C: Accounting"

Accounting for tolling in the program is practically no different from the standard. The receipt of materials is documented “Receipt of goods and services” in the menu “Purchasing”. Type of operation - “To processing”. In the document itself, you need to select materials and specify off-balance sheet account. Further, the document "Requirement-waybill" raw materials are transferred to processing. Upon completion of the process, a “Production Report" is generated. It indicates the number of manufactured goods and their cost. The document "Transfer from processing" products are transferred to a specific warehouse. On the basis of the “Invoice Requirement”, the “Sale of Processing Services” is formed. Then, according to this document, an “Invoice” is formed. The return of the waste is executed by the “Return of goods to the supplier”